Texas Instruments’ Bold Silicon Labs Acquisition Amid Semiconductor Industry Turmoil

Assessing TXN's strategic positioning, innovation pipeline, and risk exposures as it undertakes a transformative $7.5 billion acquisition amidst mixed earnings and volatile markets.

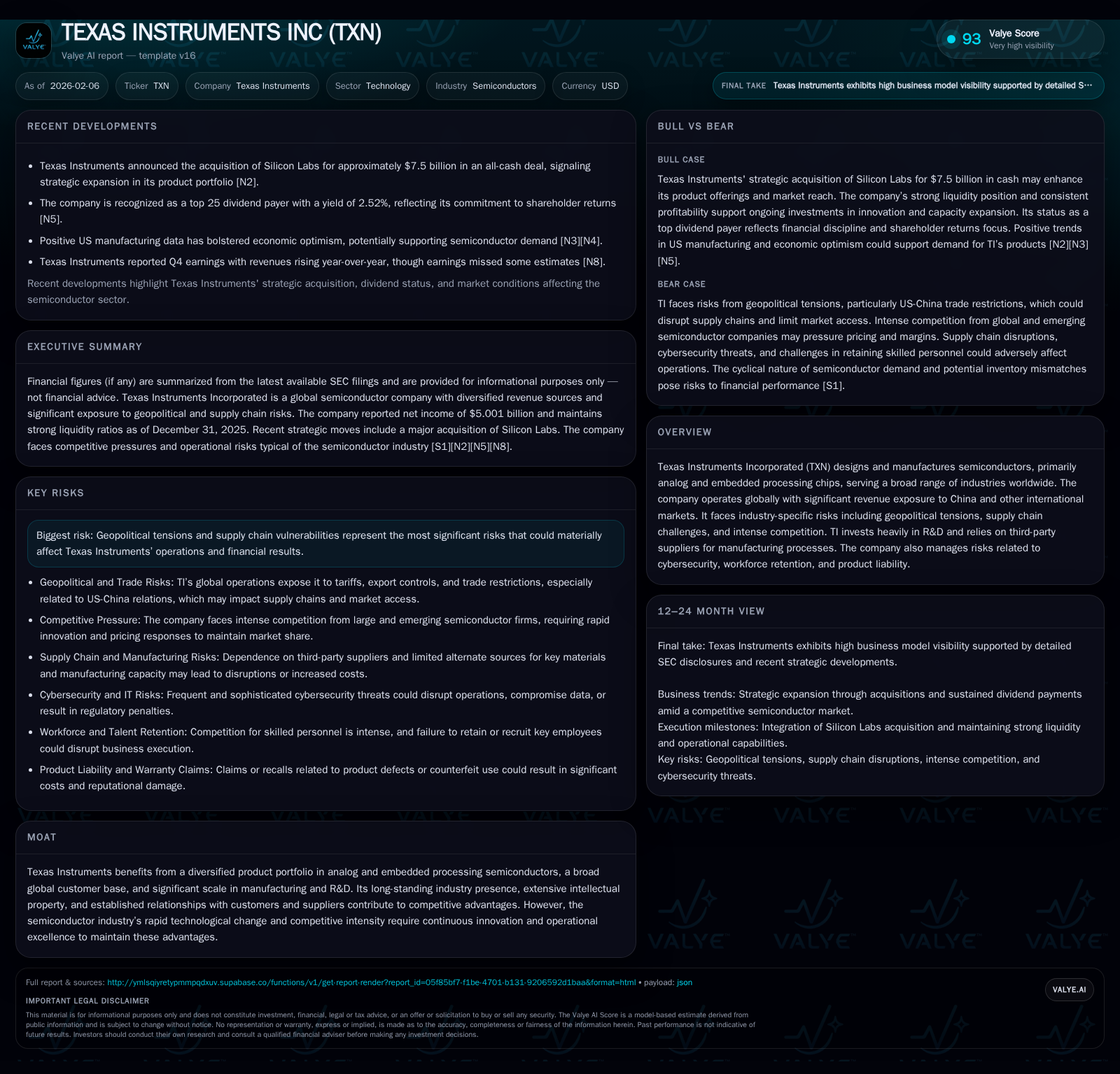

In early 2026, Texas Instruments (TXN) undertook a significant $7.5 billion all-cash acquisition of Silicon Labs, signaling an aggressive strategic expansion in its analog and embedded processing portfolio amid growing competitive pressures and geopolitical headwinds. This deal unfolds against the backdrop of a recent quarterly earnings miss that dampened investor sentiment amidst a broad semiconductor selloff. While TI’s large-scale manufacturing footprint, diversified customer base, and robust R&D spending underpin its competitive moat, ongoing risks linked to China revenue exposure and supply chain complexities demand vigilant management. Looking forward, TI’s blend of targeted innovation—especially in automotive autonomy chips—and disciplined capital allocation will be critical to sustaining its market leadership amid intensifying global competition and shifting industry dynamics.

A Strategic Gamble: The Silicon Labs Acquisition

Texas Instruments’ announcement on February 4th, 2026, to acquire Silicon Labs in an all-cash transaction valued near $7.5 billion represents a bold bet within a volatile semiconductor landscape [N1]. This deal signals TI’s intent to reinforce its footprint in the analog and embedded processing segments—markets central to its core strengths but increasingly contested amid rapid technological evolution. Silicon Labs brings complementary product lines particularly well-regarded for wireless connectivity solutions integrated into IoT applications, thus potentially expanding TI's addressable markets.

Market reaction favored Silicon Labs shareholders who saw a premium offer lifting their stock value sharply on announcement day [N10]. For TI, although the acquisition fuels optimism about accelerating product portfolio diversification and scale synergies, it also introduces typical M&A risks noted previously in regulatory disclosures—ranging from integration complexities to execution timing challenges [S1]. This strategic move aligns with efforts to counterbalance intensifying competition from well-resourced rivals leveraging government incentives globally.

Financial Performance and Market Expectations: Navigating a Missed Quarter

TI reported Q4 2025 financial results that missed analyst expectations on earnings per share despite posting year-over-year revenue growth—an outcome reflecting margin compression across product lines [N3][F1]. This modest underperformance coincided with broad-based technology sector weakness amplifying market volatility and investor caution [N9]. Analysts debated whether the stock represented a buying opportunity amidst cyclical softness or warranted further scrutiny given prevailing headwinds [N11].

Examining financial metrics reveals sustained profitability with net income near $5 billion for the calendar year ending 2025 but suggests pressures on free cash flow margins have begun reshaping capital return narratives [F1][N5]. These dynamics underscore the challenge of balancing aggressive investment—such as the Silicon Labs acquisition—with maintaining disciplined operational efficiency during economic uncertainty.

Moat Dynamics: TXN’s Product Portfolio and Manufacturing Scale in Focus

TI’s enduring competitive advantage arises from its extensive analog semiconductor portfolio paired with embedded processing capabilities deeply integrated across diverse industries—from industrial automation to communications infrastructure [valye_report_excerpt]. Its massive scale allows for cost efficiencies in production while enabling substantial R&D investment fostering consistent innovation.

However, regulatory commentary highlights that technological advancements by competitors coupled with pricing pressures threaten this moat's durability unless TI continues rapid development cycles and operational agility [S1]. The company’s long-term relationships with global suppliers and customers form an additional barrier to entry but require constant nurturing as industry disruption accelerates.

Geopolitical and Supply Chain Risks: The China Factor and Beyond

Significant risk emanates from TI’s dependence on China—close to one-fifth of revenue originates directly from Chinese customers' headquarters while shipment exposure reaches approximately half of their total sales volume [S1][valye_report_excerpt]. Rising geopolitical tensions between the U.S. and China introduce unpredictability through tariffs, export restrictions, and trade sanctions affecting supply chains and market access.

Further complicating matters are global supply chain fragilities accentuated by fluctuating macroeconomic climates, potential disruptions due to political conflict or public health crises, all of which add layers of operational volatility for multinational manufacturers like TI [S1]. Proactive risk mitigation strategies remain essential given these persistent uncertainties.

Innovation at the Core: R&D Investments Driving TI’s Future Growth

Amid these external pressures, Texas Instruments consistently prioritizes R&D as foundational to sustaining technological leadership within analog semiconductors—a strategy reinforced by recent unveiling of advanced automotive chips tailored for autonomous vehicles [N8][valye_report_excerpt]. These products target burgeoning applications where sensor fusion, power management, and reliable embedded processing are indispensable.

This commitment aligns with broader trends toward digitization across automotive manufacturing, industrial equipment modernization, and smart infrastructure development. Constant innovation cycles enable TI not only to defend legacy markets but also opportunistically penetrate segments experiencing rapid growth driven by smart technologies.

Emerging Markets & End Customer Diversification: Strengths and Vulnerabilities

TI services an array of sectors—including industrial machinery, automotive electronics, personal electronics—and owns diversified geographies spanning over 30 countries [S1][valye_report_excerpt]. Approximately 60% of revenue comes from non-U.S. customers providing some insulation against domestic cyclical downturns. Yet this breadth introduces uneven demand swings tied to end-market cyclicality.

Volatility in economic conditions influencing sectors such as automotive production rates or consumer electronics consumption creates asymmetrical pressure points across different parts of TI’s portfolio. Managing this complexity requires nimble supply chain adjustments combined with selective capital deployments targeting areas with higher anticipated growth rates while pruning less profitable segments.

Competitive Pressures and Industry Evolution: Staying Ahead or Playing Catch-Up?

The semiconductor industry is increasingly characterized by fierce rivalry intensified by Asian competitors benefiting from government-backed incentive programs aimed at building domestic chipmaking champions. Chinese policy initiatives specifically heighten competition risks as they funnel significant funding into local players focused on analog semiconductors—the cornerstone of much TI business [S1][valye_report_excerpt].

Additionally, consolidation trends among major players globally reshape competitive dynamics by concentrating market power but also pressuring pricing models downward. This environment demands continual operational refinement alongside accelerated innovation cadence just to maintain parity.

Cash Flow and Capital Efficiency: Examining Investment Discipline Trends

A notable development is the observed contraction in free cash flow margins starting late 2025 even as TI maintains strong overall liquidity—with over $3.2 billion held in cash equivalents—and a robust current ratio exceeding 4x suggesting short-term financial stability [F1][N5].

Capital allocation choices reflecting elevated spending on acquisitions (notably Silicon Labs), plant expansions, and R&D signify aggressive positioning though raise questions regarding margin sustainability if top-line growth falters amid broader tech deceleration. Vigilant cost control paired with disciplined investment prioritization will be pivotal.

In summary, Texas Instruments enters 2026 navigating an intricate mix of bold strategic expansion via the Silicon Labs acquisition tempered by near-term financial softness against an unforgiving geopolitical backdrop punctuated by China-related risks. The company’s entrenched operational scale and commitment to innovative product development underpin its competitive moat but require relentless focus amid mounting global pressures intensified by subsidy-fueled Asian challengers. While liquidity remains healthy supporting growth initiatives, evolving market demands highlight the need for nimble execution balancing capital discipline with forward-looking innovation investments.

This analysis synthesizes available reported facts without expressing investment recommendations or price forecasts.

Disclaimer: This report is for informational purposes only and does not constitute investment advice or endorsement.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments