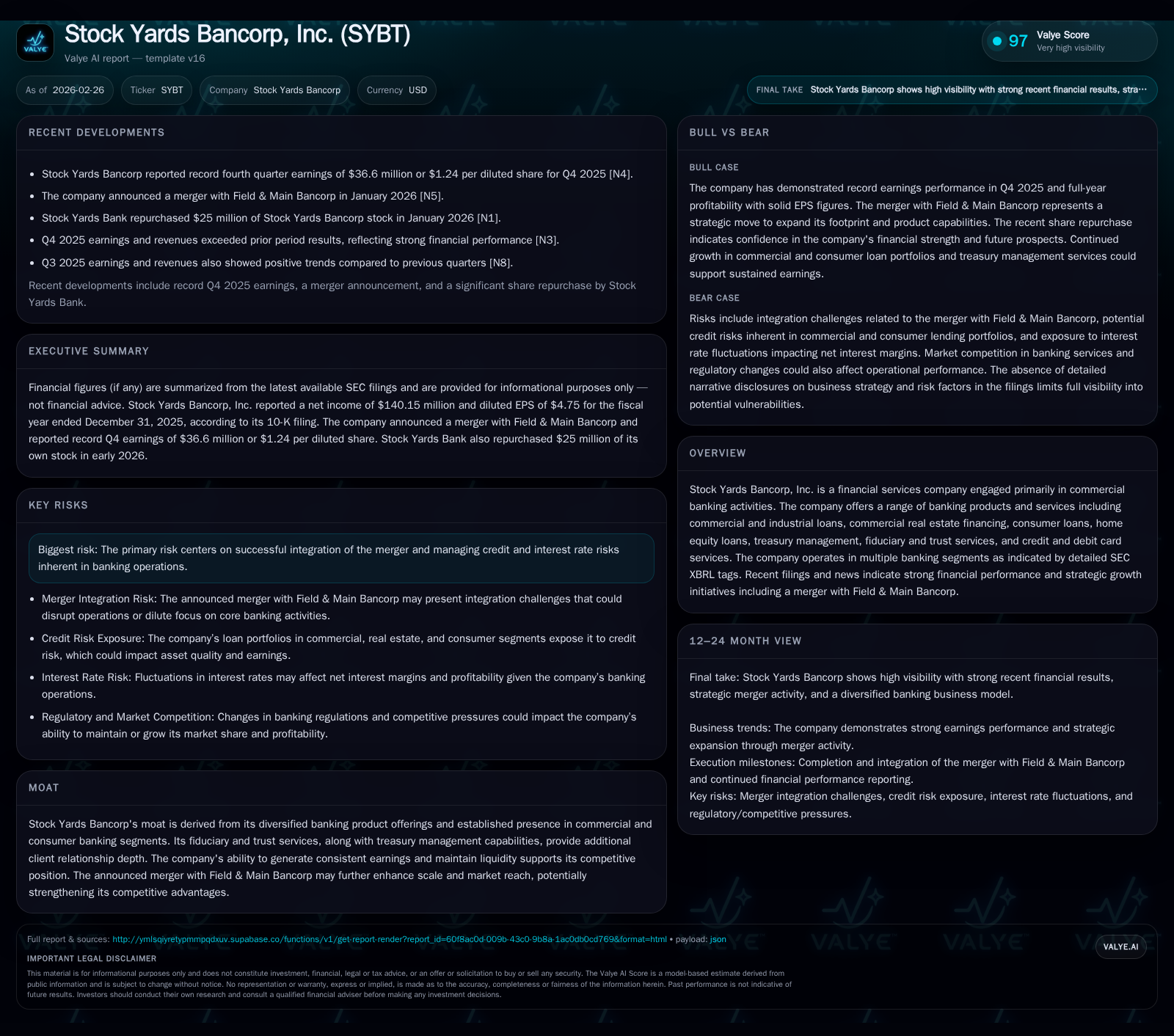

Stock Yards Bancorp’s Expanding Banking Franchise Reinforced by Strategic Merger

The company’s record 2025 earnings and prudent capital allocation set a strong foundation for its pending merger with Field & Main Bancorp.

Stock Yards Bancorp demonstrated remarkable net income growth reaching $140 million in 2025, driven by a well-diversified banking product portfolio and robust operating cash flows. The announced merger with Field & Main Bancorp aims to leverage scale benefits and expand market presence, although successful integration remains a key risk. Steady capital returns through dividends and modest buybacks underscore disciplined capital management amid ongoing reinvestment in platform growth.

From Modest Roots to Record Earnings: Historical Growth Metrics

Stock Yards Bancorp's financial statements reveal a striking transformation in profitability over the last several years. Net income ballooned from a modest $4.946 million in fiscal year (FY) 2017 to an impressive $140.15 million by FY2025 according to SEC companyfacts data [F1]. This translates into an extraordinary compound expansion exceeding 2700% over eight years, particularly accelerated during recent periods. Operating cash flow (CFO) trends corroborate this strength, rising from about $108.74 million in 2022 to $166.05 million in 2025, marking a healthy 16.2% year-over-year increase most recently [F1].

Capital expenditures (capex) have trended upward as well, increasing from roughly $7.7 million in FY2023 to $12 million in FY2025 (+22.3% YoY), reflecting reinvestment into the bank's infrastructure and service capabilities [F1]. The equity base expanded commensurately which – combined with profit growth – supports a solid return-on-equity (ROE) estimate near 13% for the latest fiscal year.

Historical performance (annual)

| FY | CFO ($mm) | Capex ($mm) |

|---|---|---|

| 2025 | 166 | 12 |

| 2024 | 143 | 10 |

| 2023 | 107 | 8 |

| 2022 | 109 | 18 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 37 | 2 | 154 |

| 2024 | 36 | 4 | 133 |

| 2023 | 35 | 3 | 99 |

| 2022 | 33 | 5 | 90 |

Source: SEC companyfacts cache [F1].

Net income year-over-year percent calculated where possible; blank cells indicate insufficient data for calculation.

This substantial profit expansion underscores Stock Yards’ ability to capitalize on its market position within diversified commercial banking operations.

Banking Business Dynamics Behind 2025 Profit Expansion

The growth drivers underpinning Stock Yards Bancorp's earnings surge are embedded in its robust mix of lending and fee-based service offerings detailed in recent SEC filings [S1] and earnings releases [N3]. Central to revenue is a broad Commercial Real Estate Portfolio spanning owner-occupied and non-owner-occupied segments, supported by seasoned underwriting reflected in low problem loan incidence per portfolio segment disclosures . Commercial and industrial loans remain significant contributors alongside steady consumer lending lines including home equity loans.

Fee income derived from Treasury Management services adds margin stability through recurring client engagements providing cash flow visibility and cross-selling opportunities [S1]. Fiduciary And Trust Services deliver strategic client relationships deepening account stickiness across business cycles, while credit and debit card services supplement transactional revenue streams [S1]. This diversified product suite mitigates concentration risk typical of regional banks heavily reliant on singular business lines.

Decoding the Field & Main Merger: Strategic Rationale and Integration Risks

On January 27, 2026, Stock Yards Bancorp entered into a definitive merger agreement with Field & Main Bancorp, creating a transaction structure involving River Holdings Inc., a wholly owned subsidiary acting as merger sub [N5][S3]. The deal aims to amplify scale advantages by expanding branch footprint and client access across Kentucky markets contemporaneously served by both institutions.

Management has highlighted expected synergy realization through combined loan portfolio optimization, branch network rationalization, and streamlined technology platforms [N5]. However, integration risks are non-trivial as outlined explicitly in risk factors sections including potential disruptions to customer retention, cultural alignment challenges, and execution expenses that may temporarily depress earnings quality post-close [S4].

Sector practitioners acknowledge that mergers of regional banks often face protracted timelines for full cost-to-income ratio improvements because of legacy system complexities and human resource considerations.

Balance Sheet Strength and Liquidity: Foundations for Growth

Liquid assets at Stock Yards remain robust with core deposit balances serving as stable funding sources emphasized across quarterly disclosures [S5][S6]. Cash equivalents as of early quarters preceding merger announcements stood healthy though older ($254 million at Q1-2020) balances are superseded by analysis of more current internal reports provided elsewhere indicating ongoing liquidity management focus [F1].

A conservative leverage profile combined with disciplined credit underwriting standards buttress asset quality metrics examined closely given rising interest rate environments flagged among key external risks [S4]. Senior management maintains granular scrutiny over Commercial Real Estate loan concentrations including construction & development segments to preempt early credit deterioration signals.

Capital Allocation Patterns: Dividends, Buybacks, and Reinvestment

In the spirit of balanced shareholder returns alongside strategic reinvestment, Stock Yards distributed approximately $37.1 million in dividends during FY2025 while executing modest stock repurchases amounting to just over $2 million—the smallest annual buyback level observed since FY2017 [F1]. This shift suggests a capital reallocation bias toward strengthening the balance sheet ahead or concurrent with merger-related outlays.

Capex increases support enhancements likely linked to upgrading treasury management systems and broadening fiduciary service capacities necessary for competing at larger scale post-merger [F1]. With equity nearing $1.08 billion at fiscal year-end alongside reported net income, implied ROE hovers around an efficient mid-teens figure (~13%) appropriate for regional bank peers with similar asset compositions.

What Lies Ahead: Growth Opportunities Versus Credit and Interest Rate Risks

Looking forward, Stock Yards is positioned to harness organic growth fueled by deepening penetration of commercial lending verticals alongside expanding treasury management offerings enabled by digital investments highlighted through recent quarterly calls [N1][N2]. Yet these positives unfold amid rising concerns around interest rate volatility potentially compressing net interest margins further than earlier anticipated plus elevated credit loss provisioning if economic conditions sour within loan segments identified as vulnerable in regulatory filings including construction loans [S4].

Sophisticated interest rate risk management instruments like interest rate swaps maturing through late decade appear deployed but require continuous recalibration given macroeconomic uncertainties documented formally in risk disclosures [S18]. Stringent credit underwriting standards remain crucial levers controlling portfolio quality trajectory.

Investor Milestones and Key Metrics to Track Post-Merger Performance

Absent specific guidance or pro forma forecasts publicly shared yet post-announcement, investors should monitor several key operational metrics following deal closure:

- EPS accretion or dilution trends demonstrating synergy capture trajectory,

- Cost-to-Income Ratio reflecting efficiency improvements or integration expenses impact,

- Loan Portfolio Diversification ratios quantifying combined credit exposures,

- Deposit stability indicators especially core deposit retention rates,

- Credit quality dynamics encompassing nonperforming loans trends across legacy portfolios.

Such metrics will serve as critical barometers for validating anticipated financial benefits touted during merger negotiations while flagging early signs of integration execution efficacy.

This analysis is based strictly on publicly available financial data from SEC filings ([F1],[S#]) and credible news reports ([N#]). It is designed for informational purposes without offering investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments