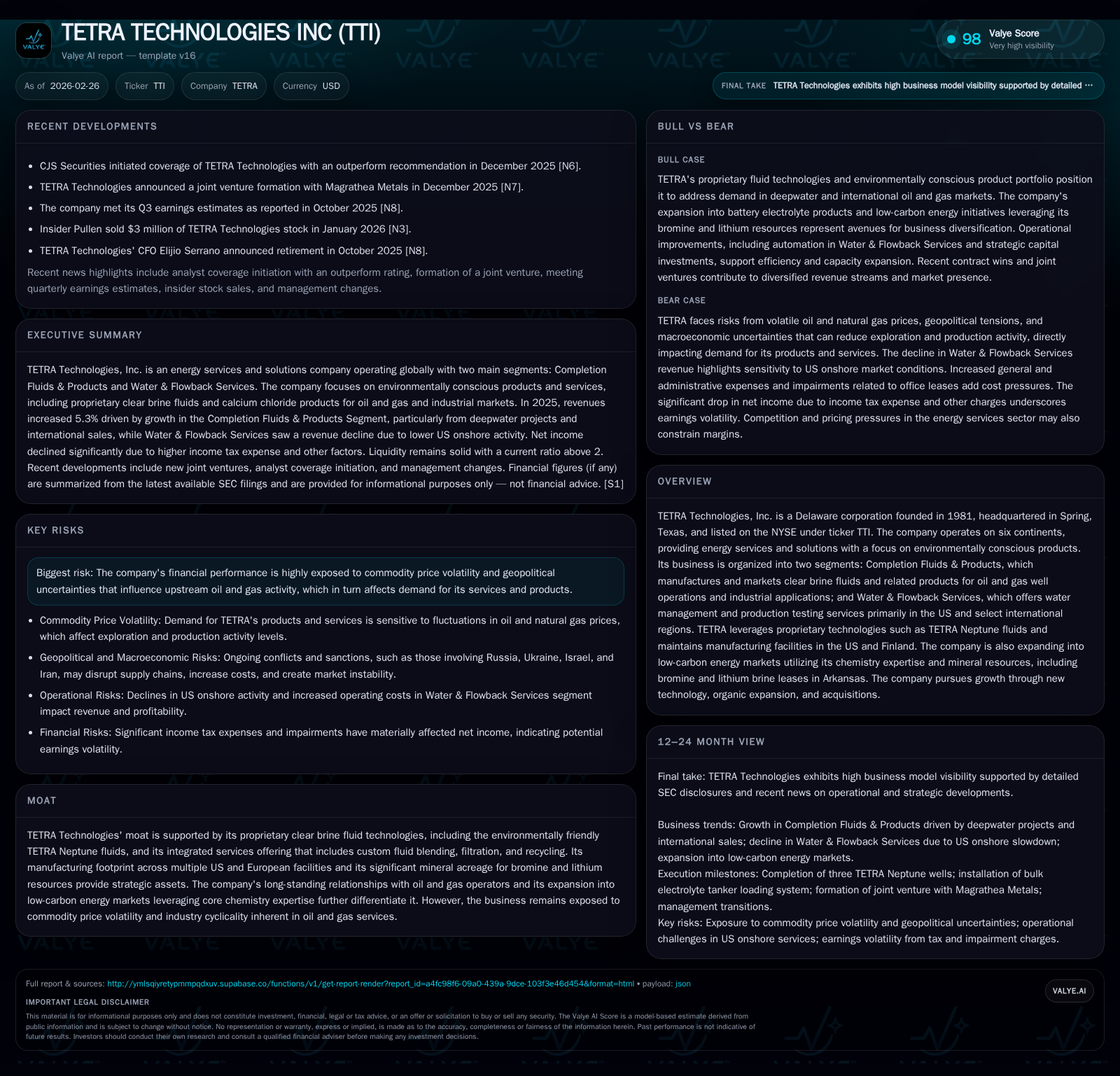

TETRA Technologies Advances Low-Carbon Energy Solutions Amid Oilfield Services Evolution

TETRA leverages proprietary fluids and mineral assets to fuel growth while adapting to energy market shifts.

In 2025, TETRA Technologies expanded its Completion Fluids & Products segment through deepwater projects utilizing its proprietary Neptune fluids, driving a notable revenue and operating income increase despite challenges in Water & Flowback Services. Strategic investments in bromine processing and electrolyte technology underscore the company's push into low-carbon energy markets, supported by solid cash flow and a stable capital structure. Market volatility linked to commodity prices and geopolitical tensions remains a key risk, with ongoing monitoring essential. Near-term catalysts include scaling battery electrolyte production and international contract renewals.

Rebounding Revenues: Examining 2025’s Operational Drivers

TETRA Technologies demonstrated resilient growth in 2025, recording consolidated revenues of approximately $631 million, a modest increase of 5.3% over 2024 [F1][S1]. This was principally propelled by the Completion Fluids & Products segment, which surged by 20.9% to roughly $376 million, largely on the back of three deepwater well completions in the Gulf of America deploying proprietary high-margin TETRA Neptune clear brine fluids (CBFs), alongside an inaugural multi-well contract in Brazil [S1][S5]. These Neptune fluids are engineered as environmentally friendly alternatives to traditional zinc bromide or cesium formate completion fluids, offering both enhanced operational performance and sustainability – a key differentiator for offshore applications during increasing regulatory scrutiny.

While consolidated operating income expanded by 11% year-over-year to about $55 million, the operating income growth was even more pronounced within the Completion Fluids segment at +32.9%, reflecting improved product mix and industrial calcium chloride business strength [F1][S5]. This operating leverage was partially offset at the corporate overhead level by increased professional fees and insurance expenses.

Despite higher revenues, net income dramatically declined by over 97% due largely to non-recurring tax adjustments and increased tax expense from shifts such as the change in Brazilian subsidiary tax classification [F1][S1]. Operating cash flow painted a more robust picture with an exceptional 174.8% increase to over $100 million, underscoring strong working capital management particularly within high-margin offshore operations [F1][S7].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 3 | 100 | 81 | -97.2% |

| 2024 | 108 | 37 | 61 | +320.0% |

| 2023 | 26 | 70 | 38 | +228.9% |

| 2022 | 8 | 19 | 40 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 20 | 1.1 |

| 2024 | -24 | 42.5 |

| 2023 | 32 | 17.4 |

| 2022 | -21 | 7.3 |

Source: SEC companyfacts cache [F1].

Table reflects key annual financial metrics sourced from SEC filings [F1]

Dissecting Segment Performance: Completion Fluids Surge vs. Water & Flowback Headwinds

The bifurcated performance across TETRA's two main segments highlights sector-specific dynamics faced during the year [S5][S17]. The Completion Fluids & Products segment capitalized on Neptune fluids' market acceptance especially for deepwater wells—a niche demanding sophisticated CBF blends free of undissolved solids and environmentally sensitive components. This translated into higher gross profits (+26.8%) and operating incomes (+32.9%), supported additionally by international expansion through higher brominated product sales in Europe and robust calcium chloride industrial volumes.

Conversely, Water & Flowback Services faced a tougher environment as U.S onshore activity decelerated alongside divestiture of early production units in Latin America, causing revenues to contract around 11.6%. Profitability in this segment suffered more acutely due to fixed costs and inflationary pressures despite automation advancements implemented to reduce operating expenses [S1][S17]. However, late-year contract wins in Argentina signal tentative stabilization efforts outside the United States.

Notably, TETRA’s use of advanced filtration technologies at customer sites facilitates recovery and recycling of used CBFs, reducing waste disposal footprint while enriching service offering—an operational tactic vital to sustainability-focused clients [S8].

Strategic Investments and Capital Allocation Supporting Growth and Sustainability

Capital expenditure commitments escalated significantly by one-third to nearly $81 million during 2025, evidencing TETRA's ambition beyond legacy oilfield services into critical mineral development [F1][S6]. The lion's share ($59.8 million) funded phase one engineering and completion of a bromine processing plant in Arkansas—a strategic move aligning with growing demand for battery-grade chemicals including zinc bromide blends sold under the TETRA PureFlow brand.

Investments also extended across the U.S. and European manufacturing footprint supporting capacity enhancement for both conventional CBFs and emerging low-carbon electrolyte products designed for energy storage markets [S10][S15]. Water & Flowback Services capex totaled $21 million focused chiefly on fleet modernization through deployment of the SandStorm fracturing flowback units augmented with automation tech.

Financially, TETRA maintained a balanced approach between expansionary spending and liquidity preservation benefiting from improved operating cash flows offsetting capex increases [F1][S7]. The company has not engaged in meaningful share repurchases recently but continues modest dividend distributions consistent with prudent capital allocation in volatile commodity cycles [S21][S23].

Navigating Macro Risks: Commodity Volatility and Geopolitical Uncertainty

Embedded within TETRA’s business model is heightened exposure to upstream oilfield investment cycles inherently tied to crude oil and natural gas price fluctuations [S2][S4][S18]. Volatility stemming from geopolitical tensions—including Russia-Ukraine conflicts and Middle East unrest—injects additional uncertainty through supply chain constraints, sanctions-driven counterparty risks, shipping disruptions notably around the Strait of Hormuz, and potential inflationary cost shocks.

These macro factors contribute directly to variations in exploration & development capex from operators influencing demand for TETRA’s completion fluids and water management services globally [S19]. While no precise short-term impact estimates are provided by management, ongoing monitoring is emphasized given recent volatility trends.

Growth Outlook: Leveraging Core Chemistry toward Low-Carbon Markets

Looking forward, TETRA aims to capitalize on its chemistry prowess underpinning its proprietary brine fluids alongside its sizable mineral acreage holding some ~40,000 gross acres rich in bromine and lithium resources located primarily in Arkansas [S1][S15]. These assets represent foundational inputs enabling production of electrolytes tailored for next-generation battery technologies.

The installation of an advanced bulk electrolyte tanker loading system at West Memphis will facilitate scaling production volumes necessary for clients such as Eos Energy Enterprises whose ramp-up schedules are expected to materially enhance revenue streams related to TETRA PureFlow Plus battery electrolytes starting early 2026 [S1]. This marks a pivotal strategic pivot incorporating sustainability principles within core operations while addressing clean energy demand increase.

Expanding revenue bases beyond conventional hydrocarbon-centric applications leverages unique competitive advantages rooted in integrated chemical manufacturing processes combined with industry relationships built over decades.

Financial Health Snapshot: Cash Flows, Debt Profile, and Dividend Policy

TETRA closed out fiscal year-end with approximately $72.6 million in unrestricted cash complemented by credit facilities totaling around $148 million (now partly expired delayed-draw provision) yielding overall liquidity approximately $220 million at December 31, 2025 [F1][S7][S28]. This solid liquidity position supports operational resilience amid uncertain macroeconomic conditions.

Leverage metrics have been managed prudently with net interest expense declining nearly 23% due partly to higher capitalization of interest related to slow-moving Arkansas capital projects alongside lower benchmark rates on credit facilities [F1][S7]. Return on equity stood near a modest ~1.1% reflective of net income impacts from taxation shifts but backed by improving underlying operating profitability.

Dividend payments persist at moderate levels aligning with conservative broader capital allocation priorities; however, no formal share repurchase programs have been pursued recently minimizing free cash flow distribution risks during volatile cycles [F1][S21].

Analyst Takeaway: What to Watch in the Coming Quarters

Investors should track several key developments including progress updates on deepwater projects employing Neptune CBFs which materially contribute outsized margins relative to standard fluids offerings [N4][N3]. Additionally, scaling commercialization of low-carbon electrolyte products tied intricately to client product ramp-ups represents a nascent but potentially transformative growth avenue closely entwined with critical minerals extraction efficiency.

Given continued commodity price fluctuations influenced by geopolitical events indicated earlier this presents both upside opportunities if upstream capex rebounds or downside risks if operator spending contracts further impacting segment profit mixes across Completion Fluids vs Water Services segments.

Working capital optimization remains a focal point for operational enhancements likely boosting free cash generation capacity potentially redeployable into further strategic ventures or shareholder returns.[N1]

Continued diversification efforts geographically—bolstering revenues via contracts secured in Argentina—and technology deployment aimed at automation will be telling markers for management’s ability to counteract regional softness within U.S onshore markets [N3][N4].

This analysis is based solely on publicly available company filings and disclosures as referenced without extrapolation or speculative forecasts intended for general informational purposes only.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments