TriNet Group’s Strategic Edge in Complex SMB HR Outsourcing Amid Shifting Regulatory Terrain

TriNet leverages its PEO model and regulatory expertise to deliver integrated HR solutions to SMBs, balancing growth with operational and compliance challenges.

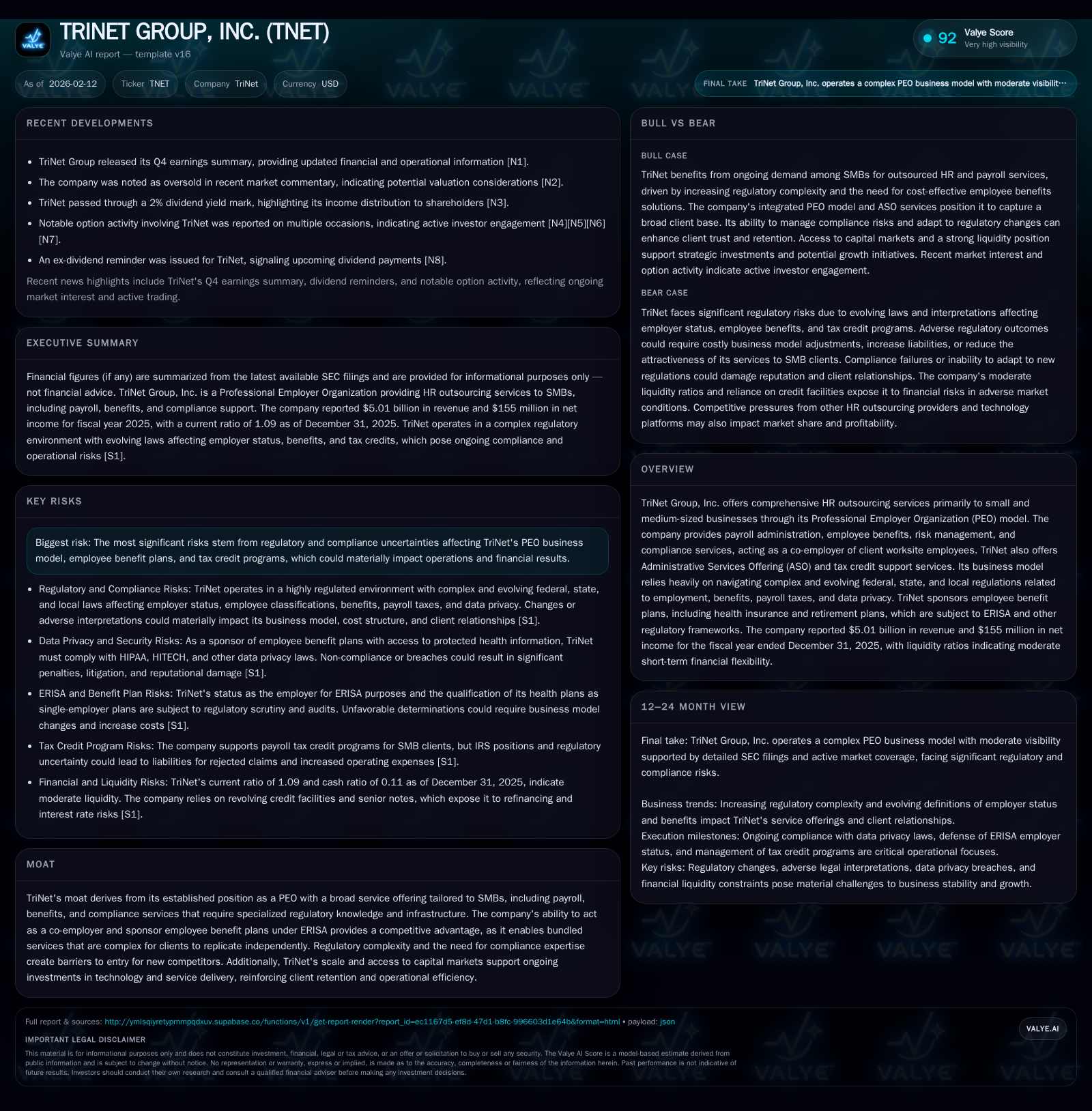

TriNet Group, Inc. occupies a distinctive position in the small and medium-sized business (SMB) human capital management space by providing comprehensive outsourcing services through its Professional Employer Organization (PEO) structure. With $5 billion in revenue for 2025 and a net income of $155 million, TriNet’s scale and regulatory know-how underpin competitive advantages, including ERISA plan sponsorship and co-employment relationships that are difficult for competitors to replicate. However, financial performance reflects pressure from restructuring costs and compliance investments in an evolving legal landscape encompassing data privacy and employment regulations. Continued platform enhancements and disciplined risk governance support TriNet's resilience as it navigates macroeconomic and legislative uncertainties affecting the broader HR outsourcing industry.

TriNet at a Glance: Serving SMBs with Integrated HR Solutions

TriNet Group, Inc. specializes in providing outsourced human resources services tailored primarily to small and medium-sized businesses (SMBs) through its Professional Employer Organization (PEO) model. This approach involves acting as a co-employer for client worksite employees, enabling TriNet to bundle a broad suite of HR services including payroll administration, employee benefits sponsorship, risk management solutions, and regulatory compliance assistance[ S1 ]. In fiscal year 2025, TriNet generated approximately $5.01 billion in revenue with a net income of $155 million[ F1 ]. The company manages both employees co-employed by TriNet as well as platform users who access its HRIS tools for functions like benefits management or bookkeeping without necessarily running payroll regularly. This dual revenue stream reflects a diversified service base increasingly monetized since 2023 through usage-based billing[ S1 ].

TriNet's clientele predominantly comprises smaller enterprises that often lack the internal infrastructure or expertise to navigate complex employment law and benefit programs themselves. By consolidating these offerings into a single outsourced relationship, TriNet provides operational leverage for clients balancing cost-efficiency with human capital risk mitigation.

Decoding the PEO Model: Co-Employment and Bundled Services Advantage

At the core of TriNet’s competitive positioning is its status as a PEO that establishes a statutory co-employment relationship with client personnel. This legal arrangement allows TriNet to act as the employer of record for purposes related to payroll taxes, employee benefit plans governed by ERISA (Employee Retirement Income Security Act), workers’ compensation insurance, and related compliance obligations[ S1 ]. Such responsibilities entail navigating multifaceted regulation across numerous jurisdictions—federal, state, and local—which frequently feature overlapping or inconsistent mandates.

This co-employment structure enables TriNet to offer bundled services that are administratively complex for clients to replicate independently. Moreover, sponsoring employee benefit plans directly under ERISA affords regulatory protections but also imposes fiduciary duties requiring specialized compliance infrastructure. These factors create substantial barriers to entry for new market participants lacking established legal frameworks or economies of scale necessary for cost-effective service delivery[ S1 ].

Furthermore, TriNet’s ability to integrate federal tax credit support programs complements its comprehensive value proposition. The tightly regulated nature of these programs further entrenches the company's moat by requiring continual adaptation to shifting legislative interpretations.

Financial Performance Weighed Against Operational Challenges (2023-2025)

Despite consistent revenue around the $5 billion mark over recent years[ F1 ], TriNet’s net income declined notably from $375 million in 2023 to $155 million in 2025[ S1; F1 ]. This reduction aligns with increased restructuring costs ($11 million in 2025 versus none in 2023), along with elevated expenses related to stock-based compensation ($65 million annually) and higher operating investment expenditures impacting adjusted EBITDA margin which fell from 14% in 2023 to approximately 8.5% in 2025[ S1 ].

The company maintains solid liquidity reflected in a current ratio of roughly 1.09 (current assets of $2.87 billion against current liabilities of $2.64 billion)[ F1 ], signaling sufficient short-term financial flexibility despite operating headwinds.

Management’s disclosures highlight ongoing efforts toward strategic realignment designed to improve operating efficiencies amidst inflationary pressures affecting insurance costs and wage trends[ S1; S2 ]. These efforts are embedded within larger digital transformation initiatives intended to future-proof service delivery mechanisms.

Regulatory Headwinds: Compliance, Data Privacy, and ERISA Obligations

TriNet operates at the intersection of numerous regulatory layers encompassing labor classification rules, wage-hour laws, benefits administration statutes, tax regulations, workers’ compensation regimes, insurance requirements, anti-discrimination statutes, health information privacy standards under HIPAA/HITECH Acts, and fiduciary mandates associated with ERISA-governed plans[ S1 ].

The company explicitly acknowledges data privacy as a significant area of risk due both to its stewardship of protected health information (PHI) within sponsored benefit plans and sensitivities around Personally Identifiable Information (PII). Compliance failures could expose TriNet to substantial fines, litigation including class action suits, regulatory investigations, reputational harm, and remediation costs which would materially impact financial performance[ S1 ].

Furthermore, ambiguities about how certain employment laws apply to PEO entities contribute additional uncertainty. Since many statutes do not clearly delineate applicability or enforcement standards relative to co-employment relationships, regulatory scrutiny varies widely by jurisdiction creating complexity for operational execution.[ S1 ]

Technology and Platform Evolution Driving Client Engagement

Investments since early 2023 into platform capabilities have significantly expanded TriNet’s engagement model beyond traditional payroll-based revenue streams. The rollout of usage-based billing for PEO Platform Users — individuals authorized by clients who may not be officially co-employed but require access for administrative functions — has broadened monetization opportunities while deepening integration within client operations[ S1; S2 ].

Such technology enhancements enable more seamless benefits enrollment processes, self-service functionality for employees and managers alike, and tighter data analytics supporting risk management.

These ongoing upgrades provide differentiation by improving client retention rates through enhanced experience while also supporting scalable cost structures by reducing manual intervention needs.

Risk Landscape: Cybersecurity, Legal Exposure, and Policy Uncertainties

Given its role as custodian of sensitive employee data spanning health records through payroll details, cybersecurity forms a critical pillar of TriNet's risk governance framework. The company operates a defense-in-depth strategy that includes a Security Risk Management Program modeled on leading frameworks such as NIST.[ S1 ] Leadership from the Chief Security Officer ensures enterprise-wide coordination supported by an incident response team capable of rapid investigation escalation should breaches be suspected.

Additionally, third-party vendor risks are actively monitored through internal assessment protocols reflecting multi-layered controls that align with enterprise risk management priorities.[ S1 ] Despite these measures no material cybersecurity incidents were reported as impacting business strategy or operations through year-end 2025.

Legal risk associated with compliance failures or interpretive disputes remains salient given evolving labor laws nationwide coupled with industry-specific considerations affecting client sectors.[ S1 ] Maintaining robust oversight is therefore integral not just for regulatory adherence but also reputational safeguard.

Analyzing Market Sentiment: Recent Earnings and Investor Reactions

TriNet’s fourth-quarter results reported on February 12th, 2026 beat estimates driven by stronger-than-expected revenue stability yet tempered by continued margin pressures attributable partly to restructuring investments[ N1; N2 ]. Analysts cite valuation dislocation labeling the stock “oversold,” highlighting an opportunity gap relative to fundamentals perceived as undervalued given durable customer relationships and recurring contracts[ N3 ].

Dividend yields recently exceeded the psychologically relevant threshold of 2%, attracting yield-focused investors hunting income sources amid low interest rate environments[ N4; N9 ]. Simultaneously options activity has been notable for strategies aimed at boosting yield via covered calls or put writing designed around underlying equity exposure[ N5; N6; N7; N8 ], reflecting sophisticated investor engagement adapting payoff profiles.

Strategic Pathways: Capital Structure, Restructuring, and Growth Initiatives

The company’s capital structure incorporates a $700 million revolving credit facility with amendments extending capacity or terms supplemented by senior unsecured notes totaling $900 million maturing during fiscal years ending March 2029 ($500M notes) and August 2031 ($400M notes)[ S2 ]. This mix provides strategic financial flexibility enabling ongoing investments even during restructuring phases discussed extensively in MD&A disclosures.[ S2 ] Restructuring actions focus on streamlining overhead while aligning workforce capabilities closer to growth initiatives primarily centered on technology innovation and broadened product offerings deserving enhanced go-to-market emphasis.[ S1; S2 ]

Stock-based compensation represents a consistent part of total operating costs reflecting efforts at talent retention critical within the tech-enabled services sector triaging innovation while controlling expenses carefully.[ S1 ]

Management outlook remains cautiously optimistic about expanding client penetration within large addressable markets driven by demand from SMBs needing sophisticated yet affordable human capital management solutions.[ S1 ]

Investment Implications: Moat Durability Amid Macro and Regulatory Shifts

TriNet’s enduring competitive moat stems from leveraging deep regulatory expertise embedded within its PEO co-employment model combined with scale advantages fueling comprehensive bundled human resource outsourcing solutions uniquely adapted for SMBs.[ S1; F1 ] The intricate overlay of federal employment laws alongside state-level mandates means replicating these offerings independently presents formidable operational challenges without similar infrastructure investments.

However an inflationary cost backdrop alongside rising compliance expenditures continue exerting margin compression risks visible across recent fiscal periods,[ S1 ] suggesting profitability enhancements require continued focus on efficiency gains including automation adoption.

Macro-economic uncertainties including shifts in labor market dynamics or benefit cost inflation further reinforce volatility potential necessitating agile management responses. Nonetheless sustained growth prospects anchored on technology-driven platform scalability offer avenues for margin expansion over time provided regulatory complexity does not meaningfully increase compliance burdens beyond forecasted levels.[ N3 ]

In sum, TriNet navigates a delicate balance between leveraging complex regulatory structures advantageous for competitive differentiation while striving diligently to contain operational costs amid evolving macro-financial conditions shaping investor sentiment today.

This analysis is based solely on publicly available information including SEC filings dated February 12th, 2026 (Form 10-K), quarterly filings (Form 10-Q), Nasdaq news reports dated January–February 2026 together with company facts data extracted from XBRL SEC databases. It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments