Semnur Pharmaceuticals Faces Liquidity Constraints While Advancing Early-Stage Pipeline

The latest quarterly disclosure highlights Semnur’s ongoing developmental stage with tight liquidity and reliance on strategic partnerships.

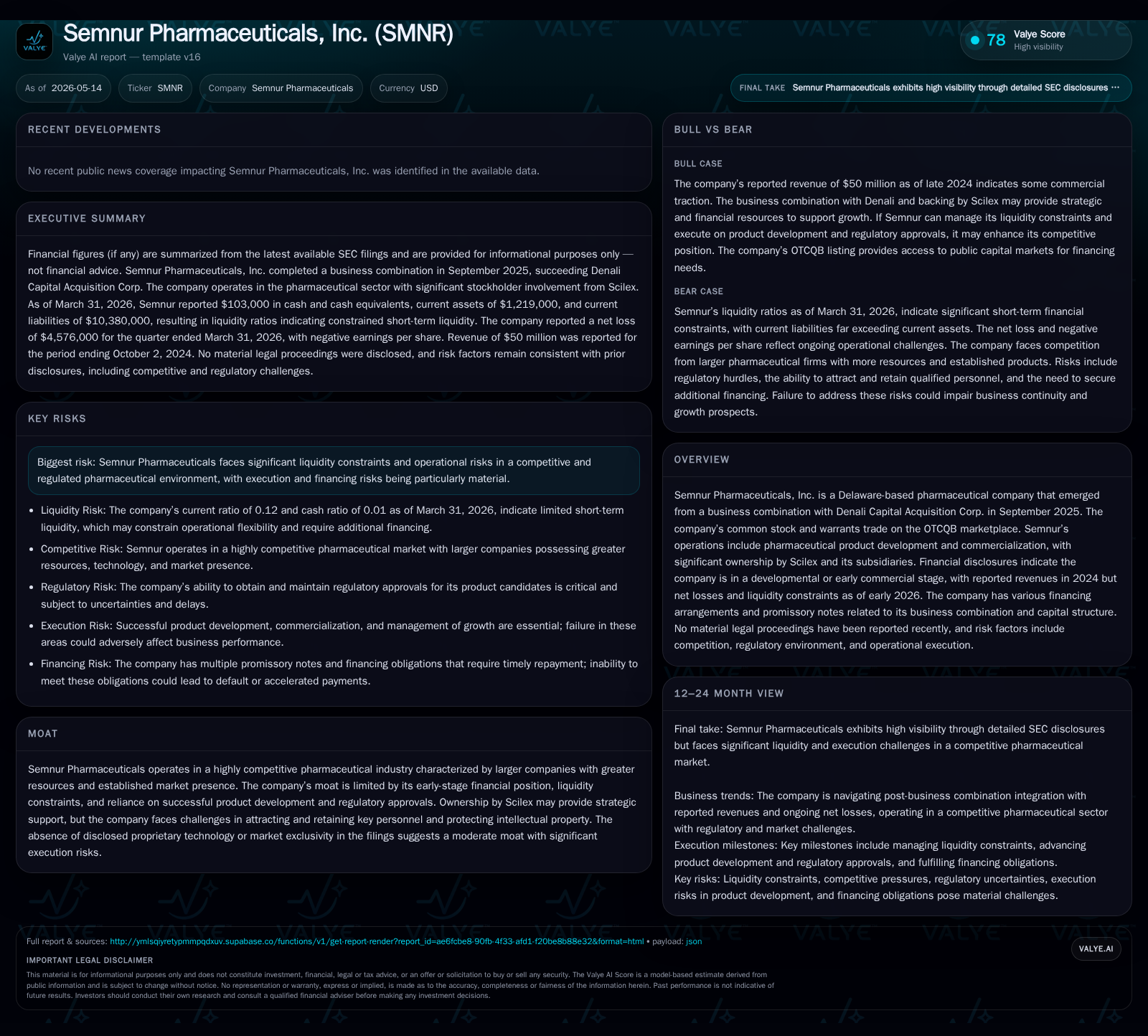

Semnur Pharmaceuticals, following its business combination in late 2025, remains an early-stage pharmaceutical company focused on product development and commercialization. The 2026 first-quarter filing reveals significant liquidity pressures with minimal cash on hand against sizable current liabilities, underscoring financing risk as a key hurdle. Despite these constraints, Semnur’s backing by Scilex Holding Company offers strategic alignment but does not mitigate substantial operational execution challenges inherent in the competitive pharma environment. Future progress hinges on advancing regulatory approvals and successfully scaling commercial operations amid these financial headwinds.

Recent Operating Update

Total debt also weighed at around $6.06 million at quarter-end [F1], further constraining flexibility to invest internally or push aggressive market entry plans. This data signals heightened refinancing and liquidity risk that could limit operational agility unless timely funding or revenue ramp occurs.

This operating snapshot contrasts somewhat with Semnur’s prior status following its business combination—in September 2025—with Denali Capital Acquisition Corp., which transitioned the company into the publicly traded sphere on the OTCQB market with ticker symbols SMNR and SMNRW (for warrants) [S3]. This structural change aimed to enhance capital access and visibility but has yet to translate into substantial operational or financial momentum.

Business Model

Semnur Pharmaceuticals operates primarily as a development-stage pharmaceutical entity focusing on the research, development, and eventual commercialization of specialized pharmaceutical products. The company derives value principally through producing product candidates that can achieve regulatory approval for market launch.

Revenue generation remains nascent; while some revenues were reported in fiscal 2024 preceding the merger [(Valye excerpt)], these remain modest relative to operating losses reflective of the high R&D spending typical in biotech sectors.

Ownership by Scilex Holding Company confers strategic benefits—including potential access to capital resources, expertise in commercialization strategies, and leverage of established industry relationships—but does not remove fundamental dependencies on successful clinical development outcomes and regulatory milestones [S3].

Revenue mechanics rely heavily on milestone payments from prospective licensing deals or product sales post-approval. The company must execute effectively across long development cycles to move candidates from preclinical stages through FDA approvals—a process costly and fraught with uncertainty.

Industry Structure and Competitive Position

The pharmaceutical sector where Semnur operates is characterized by intense competition dominated by large-cap companies with vast R&D budgets, expansive commercial operations, and robust patent portfolios. For an emerging player like Semnur:

- The absence of disclosed proprietary drug platforms or novel molecular entities reduces differentiation against entrenched competitors.

- Scale limitations impair negotiation leverage with suppliers and distributors.

- Heavy regulation governs approval timelines and post-market surveillance.

- Market access depends increasingly on payer acceptance plus evolving reimbursement models.

Semnur’s moderate moat status stems largely from its current developmental phase status combined with execution risks endemic to smaller biopharma players attempting to commercialize without much operating history or proven products (Valye excerpt).

Growth Drivers

Semnur’s path to growth centers around several key potential catalysts:

- Advancing clinical trials towards regulatory submissions—the achievement of IND filings, regulatory approvals constitutes critical inflection points.

- Launching first-to-market therapies especially in niche or underserved indications where competition might be less intense.

- Leveraging ownership ties with Scilex Holding Co. for strategic partnerships or co-commercialization arrangements that can amplify market reach.

- Potential acquisitions or licensing deals that expand the pipeline or accelerate time-to-market for new candidates.

Successful progression along each milestone would enhance Semnur’s revenue profile from minimal levels towards commercialization-scale sales streams while potentially improving negotiating power across the supply chain.

Risks / Watchpoints / Growth Constraints

Several factors threaten Semnur’s trajectory:

- Liquidity Risk: Cash reserves are critically low ($103K) relative to obligations exceeding $10 million; failure to secure additional funding could impede ongoing operations [F1][S2].

- Execution Risk: Transitioning from product development to successful commercialization requires robust operational capabilities that may be underdeveloped given current scale.

- Regulatory Risk: The inherent uncertainty of FDA approval processes means pipeline projections remain highly contingent.

- Competitive Pressure: Larger peers possess superior resource depth making marketplace entry challenging.

- Retention Risk: Attracting and retaining highly skilled personnel critical for R&D success remains a challenge without demonstrated commercial success (Valye excerpt).

What to Watch Next

Key indicators for monitoring Semnur's operational health include:

- Quarterly burn rate trends indicating financial runway extensions or contractions [S2].

- Progress reports related to clinical trial milestones or regulatory submissions as publicly disclosed.

- Updates on capital raising initiatives such as equity offerings, debt facilities, or partnerships announced via SEC filings or press releases [S3].

- ANY enhancement of licensing deals or collaboration agreements expanding the commercial footprint.

- Changes in ownership structure or strategic shifts involving Scilex Holding Co.’s stake.

These markers will elucidate whether Semnur can effectively navigate near-term financial stress while positioning itself for sustainable longer-term growth.

Financial Profile (Latest Quarter Snapshot)

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $103000 | |

| 2026-03-31 | ||

| Total debt | $6mm | |

| 2026-03-31 | ||

| Net debt | $6mm | |

| 2026-03-31 | ||

| Current assets | $1219000 | |

| 2026-03-31 | ||

| Current liabilities | $10mm | |

| 2026-03-31 | ||

| Current ratio | 0.12x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value | Period End |

|---|---|---|

| Cash & equivalents | $103,000 | |

| 2026-03-31 | ||

| Total Debt | $6,058,000 | |

| 2026-03-31 | ||

| Current Assets | $1,219,000 | |

| 2026-03-31 | ||

| Current Liabilities | $10,380,000 | |

| 2026-03-31 | ||

| Current Ratio | 0.12 | |

| 2026-03-31 | ||

| Net Debt | $5,955,000 | |

| 2026-03-31 |

The severely constrained current ratio underscores acute short-term liquidity challenges requiring resolution through financing solutions or revenue growth expansion [F1][S2].

This analysis synthesizes Semnur Pharmaceuticals’ available public disclosures focusing heavily on recent quarterly developments reflecting operational difficulties characteristic of early-stage biotech companies. While strategic support exists via Scilex Holding Company affiliation, Semnur faces material risks that investors and stakeholders should carefully monitor going forward.

This narrative does not constitute investment advice but aims instead to provide an informed perspective grounded firmly in documented SEC filings and company disclosures as of mid-May 2026.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments