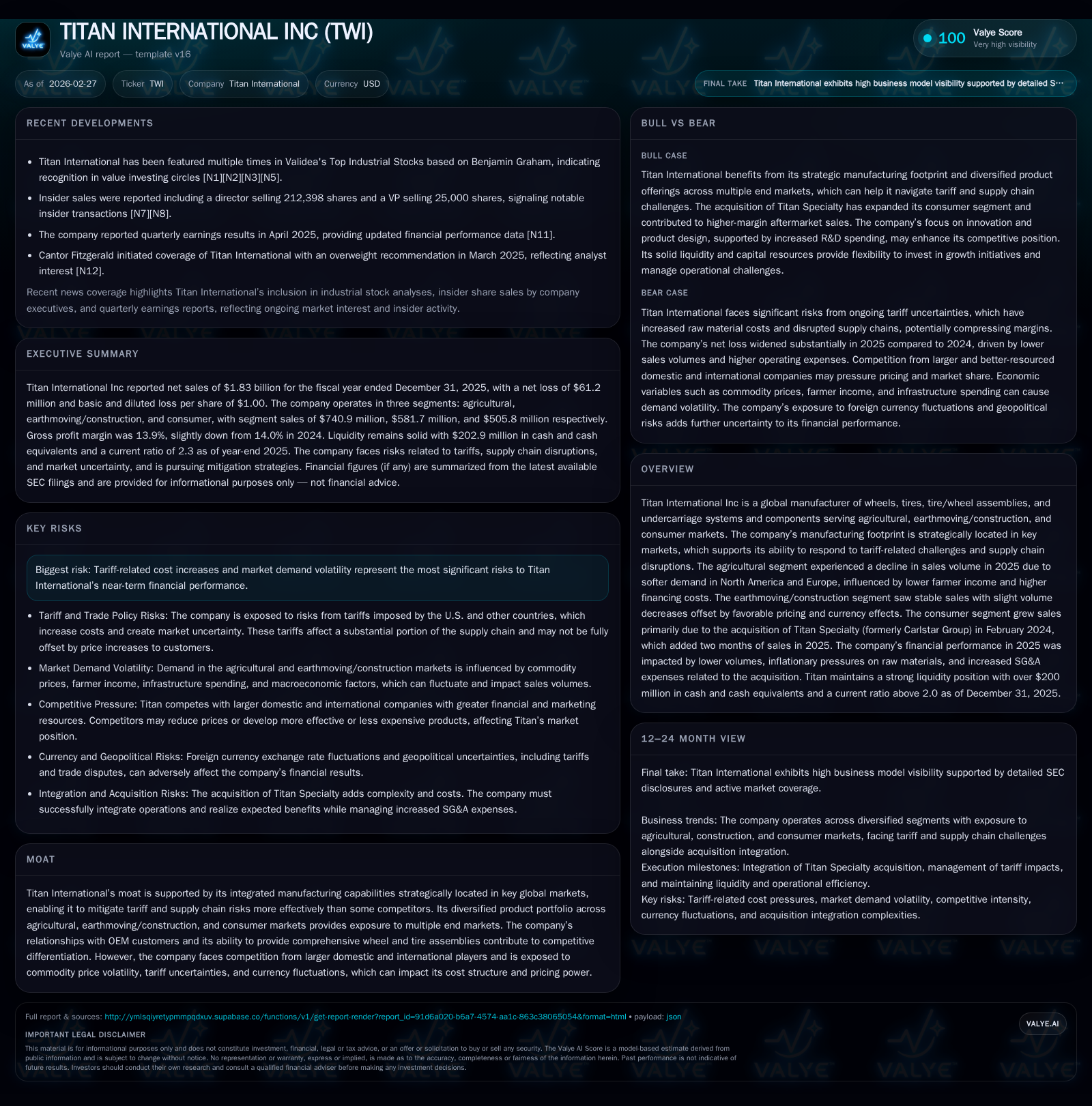

Titan International’s Strategic Maneuvers Amid Tariff Shocks and Market Volatility

Titan’s 2025 financials reflect the complex interplay of its Carlstar acquisition, tariff-driven cost pressures, and uneven segment demand.

Titan International expanded revenue notably in 2025 following its February 2024 acquisition of Carlstar (renamed Titan Specialty), which contributed additional sales volume and broadened its consumer product offerings. However, profitability suffered a significant contraction, with operating income declining over 37% and net income swinging to a sizable loss driven largely by cost inflation and volume softness in agricultural and earthmoving sectors amid tariff uncertainties. Cash flow generation weakened sharply, constrained by elevated input costs and lower operational leverage, while the company maintained liquidity through revolving credit and manageable debt covenants. Going forward, tariff volatility, commodity price swings, and integration execution remain key variables influencing Titan’s financial trajectory.

Historic Revenue Expansion Fueled by Strategic Acquisition

Titan International reported consolidated revenue growth of approximately 19% year-over-year for FY2025, reaching about $1.83 billion[F1]. This increase primarily reflects the February 29, 2024 acquisition of Carlstar Group (now Titan Specialty), which contributed roughly two months of additional sales in 2025, particularly bolstering the consumer market segment[S1, S2]. Organic sales volume trends varied across segments during mixed market conditions.

Segment-Specific Sales Trends Highlight Mixed Market Demand

The agricultural segment experienced volume declines driven by softer farmer incomes influenced by volatile commodity prices and higher financing costs within an uncertain global tariff environment[S1]. Demand for large agricultural products softened notably in North America and Europe, while smaller agricultural product demand held relatively steadier. The earthmoving/construction segment maintained relatively stable revenues as pricing gains offset volume decreases, supported by favorable commodity market conditions[S1]. The consumer segment showed strong growth fueled by Titan Specialty's product offerings including specialty tires for powersports and outdoor power equipment[S1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -63 | 30 | 21 | 55 | -1042.0% |

| 2024 | -6 | 141 | 33 | 66 | -107.1% |

| 2023 | 79 | 179 | 149 | 61 | -55.3% |

| 2022 | 176 | 161 | 206 | 47 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | -25 | -12.3 | |

| 2024 | 76 | -1.1 | |

| 2023 | 33 | 119 | 16.9 |

| 2022 | 25 | 114 | 46.2 |

Source: SEC companyfacts cache [F1].

Tariff Environment as a Persistent Constraint on Margins

Reciprocal tariffs imposed since April 2025 have increased raw material costs—particularly steel and rubber—impacting manufacturing expenses despite Titan’s strategically located facilities mitigating some supply chain disruptions[S1, S14]. The company faced inflationary pressures that outpaced the ability to fully pass through these costs to customers.

Operational Profit Compression: What's Pressuring Earnings?

Operating income decreased by approximately 37.4%, falling from $33.2 million in FY2024 to $20.8 million in FY2025[F1]. Net income shifted from a loss of $5.6 million in FY2024 to a larger loss of $63.5 million in FY2025[F1], reflecting acquisition-related expenses from the Titan Specialty deal, increased selling/general & administrative expenses related to expanded operations, lower fixed cost absorption at reduced volumes, and continued raw material inflation.

Operating cash flow declined sharply by nearly 79% year-over-year to about $30 million in FY2025 from $141 million previously, indicating working capital challenges under current market conditions[F1]. Capital expenditures decreased roughly 17% to $54.6 million but remained substantial given investments into productivity improvements[F1, S17]. This resulted in free cash flow turning negative by an estimated $24.6 million.

Capital Structure Overview and Liquidity Position

Titan remains compliant with all covenants tied to its $400 million principal amount of 7.00% senior secured notes due in 2028—guaranteed by key subsidiaries—and maintains a $225 million revolving credit facility secured against accounts receivable and inventory[S4, S5, F1]. As of December 31, 2025, borrowings under the revolving credit facility totaled approximately $156 million with about $36 million available for additional draws[S7, S9, S10, F1]. The weighted average interest rate on debt stood at roughly 5.78%, reflecting SOFR-based pricing.

Liquidity remains strong with nearly $203 million in cash and equivalents at year-end—mostly held offshore—to support working capital needs alongside planned capital expenditures between $50 million and $55 million for fiscal year 2026 focused on facility upgrades and tooling enhancements[S8, S9, F1].

Investments, Cash Flow Dynamics, and Shareholder Returns

Despite top-line growth, free cash flow turned negative due to reduced operating cash flows coupled with sustained capital spending aimed at productivity gains[F1, S17, S15]. Dividends were suspended after 2020 with none paid through FY2025[F1, S15]. A prior share repurchase program concluded during calendar year 2025 after buybacks totaling approximately $58 million over recent years[F1, S15].

Forward-Looking Indicators and Key Risks on the Horizon

Management highlights mid- to long-term support from global population growth driving replacement demand for agricultural equipment but remains cautious due to near-term tariff impacts inflating input costs unpredictably[S1, S14, S2]. Currency fluctuations add complexity given international operations.

Agricultural demand is vulnerable to weather variability, subsidy changes, used equipment markets, interest rates affecting financing availability—all within an opaque tariff policy environment influencing farmer sentiment globally[S1, S14]. The earthmoving/construction business benefits modestly from mining capital spending increases but is influenced heavily by GDP trends and infrastructure spending patterns across key regions.

Competitive pressure persists as larger OEMs may internalize wheel/tire assembly production or source alternatives competitively[S1, S14]. Monitoring tariff pass-through effectiveness alongside integration progress of Titan Specialty brands will be critical.

This analysis is based solely on publicly available SEC filings dated up to February 27, 2026 , , related exhibits, and historical financial disclosures without offering investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments