Tesla's Strategic Pivot and Market Dynamics Amidst Shifting EV and AI Frontiers

Tesla navigates a complex automotive and AI landscape, balancing production shifts with ambitious AI-driven mobility initiatives.

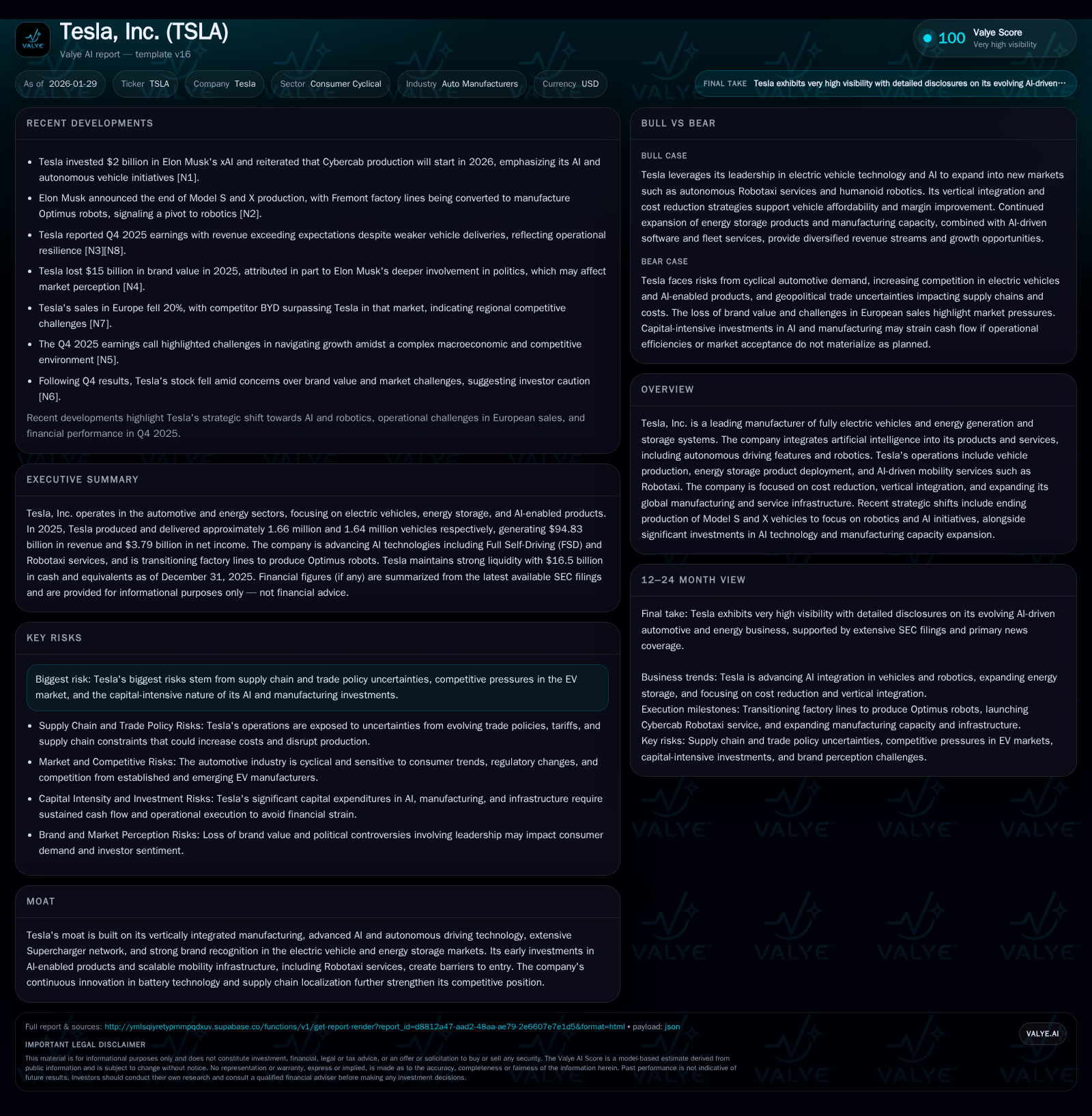

Tesla recently reported revenue exceeding analyst expectations despite a slowdown in vehicle deliveries, reflecting evolving operational priorities and market pressures [N1]. The company is undertaking a strategic pivot by ceasing Model S and X production to focus resources on robotics and AI, notably its Robotaxi program, while expanding manufacturing footprint and investing heavily in battery technology and AI capabilities [valye_report_excerpt]. Tesla’s vertically integrated model and early AI investments underpin a strong competitive position in electric vehicles and mobility services, though supply chain challenges and intensifying competition remain critical risks. Close attention is warranted on Tesla’s execution in scaling new AI-driven revenue streams and managing cost pressures amid a capital-intensive transition.

What Changed Recently

Tesla’s Q4 2025 earnings revealed a nuanced picture: revenue beat consensus with approximately $24.5 billion, yet vehicle deliveries were softer than expected [N1, N3, N8]. This divergence points to a more complex revenue mix beyond unit sales, including energy storage and AI-driven services. Market reaction was mixed, with shares declining and brand value assessments signaling caution about near-term challenges [N2, N14]. Tesla also announced the discontinuation of Model S and Model X production to pivot towards robotics and AI platforms, notably its autonomous Robotaxi ambitions [valye_report_excerpt]. This represents a strategic reallocation of capital and engineering talent away from legacy flagship vehicles towards emerging mobility and AI ecosystems.

The company continues to aggressively expand manufacturing capacity globally, aiming to localize supply chains and enhance cost efficiency amid ongoing geopolitical and macroeconomic headwinds [valye_report_excerpt]. Battery technology advancements and cell production scale were emphasized as critical to meeting future demand and improving unit economics [N7]. The earnings call highlighted Tesla’s focus on managing growth amidst these operational shifts, signaling a transitional phase with potential volatility in deliveries and margins [N3, N6].

Business Model as a System

Tesla operates as an integrated technology and manufacturing platform centered on electric vehicles (EVs), energy storage, and AI-driven mobility solutions. Its vertically integrated system encompasses: vehicle design and assembly, proprietary battery cell production, software development for autonomous driving, and an expanding network of charging infrastructure [S1-S7]. Vehicle sales remain the primary revenue driver but are increasingly complemented by energy products and software-enabled services.

The cessation of Model S and X production reflects Tesla’s strategy to streamline its product lineup, freeing capacity and R&D resources to accelerate AI and robotics innovation [valye_report_excerpt]. This shift underscores Tesla’s view of future mobility as a software-led platform leveraging autonomous vehicle technology and data monetization, particularly through Robotaxi services. The company’s AI stack integrates real-time vehicle data, advanced neural networks, and simulation to improve driving autonomy—a critical moat difficult for competitors to replicate quickly.

Manufacturing efficiencies benefit from Tesla’s integrated Gigafactory model combining battery and vehicle assembly under one roof, reducing logistics complexity and enabling rapid iteration [S4, S6]. Tesla’s direct-to-consumer sales and service model allows for customer engagement feedback loops and margin retention without traditional dealership overheads. The energy segment, including solar and stationary storage, leverages shared lithium-ion technology, diversifying revenue and smoothing cyclicality.

Capital deployment prioritizes expanding production footprints near key markets, battery R&D, AI development, and infrastructure build-out. Tesla’s capital intensity is substantial, reflecting both hardware manufacturing and software platform scale requirements [S8, S10]. The company’s balance sheet shows robust liquidity and asset base, supporting ongoing investment while managing working capital needs.

Industry Map & Competitive Battlefield

Tesla sits at the intersection of several converging industries: traditional automotive manufacturing, energy storage, and AI-powered mobility services. The core competitive set includes legacy automakers rapidly electrifying fleets, pure EV startups, battery suppliers, and technology firms advancing autonomous driving and AI systems.

In EV manufacturing, Tesla’s early-mover advantage combined with vertical integration and battery technology leadership creates a durable position. However, competitors from Volkswagen, GM, Hyundai, and Chinese OEMs aggressively scale EV models with significant government support, compressing market share and pricing power. Tesla’s direct sales model and brand reputation remain differentiators but face growing scrutiny as new consumer choices emerge.

In autonomous mobility, Tesla attempts to leapfrog competitors by deploying AI at scale through its extensive vehicle fleet data and in-house neural network training. This approach contrasts with other players relying on expensive lidar sensors and incremental partnerships. The Robotaxi concept aims to open a new revenue frontier, competing against ride-hailing incumbents and emerging autonomous fleets, though regulatory, technological, and consumer acceptance hurdles persist.

Energy storage and generation markets are also competitive, with firms like LG Chem, Panasonic, and Sonnen vying for residential and grid-scale battery deployments. Tesla’s integration with its automotive batteries and solar products offers cross-selling opportunities but requires balancing focus and capital.

Supply chain dynamics remain complex, given the concentrated raw material sourcing for lithium, cobalt, and nickel. Tesla’s moves to localize supply and develop proprietary cell chemistries strive to mitigate volatility and geopolitical risk.

Where the Economics Become Real

Tesla’s unit economics hinge substantially on battery cost per kilowatt-hour, manufacturing throughput, and software monetization. Battery cost reductions drive gross margin expansion and enable more affordable vehicle pricing, critical for scaling volume in price-sensitive markets. Tesla’s Gigafactory model and investments in cell chemistry innovation aim to sustain a declining cost curve.

Manufacturing efficiency gains through automation and vertical integration reduce per-unit labor and logistics costs. However, the transition to new product architectures for robotics and AI platforms introduces upfront complexity and capital expenditure, pressuring margins in the near term.

Software and AI services, including Full Self-Driving (FSD) subscriptions and Robotaxi deployment, offer high incremental margins once development and infrastructure are established. These services could shift Tesla’s revenue mix towards recurring, scalable income streams, improving overall profitability leverage.

Tesla’s capital intensity is notable, with significant R&D and capex spending required to maintain technology leadership and capacity growth. Maintaining healthy liquidity and managing working capital cycles are critical to fund these investments without dilutive financing.

Supply chain bottlenecks, such as raw material availability and semiconductor shortages, remain key constraints that can delay production ramp-ups and increase costs. Tesla’s focus on supply chain localization and direct material sourcing aims to alleviate these pressures but requires execution discipline.

Diligence Questions / Disconfirming Signals

- How effectively can Tesla transition engineering and manufacturing resources from legacy Model S and X lines to robotics and AI platforms without disrupting core vehicle production?

- What is the timeline and regulatory risk profile for scaling Robotaxi services, and how dependent is this on breakthroughs in autonomous driving safety and consumer acceptance?

- To what extent can Tesla sustain its unit cost improvements amid macroeconomic inflationary pressures on raw materials and labor?

- How will increasing competition from established automakers and new entrants impact Tesla’s pricing power and market share, especially in China and Europe?

- Are there vulnerabilities in Tesla’s supply chain localization strategy, particularly concerning geopolitical tensions and rare earth material availability?

- How robust is Tesla’s software monetization model in driving predictable, recurring revenue, and what risks exist around regulatory scrutiny or technology adoption?

- What are the implications of Tesla’s capital intensity on free cash flow generation in the medium term, especially if growth slows or new product launches face delays?

- How does Tesla’s brand perception volatility post-earnings reflect underlying operational or strategic risks that could affect long-term positioning?

This analysis is based on publicly available information and industry context as of January 2026. It does not constitute financial advice or investment recommendations. The future performance of Tesla depends on multiple uncertain factors including market conditions, regulatory environment, and execution capabilities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments