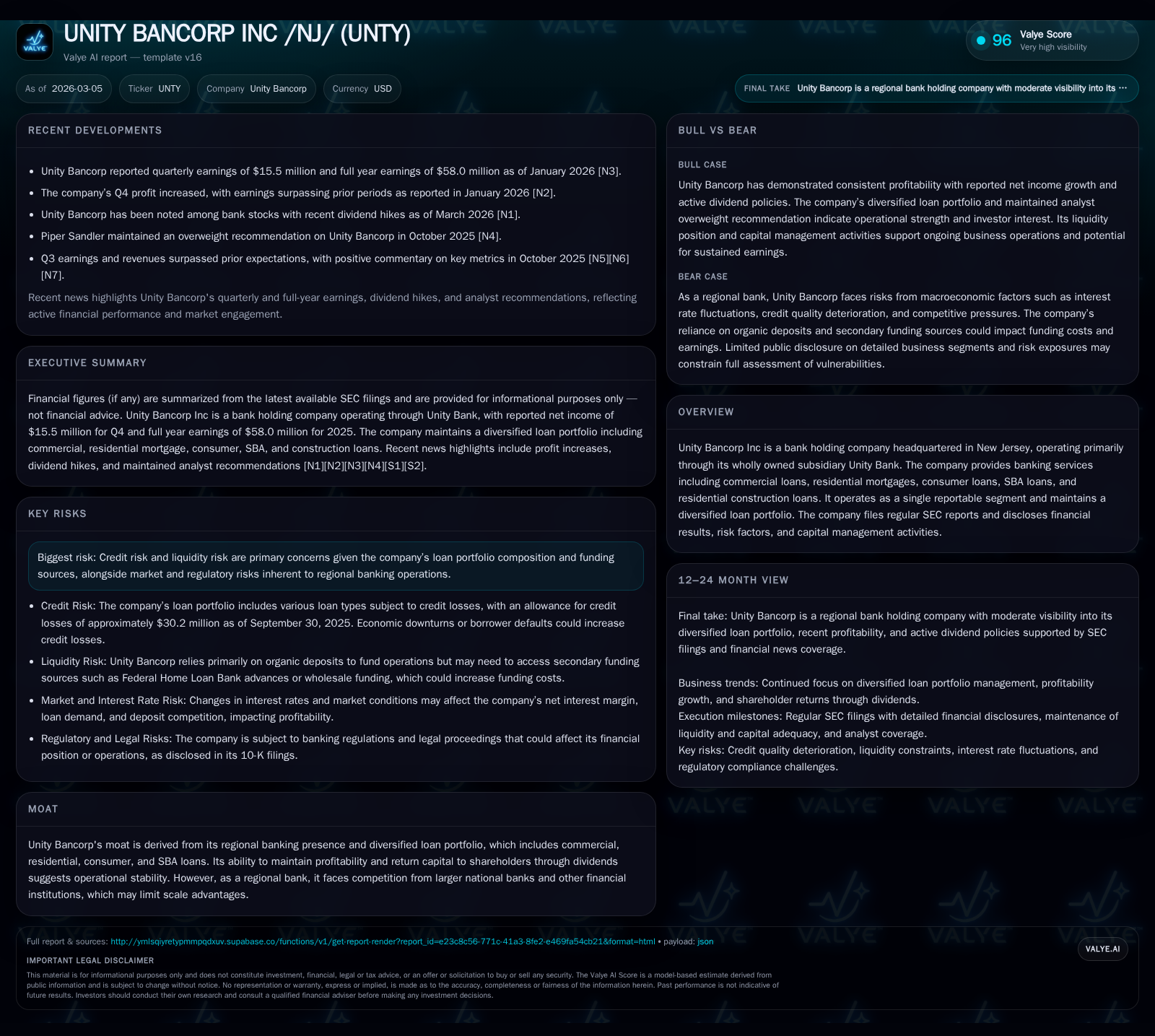

UNITY BANCORP’s Growth Fueled by Loan Expansion and Steady Capital Returns in a Competitive Regional Banking Sector

Unity Bancorp maintains growth through diversified lending and consistent shareholder returns despite regional banking challenges.

Unity Bancorp Inc, a New Jersey-based bank holding company operating through Unity Bank, has demonstrated robust net income growth driven by expanding commercial and residential loans. The company’s diversified loan portfolio balances credit risk, enhancing operational stability in a competitive market dominated by larger banks. Capital allocation priorities include regular dividends and share repurchases, supporting shareholder value amid modest return on equity. Key risks remain credit quality and external macroeconomic pressures, including liquidity demands and regulatory shifts.

Company Overview

Unity Bancorp Inc is a bank holding company based in New Jersey, operating primarily through Unity Bank as its wholly owned subsidiary. The company focuses on delivering a range of banking services encompassing commercial loans, residential mortgages, consumer lending, SBA loans, and residential construction financing. It reports as a single operating segment with a diversified loan portfolio designed to spread credit risk across various borrower profiles and industries [S1][S21].

Historical Performance and Growth Drivers

Unity has experienced consistent expansion over recent years, illustrated by net income rising from $9.96 million in FY2022 to $15.47 million in FY2025 — marking a compound trajectory punctuated by a 34.5% year-over-year increase between FY2024 and FY2025 [F1]. This uptrend correlates closely with significant growth in the loan book: total loans increased about $208 million from approximately $2.26 billion at the end of 2024 to about $2.47 billion at the end of Q3 2025 [S4], reflecting higher origination activity particularly within commercial and residential segments.

The loan portfolio composition highlights commercial loans as the dominant category ($1.58 billion as of September 30, 2025), followed by residential mortgages ($677 million) and smaller allocations to consumer loans ($83 million) plus SBA and construction loans [S4]. This diversified exposure establishes resilience against sector-specific downturns while capitalizing on regional economic growth.

Operating cash flow showed slight contraction by -6.4% YoY to approximately $44.9 million for FY2025 after peaking in prior years, largely due to fluctuations in working capital related to loan originations [F1]. Despite this, free cash flow remains healthy around $44.3 million after accounting for modest capital expenditures (down 18.6% YoY), indicating efficient operational management [F1].

Equity grew materially from $239 million at the end of FY2022 to roughly $346 million at end-FY2025 supported by retained earnings accumulation and equity issuance, bolstering capital adequacy for future growth opportunities [F1][S23].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|

| 2025 | 15 | 45 | 564000 | +34.5% |

| 2024 | 12 | 48 | 693000 | +17.8% |

| 2023 | 10 | 47 | 955000 | -1.9% |

| 2022 | 10 | 43 | 1482000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 6 | 5 | 44 |

| 2024 | 5 | 6 | 47 |

| 2023 | 5 | 16 | 46 |

| 2022 | 4 | 0 | 41 |

Source: SEC companyfacts cache [F1].

Note: Operating Cash Flow (OpInc), Capex, Dividends and Buybacks are approximate annual totals.

Capital Allocation and Returns

Unity Bancorp allocates capital toward steady dividend payouts alongside share repurchases illustrating commitment to returning value amid moderate profitability metrics. Dividends paid increased annually reaching over $5.6 million in FY2025 with payouts remaining consistent per share at approximately $0.14 quarterly as noted in recent filings [S3][S24]. Concurrently, share repurchases totaled about $5 million last year after larger buyback activity during FY2023; reflecting both opportunistic capital deployment during valuation windows and management's intent to support earnings per share [F1].

The approximate Return on Equity stands near 4.5% based on FY2025 net income relative to average shareholders' equity — below typical peer regional banks thus indicating potential room for margin expansion or cost efficiency gains over time [F1]. Low interest rate environments combined with competitive pressure may cap ROE improvement absent strategic portfolio rebalancing or revenue diversification.

Balance Sheet Quality & Funding

On the asset side, liquidity is sound with cash equivalents around $203 million as of late Q3 2025 holding steady versus prior periods [S4]. Investment securities aggregate about $131 million comprising debt securities available for sale and held-to-maturity categories alongside equity securities totaling nearly $13 million [S4].

The deposit base totaled approximately $2.27 billion as of September 30, increasing year-over-year across demand deposit types and time deposits — with brokered deposits rising modestly providing additional funding diversification [S23]. Borrowed funds including Federal Home Loan Bank advances stand near $232 million complementing deposits though exposing the bank to wholesale funding risk if primary deposits decline under stress scenarios [S23][S22].

The allowance for credit losses increased from roughly $26.8 million at end-2024 to about $30.2 million by Q3-2025 tracking loan book expansion while managing emerging credit risks amidst economic uncertainty [S4][S18]. Nonperforming assets remain contained but require ongoing vigilance given exposure to commercial construction loans especially where delinquencies have historically been cyclical.

Industry Context (Analysis)

Unity Bancorp functions within a highly fragmented U.S regional banking sector where scale advantages often accrue to larger institutions imposing pricing pressures on deposit gathering and loan spreads for mid-sized peers like Unity Bank . Rising regulatory scrutiny post-pandemic era adds compliance costs impacting smaller banks disproportionally relative to their resources.

Competition from fintech lenders and larger money-center banks offering bundled digital services further constrains growth channels for traditional lenders reliant on branch networks within regional markets such as New Jersey . However, Unity's relationship-driven SBA portfolio niche offers some differentiation leveraging federal guaranteed programs crucial for small business lending.

Future Growth Prospects & Risks

Growth moving forward likely hinges on sustaining momentum in core commercial lending coupled with selective expansion into consumer or residential construction where yields may command premium pricing given builders' demand cycles [N1][S1]. Management must balance aggressive volume growth against evolving credit monitoring frameworks especially if macroeconomic headwinds intensify.

Liquidity management will remain critical should deposit volatility increase amidst shifting interest rates or broader financial system uncertainties compelling stepped-up reliance on wholesale funding sources that could elevate funding costs [S22][S26]. Regulatory changes affecting capital buffers or lending restrictions represent persistent risks given Unity’s intermediate bank size.

Though explicit guidance was not disclosed in recent filings or press releases beyond dividend declarations [N1][S3], investors should monitor quarterly updates tracking asset quality trends (e.g., nonperforming loans ratios), margin compression indicators tied to interest rate movements, as well as capital adequacy ratios ensuring resilience under stress tests.

Conclusion

Unity Bancorp has demonstrated commendable top-line earnings growth powered principally by sustained loan book enlargement alongside disciplined capital returns via dividends and buybacks over the past several fiscal years [F1][S24]. Its diversified loan portfolio supports risk mitigation yet exposes the company to credit cycle fluctuations particularly within construction financing segments.

Operating cash flows remain healthy albeit somewhat constrained recently while ROE levels suggest moderate profitability characteristic of regional banking franchises without scale dominance [F1]. Liquidity remains adequate but warrants close monitoring due to increasing competition for deposits against national peers compounded by potential macroeconomic shocks.

Maintaining a proactive risk management stance alongside focusing on efficiency improvements could enhance shareholder returns going forward while preserving the franchise positioning within its New Jersey banking market niche.

Disclaimer: This analysis is intended solely for informational purposes derived from publicly filed documents and news sources; it is not investment advice nor an endorsement or critique of any security.

Comments