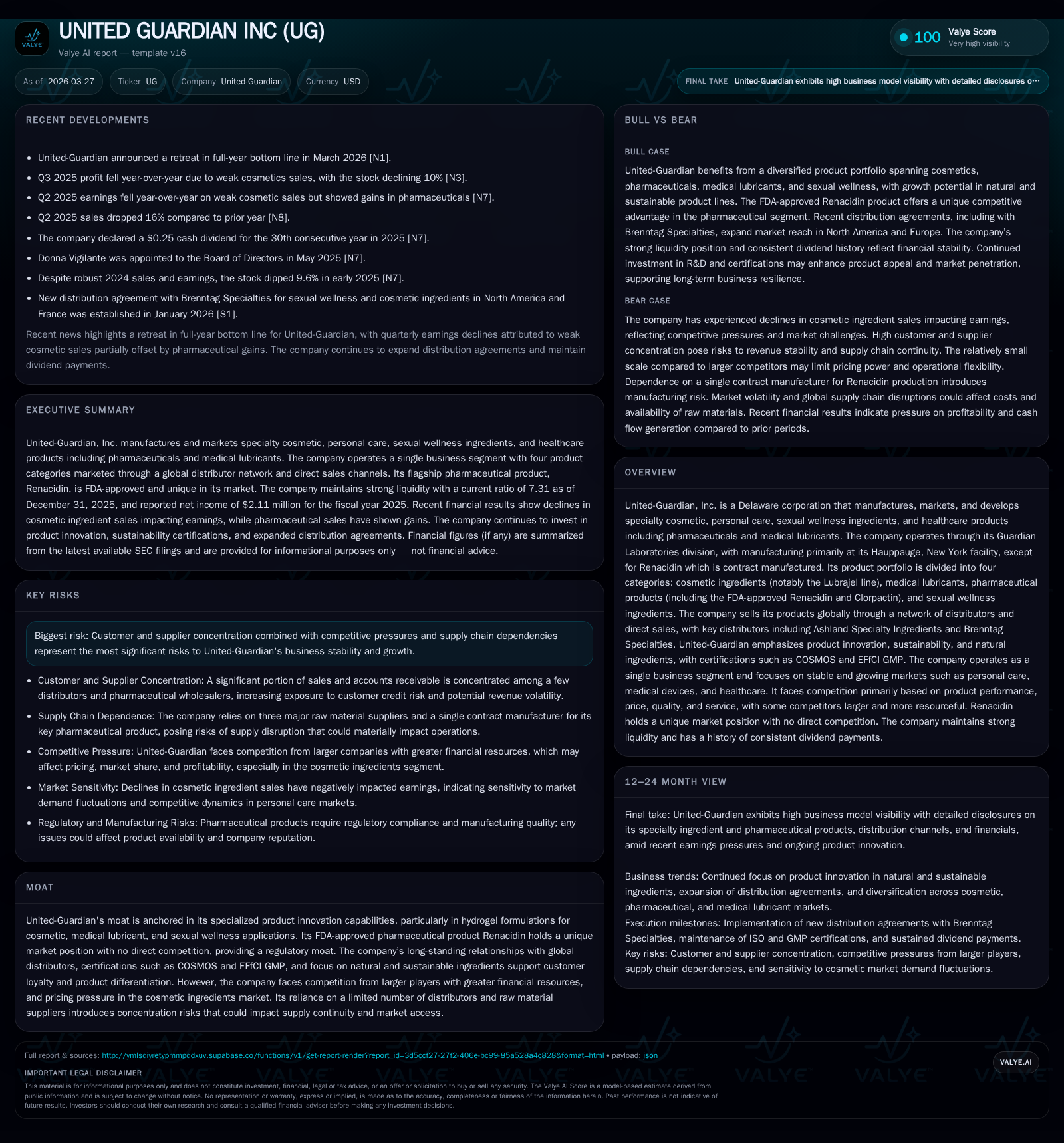

United-Guardian’s 2025 Earnings Decline Highlights Challenges in Cosmetic Ingredients Amid Growth in Pharmaceuticals

UNITED GUARDIAN INC reported a notable decrease in operating income and net income for 2025 despite revenue growth fueled by pharmaceutical sales.

In 2025, United-Guardian achieved revenue growth primarily from increased pharmaceutical product sales, notably Renacidin, and expansion of its distribution network. However, the company faced a significant retreat in profitability driven by lower-margin cosmetic ingredient sales, rising overhead costs, and ongoing tariff and supply chain headwinds. While new sexual wellness products are positioned for future uptake, risks remain centered on customer and supplier concentration and competitive pressures. Capital allocation continues to prioritize dividends, with steady R&D investment supporting innovation amid tightening market conditions.

Company Overview and Historical Performance

United-Guardian Inc operates through its Guardian Laboratories division, producing specialty cosmetic, personal care, sexual wellness ingredients, pharmaceuticals, and medical lubricants primarily out of Hauppauge, New York [S1][S15]. Its product portfolio uniquely blends hydrogel formulations such as the Lubrajel line for cosmetics and medical use alongside FDA-approved pharmaceutical products like Renacidin and Clorpactin [S15][S18].

Historically, the company’s revenue demonstrates cyclical dynamics influenced by product category demand and supply chain constraints. From 2017 to 2025, total revenues fluctuated notably:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 2 | 2 | 2 | 58995 | -35.2% |

| 2024 | 3 | 3 | 4 | 433077 | +25.9% |

| 2023 | 3 | 3 | 3 | 165716 | +0.5% |

| 2022 | 3 | 3 | 4 | 75179 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 3 | 2 | 18.7 |

| 2024 | 3 | 3 | 27.4 |

| 2023 | 0 | 3 | 22.7 |

| 2022 | 3 | 2 | 27.7 |

Source: SEC companyfacts cache [F1].

[Note: Revenue shows substantial variability partly due to product-specific cycles; operating income saw a steep decline in the latest year despite top-line growth -- data per [F1]]

Drivers of Past Growth

Key drivers include the pharmaceutical segment's rebound post-manufacturing disruptions in Renacidin supply during late-2023/early-2024 [S8]. Increased sales volumes to major wholesalers contributed to an approximate gross sales growth of pharmaceuticals by ~11% year-over-year in this period [S8]. The contract manufacturing model for Renacidin allows rapid scaling once resolved supply issues ease.

Contrasting this were declines in cosmetic ingredient volumes — particularly Lubrajel hydrogels — which typically command higher margins but faced pricing pressure from lower-cost competitors and reduced demand [S8][S19]. New trade tariffs imposed by the U.S., although partially mitigated by renegotiated trade agreements, introduced cost volatility impacting the company’s cost structure [S1].

Profitability Trends

Declining cosmetic ingredient contributions coupled with fixed production overheads raised unit costs in that segment, compressing overall gross margin from approximately 53% in FY24 to roughly 49% in FY25 [S12]. While operating expenses increased marginally (+3%), partly driven by consulting fees related to Renacidin studies and payroll costs aligned with innovation efforts, these could not offset margin erosion [S12].

Future Growth Prospects

United-Guardian has recently inked new distribution deals intended to expand sexual wellness ingredient sales across North America and France commencing early-2026 [S1][S15]. Though no revenues have been reported yet from this category, it represents a strategically targeted growth area leveraging the company's hydrogel formulation expertise.

The ongoing shift toward natural and environmentally friendly raw materials underpins product development efforts — certified under standards like COSMOS — which could enhance competitive positioning as sustainability becomes critical in personal care formulations [S15][S18].

Challenges remain around concentration risks: three distributors accounted for nearly three-quarters of sales in recent periods; similarly, three suppliers constituted about 97% of raw material purchases [S4][S16]. The company acknowledges these dependencies as potential disruptors if any partner curtails cooperation or faces supply issues.

Regulatory & Market Environment Impact

Pharmaceutical revenue is sensitive to government rebate programs like Medicare Part D reforms that affect pricing structures and rebate liabilities; however, United-Guardian benefits temporarily from "specified small manufacturer" status reducing immediate rebate impacts through at least the next couple years [S21][S14].

Trade policy uncertainties—such as retaliatory tariffs affecting imports/exports—continue presenting risks especially where raw materials are procured internationally or products are sold globally via distributors servicing diverse geographies including heavy exposure to China through ASI’s downstream channels [S1][S16][N1].

Forecasts & Monitoring Points (Analysis)

Explicit forward guidance is not provided; however, monitoring should focus on:

- Sales ramp-up of sexual wellness ingredients under newly signed Brenntag Specials distribution agreements,

- Margin recovery or further compression linked to cosmetic ingredient pricing dynamics,

- Progress on R&D initiatives – increased budget anticipated with project pipeline expansion,

- Potential impact of sustained or new tariffs altering cost basis or market access,

- Distributor agreement renewals especially with key customers like ASI given sizable share of sales.

Returns & Capital Allocation

United-Guardian reported an approximate Return on Equity around 18.7% for FY25 as net income totaled $2.11 million against equity near $11.23 million [F1]. Operating cash flow dropped sharply (-43%) relative to FY24 but remained positive at ~$1.97 million amidst sharply reduced capital expenditures ($59K vs prior $433K), reflecting conservative capex management possibly due to uncertain demand conditions or completed capacity investments [F1].

Free cash flow was approximately $1.9 million after accounting for capex outlay [F1]. Dividend payments stayed steady at about $2.77 million for the year representing a considerable distribution of available cash resources aligned with shareholder return priorities albeit constraining internal reinvestment potential somewhat [F1]. No share buybacks are noted.

Competitive Positioning & Moat Assessment

United-Guardian’s moat arises largely from its specialized hydrogel chemistry expertise enabling unique sensory-enhancing formulations across segments along with an FDA-approved pharma asset—Renacidin—that holds regulatory exclusivity lacking direct competition in urological treatment applications . Sustained relationships with global distributors also embed market access barriers for entrants though these same ties intensify concentration risks if partner alignments shift.

Focus on natural/sustainable ingredient lines certified by bodies like COSMOS adds differentiation but intensified competition from larger multinationals with deeper pockets limits pricing flexibility [S8]. Supply chain dependencies particularly concerning key raw material vendors accessed primarily domestically help reduce geopolitical risks but any disruptions would have outsized impact given supplier concentration levels.

Risks Summary

United-Guardian cites customer concentration risk—where three distributors drive roughly two-thirds+ of sales—and supplier concentration—with three main vendors fulfilling approximately all raw material purchase volume—as notable systemic vulnerabilities [S4][S16]. Increasing trade tensions exacerbate cost uncertainty especially given global supply chains linked significantly through China markets served indirectly via distributor ASI channels [N1][S1]. Competitiveness pressures particularly affect cosmetic ingredients with margin sensitivity heightened under pricing discounting strategies necessitated by market dynamics [S8].

Conclusion Summary

The juxtaposition between robust pharmaceutical volume growth against declining cosmetic ingredient profitability frames United-Guardian’s current earnings landscape following FY25 results: revenue expanded meaningfully but profits contracted substantially due to margin pressures and overhead cost absorption challenges within key segments.

Innovation investment continues alongside strategic distribution expansions into burgeoning sexual wellness categories offering longer-term growth avenues though initial commercialization hurdles remain evident.

Capital allocation favors dividend continuity supported by solid liquidity metrics despite lower operating cash flows.

Concentration risks along supplier/customer axes coupled with externalities tied to trade policies call for vigilance around operational resilience moving forward.

This analysis is based exclusively on publicly filed SEC reports ([S1]–[S29]), recent news ([N1]), and standardized financial data ([F1]). It does not embed speculative forecasts nor provide investment recommendations but contextualizes United-Guardian Inc.'s current business profile within its competitive and regulatory environment.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments