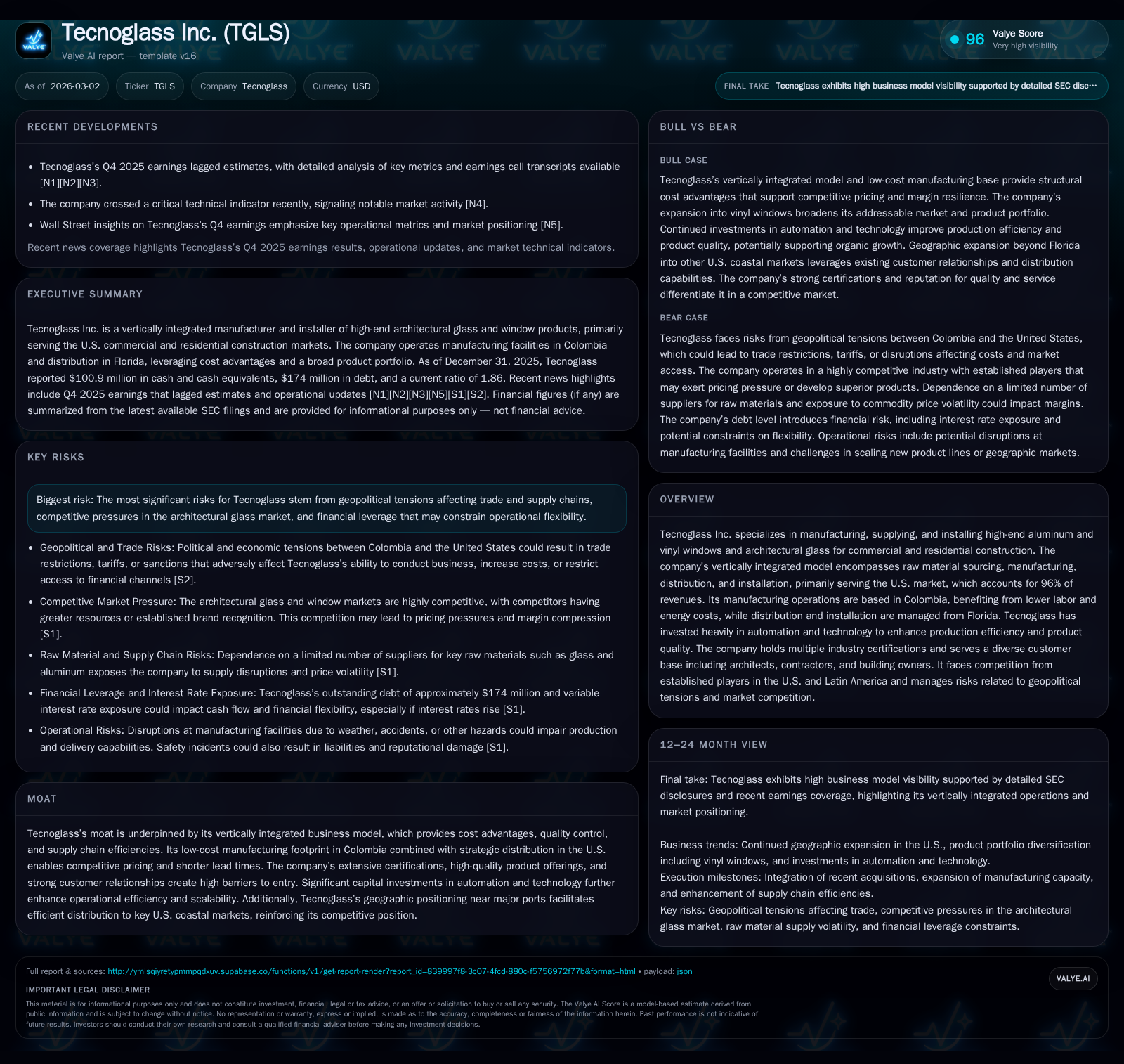

Tecnoglass Inc. Credits Vertical Integration for Steady Margin Resilience

Tecnoglass leverages its integrated manufacturing and distribution model alongside geographic advantages to sustain growth and profit stability in a competitive, tariff-sensitive market.

Tecnoglass Inc. distinguishes itself through a vertically integrated business model that spans raw material sourcing, manufacturing, distribution, and installation. This integration, combined with cost-efficient manufacturing in Colombia and strategic U.S. distribution hubs, supports robust revenue growth and steady operating income margins despite raw material inflation and geopolitical challenges. Recent capital investments in automation and acquisitions underpin a positive medium-term outlook amid risks from trade tensions and leverage constraints.

Historical Performance and Growth Drivers: Scaling Manufacturing and Market Reach

Tecnoglass Inc.’s growth trajectory is anchored by its vertically integrated model encompassing manufacturing, distribution, and installation services primarily targeting the U.S., which constitutes about 96% of revenues [S4][S5]. While the latest available revenue figure dates to fiscal year 2018 at $97.9 million [F1], the company has demonstrated strong operational performance with operating income reaching $230.7 million in FY2025, up slightly from prior years despite raw material cost pressures [F1].

The acquisition of Continental Glass Systems in April 2025 notably expanded Tecnoglass’s presence within the U.S., particularly outside Florida, enhancing backlog strength and diversifying project geography [S5][S11]. High-profile projects including Aston Martin Residences (Miami) and Salesforce Tower (San Francisco) underscore Tecnoglass’s positioning in high-specification markets requiring rigorous quality standards and fast delivery [S18].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 160 | 136 | 231 | 101 | -1.1% |

| 2024 | 161 | 171 | 227 | 80 | -11.8% |

| 2023 | 183 | 139 | 260 | 78 | +17.4% |

| 2022 | 156 | 142 | 226 | 71 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 28 | 34 | |

| 2024 | 20 | 91 | |

| 2023 | 16 | 61 | 33.4 |

| 2022 | 13 | 71 | 44.6 |

Source: SEC companyfacts cache [F1].

Table: Historical Financial Performance Summary [F1]

Capital Allocation: Balancing Growth Investments and Cash Generation

Tecnoglass maintains a capital-intensive investment approach focused on expanding capacity and enhancing automation capabilities—evidenced by capex rising over 27% from $79.6 million in FY24 to $101.3 million in FY25 [F1][S21]. Operating cash flow declined approximately 20% year-over-year to $135.8 million in FY25, reflecting working capital dynamics amid growth initiatives [F1]. Despite this contraction, free cash flow remains positive near $34.5 million.

Shareholder returns have grown steadily with dividends increasing from $12.9 million in FY22 to an estimated $28 million in FY25, indicating management's commitment to shareholder remuneration alongside reinvestment priorities [F1]. The company’s capital structure includes a $174 million term loan maturing in late 2030 at SOFR plus a spread of approximately 125 basis points providing manageable leverage with liquidity supported by a current ratio near 1.86 at year-end FY25 [F1][S7][S8].

Competitive Strengths: Vertical Integration and Cost Advantages

Tecnoglass’s vertically integrated model spans raw glass sourcing—supported by minority ownership in Vidrio Andino Holdings S.A.S.—through manufacturing aluminum extrusions/vinyl products at its Colombian facility near major ports, distribution logistics, and final installation services predominantly across U.S markets [S10][S14][S19]. This integration reduces supply chain inefficiencies, enables strict quality control, shortens lead times, and lowers costs relative to competitors reliant on more fragmented supply chains.

The Barranquilla plant’s proximity (<16 km) to key Colombian ports allows direct maritime shipments to major U.S coastal cities with transit times substantially shorter than competitors relying on land transport alone—a critical advantage for time-sensitive construction projects [S19]. Labor cost arbitrage is significant as Colombian wages remain materially lower than comparable U.S roles while automation reduces dependency on manual labor inputs mitigating wage inflation risk [S14][S21].

Complementing operational efficiencies are sustainability initiatives including onsite solar energy generation (~5MW), reducing energy costs while aligning with environmental governance standards sought by clients [S14]. Competitors include Viracon (Apogee Enterprises subsidiary), PGT Industries, Cardinal Glass among others; however Tecnoglass’s product breadth, certifications (e.g., IGCC, ISO9001), and custom solutions create barriers against new entrants lacking comparable scale or technical expertise [S9][S12][S20].

Recent Earnings Context: Q4 Performance Highlights

In Q4 2025 earnings released February 26, 2026, Tecnoglass reported results below analyst estimates driven by unexpected increases in raw material costs—particularly aluminum price spikes—and inventory adjustments amid shifting demand patterns across commercial construction segments [N2][N4]. Revenue growth remained positive but decelerated compared to prior quarters.

Investor sentiment reflected caution as shares crossed technical support levels signaling concerns over narrower margins and expense pressures despite backlog strength [N6]. Management emphasized focus on backlog conversion efficiency and sustaining customer service levels amid these external cost headwinds [N3].

Risk Factors: Geopolitical Exposure and Operational Concentration

Tecnoglass’s manufacturing base is concentrated in Colombia while nearly all revenues derive from the United States (~96%), exposing it to geopolitical risks including trade policies between Colombia/U.S., Venezuela-related tensions affecting supply corridors, potential tariffs or reciprocal duties should diplomatic relations shift unfavorably [S2][S9][S16].

Although no reciprocal tariffs are currently active, policy uncertainty persists under changing political administrations potentially impacting cross-border trade costs or financial access.

Operational risk centers on reliance upon the main manufacturing complex which houses critical equipment for core product lines; localized disruptions such as weather events or accidents could cause significant production delays without alternate capacity options available immediately [S9][S24][S27]. Labor availability also remains a factor given local market conditions.

Raw material price volatility—particularly aluminum extrusion priced against London Metal Exchange benchmarks—introduces input cost unpredictability despite hedging mechanisms aimed at mitigating short-term shocks; sustained commodity price increases could compress margins absent effective pricing strategies [S9][S10].

Outlook: Expansion Initiatives and Innovation Focus

While explicit forward guidance is not publicly available, growing order backlogs outside Florida into East Coast markets along with states like Texas support incremental growth prospects while reducing regional concentration risk inherent from historically >90% Florida revenue share [N3][S11][S13]. Acquisition synergies post-Continental Glass Systems integration are expected to enhance vertical integration benefits extending supply chain control deeper into the U.S.

Product innovation includes new vinyl window offerings launched late-2023 broadening addressable markets where vinyl frames dominate residential segments traditionally underserved by aluminum products [S13][S21]. Automation improvements are ongoing targeting ~30% reductions in labor waste and onsite damage rates enhancing throughput scalability supporting mid-to-long-term margin sustainability as volumes expand without proportional cost increases [S20][S21].

What Investors Should Monitor

Key indicators include backlog growth outside Florida revealing success of geographic diversification strategies; margin trends amidst persistent input inflation revealing procurement agility; leverage metrics assessing balance sheet flexibility given acquisition-driven debt levels; receivables aging reflecting credit quality amid customer concentration where top ten clients represent about one-third of sales but none exceeds single-digit percentages individually mitigating counterparty risk partially yet warranting vigilance [F1][S6][S7].

This analysis integrates public financial data from SEC filings alongside recent market commentary without recommending any investment action regarding Tecnoglass Inc.'s securities or operations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments