Sow Good Transitions Leadership Amid Tanzanian Graphite Project Acquisition

Recent executive upheaval coincides with Sow Good’s strategic acquisition of an advanced-stage graphite asset, spotlighting its liquidity challenges and growth outlook.

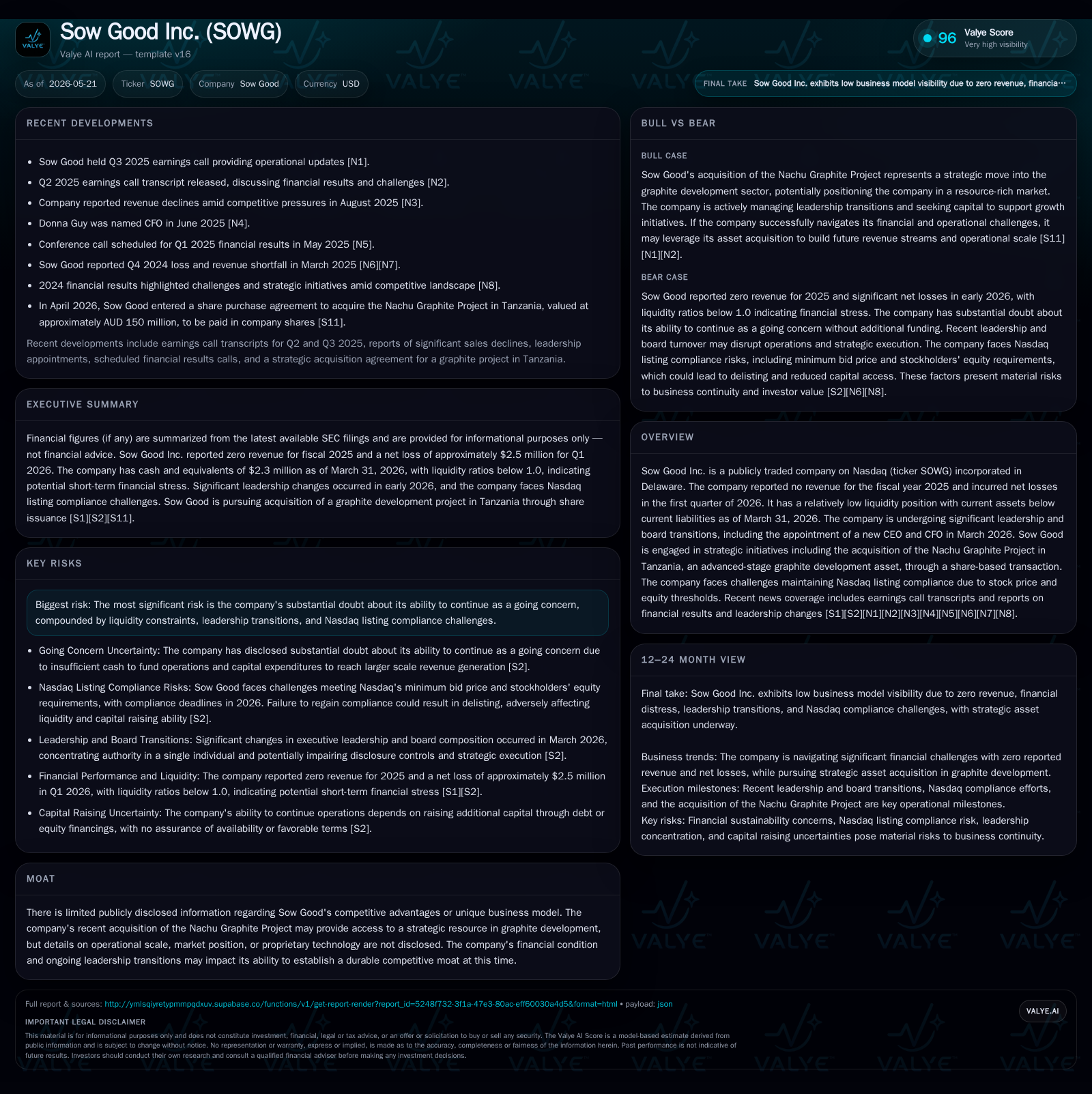

Sow Good Inc. reported a precarious liquidity stance and mounting doubts about its ability to continue as a going concern in its 2026 first-quarter filing. The company has entered a transformative phase with the acquisition of the Nachu Graphite Project in Tanzania, signaling a pivot toward asset-backed resource development despite zero revenue in 2025. Alongside this strategic move, Sow Good underwent significant leadership and board turnover, consolidating decision-making authority under one individual but raising governance risks. The company’s growth depends heavily on successful capital raises and regulatory approvals in Tanzania amid pressures to maintain Nasdaq listing compliance.

Recent Quarterly Developments Spotlight Operational Uncertainty

Simultaneously, a major overhaul of Sow Good's senior leadership occurred. Both the CEO David Lazar and CFO Donna Guy resigned effective March 31, replaced by Yisroel Goldberg who assumed both roles [S2][S3][S28]. In conjunction with this executive turnover, five Board members resigned and four new directors were elected, concentrating authority significantly under Goldberg. This rapid transformation raises concerns about governance stability, knowledge retention, and continuity as noted by management itself.

This confluence of liquidity strain paired with volatile governance introduces heightened risks around operational execution capacity and investor confidence during ongoing development efforts.

Business Model Orientation and Strategic Asset Acquisition

Historically characterized by exploration-stage operations without revenue generation—confirmed by zero reported revenue for fiscal year 2025—Sow Good's business model principally involved early resource evaluation activities [F1][S1]. Its operating losses reflected developmental expenditures absent commercial production.

However, recent strategic moves represent a tectonic shift towards resource ownership at a more advanced stage. On April 20, 2026, Sow Good agreed via a share purchase agreement to acquire Uranex Tanzania Limited and Magnis Technologies (Tanzania) Limited from Ryzon Materials Ltd., thereby gaining control of the Nachu Graphite Project — an advanced graphite development asset situated in southern Tanzania's Lindi region valued at AUD 150 million (approximately USD 107 million) through issuance of common stock shares [S15][S16]

This transaction transitions Sow Good from pure exploration towards project development with tangible mineral assets capable of supporting future production once capitalized effectively. The acquisition consideration entails about 22 million post-reverse-split shares issued contingent on closing conditions including regulatory approvals in Tanzania and shareholder consent under Nasdaq rules.

While this shifts core value proposition towards downstream project advancement rather than prospecting alone, the operational scale-up demands substantial capital deployment for permits, feasibility studies, infrastructure buildout, and eventual mining operations.

Industry Dynamics in Graphite Development and Resource Sector

Graphite is central to emerging technology sectors such as lithium-ion batteries powering electric vehicles (EVs), renewable energy storage solutions, and industrial lubricants. Advanced-stage graphite projects like Nachu hold strategic potential given increasing demand forecasts driven by decarbonization trends.

Nonetheless, graphite mining ventures face intrinsic challenges: exposure to commodity price volatility influences project economics; capital intensity requires access to sizeable upfront investment especially for African projects facing infrastructural hurdles; regulatory compliance necessitates navigating local mining codes including environmental impact assessments; geopolitical risk factors moderate investment appetite; quality variability across deposits complicates market acceptance.

Tanzania as an emerging mining jurisdiction presents both opportunities via rich mineral endowment and hurdles through bureaucratic complexity or competition from established producers in China or Mozambique.

Competitively, Sow Good operates without disclosed proprietary processing technologies or diversified product portfolios limiting defensibility - positioning it primarily as a junior resource developer reliant on scaling Nachu efficiently while managing cost execution and permitting timelines.

Growth Drivers: Nachu Project Potential and Capital Raising Imperatives

Fundamental growth drivers depend on converting the Nachu graphite asset into feasible production capability accompanied by sufficient financing support. Key levers include:

- Successful closing of the share-based acquisition subject to shareholder approval and Tanzanian regulatory endorsements per transaction terms expiring October 2026 [S15][S16].

- Raising capital beyond existing cash reserves—including securing definitive credit documentation for announced $20 million line of credit sought via non-binding term sheet announced May 5, 2026—to fund next-stage development expenditures such as drilling programs or plant construction [S13].

- Effective management execution led by recently appointed leadership tasked with steering permitting milestones while restoring investor trust amidst governance shifts.

- Strategic engagement with Tanzanian authorities including fair competition commission clearance expected to mitigate operational risk.

Absent these foundational developments both liquidity pressures will intensify while project advancement timelines could stall indefinitely restricting medium-term revenue prospects.

Risks: Liquidity, Governance Changes, and Nasdaq Compliance Challenges

Several interrelated risks dominate the current outlook:

Liquidity Constraints:

The company's cash reserves are insufficient to cover current liabilities or develop the Nachu Project adequately without raising additional funds imminently [F1][S2][S23]. Failure to secure acceptable financing could force curtailment of operations or bankruptcy scenarios leading to total investor loss.

Governance Concentration Risk:

Consolidation of CEO/CFO roles under Mr. Goldberg simultaneously with wholesale board changes may impair internal controls or decision quality during critical stages demanding multifaceted expertise. Institutional knowledge depletion poses execution hazards.

Nasdaq Listing Compliance:

Nasdaq notified Sow Good in April 2026 that it failed minimum stockholders' equity requirements ($2.5M threshold) based on December 31 figures—a breach triggering potential delisting unless rectified within set deadlines extending potentially through October 2026 [S14][S29]. Also relevant is previous minimum bid price deficiency remedied only recently but continuing issuance dilution may pressure stock value further complicating equity raises.

These risks suggest elevated volatility for shareholders with heightened default probabilities absent successful turnaround steps.

What to Watch Next: Funding Milestones and Project Progress Updates

Investors should monitor several upcoming indicators pivotal for assessing turnaround viability:

- Timely consummation of Nachu acquisition including receipt of shareholder votes approving new common stock issuances tied to purchase consideration [S15][S16].

- Regulatory clearance updates from Tanzanian governmental bodies—the Mining Commission and Fair Competition Commission essential for closing within Sunset Date October 15, 2026.

- Closure or extension terms relating to announced $20 million credit facility critical for near-term financial runway stabilization [S13].

- Subsequent quarterly filings revealing cash burn reduction trajectories post-financing or operational reprioritization strategies.

- Nasdaq correspondence regarding continued listing compliance status especially regarding equity thresholds throughout remainder of calendar year [S14][S29].

- Leadership communication evidencing management integration success while maintaining disclosure controls after massive board reshuffling.

Performance on these fronts will clarify whether Sow Good can transition from capital-constrained early-stage entity into funded graphite project developer capable of delivering scale economies later.

Financial Profile: Current Assets, Liabilities, and Capital Constraints

As of March 31, 2026, Sow Good held approximately $2.3 million in cash versus $4.3 million in current liabilities translating into a suboptimal current ratio (~0.68) highlighting imminent liquidity mismatch risks [F1]

The accumulated deficit exceeding $105 million evidences sustained negative earnings trends from developmental expenditures absent revenue inflows confirming ongoing cash burn pressures [S2][S23]. Management acknowledges these factors precipitate "substantial doubt" over going concern assumptions emphasizing urgent necessity for capital raises.

A sales agreement allowing for share offerings up to $100 million exists but efficacy depends on market receptivity constrained by ongoing stock price weakness coupled with Nasdaq delisting threats impeding financing options availability on reasonable terms [S22]. Without prompt strengthening of cash positions financing downtime could necessitate operational slowdowns jeopardizing recovery feasibility.

Disclaimer: This analysis is based exclusively on publicly filed documents including SEC disclosures cited herein up to May 21, 2026. It does not constitute investment advice or research views but aims solely to present an informed industry perspective synthesizing recent operational developments affecting Sow Good Inc.'s business position and outlook.

Financial position in context

As of 2026-03-31, companyfacts shows $2mm in cash and equivalents [F1]. Current assets of $3mm and current liabilities of $4mm imply a current ratio near 0.68x for 2026-03-31 [F1].

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments