Donegal Group Navigates Regional Constraints and Volatile Loss Trends While Sustaining Profitability

Donegal Group leverages its regional focus and underwriting discipline to manage growth and underwriting volatility amid increasing loss severity in property-casualty insurance.

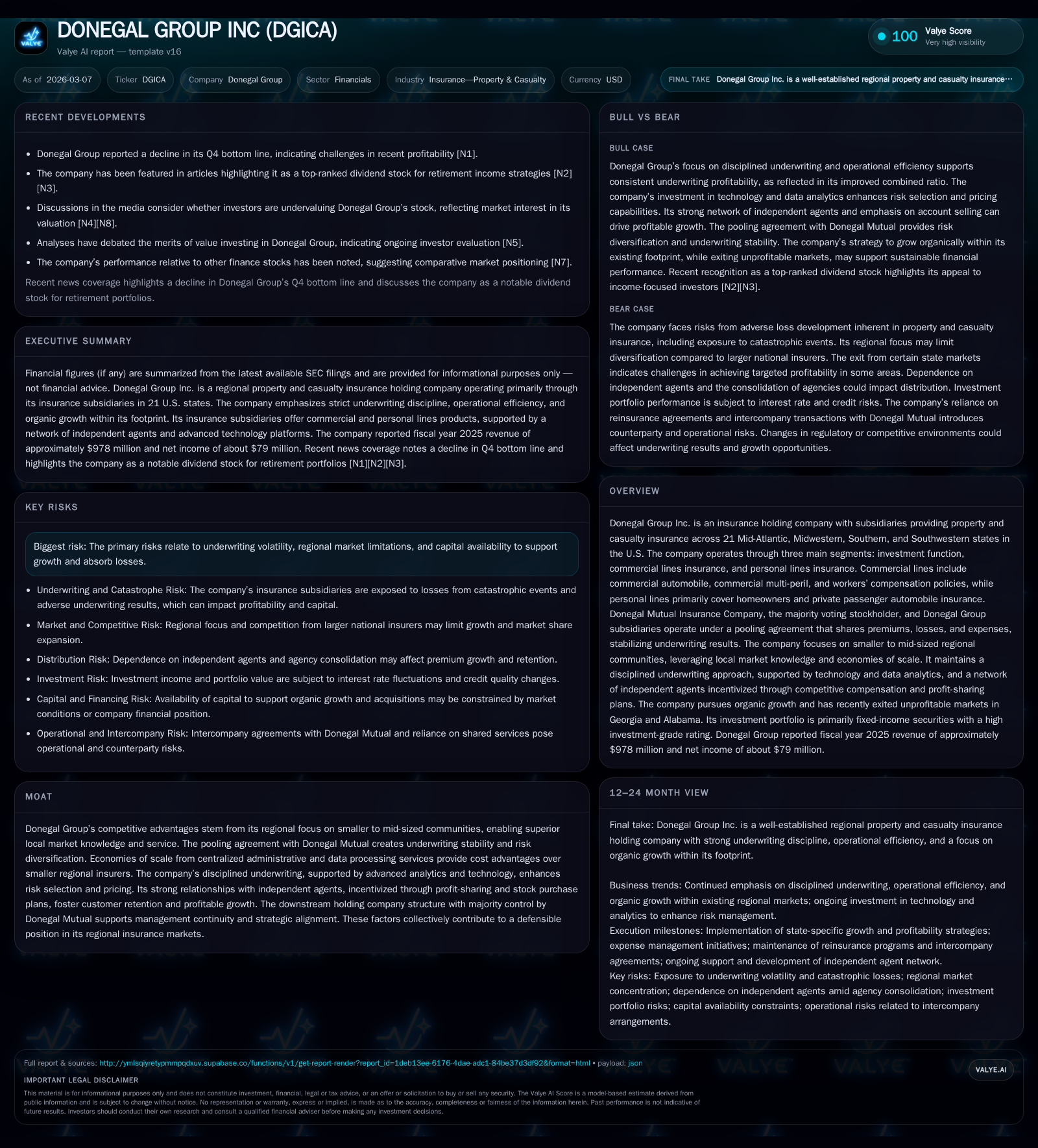

Donegal Group Inc., a mid-sized regional property and casualty insurer operating primarily in 21 U.S. states, reported modest top-line contraction but significant net income improvement in 2025. The company benefits from a pooling agreement with its majority stockholder Donegal Mutual and leverages local market knowledge to maintain underwriting discipline and stable agent relationships. Key risks include heightened loss severity driven by social inflation, weather catastrophes, and regulatory pressures, alongside capital constraints limiting expansion. Donegal is focused on profitable organic growth rather than acquisitions, investing in technology modernization and analytics to enhance underwriting precision and operational efficiency.

Company Overview

Donegal Group Inc. is a classic example of a well-capitalized regional property and casualty insurance holding company that operates primarily in smaller to mid-sized communities across 21 U.S. states spanning the Mid-Atlantic, Midwest, South, and Southwest regions [S1][S5][S7]. The company’s insurance subsidiaries write commercial lines such as commercial automobile, multi-peril policies including workers’ compensation, alongside personal lines like homeowners and private passenger automobile insurance.

Central to Donegal’s business model is its downstream holding company structure dominated by Donegal Mutual Insurance Company—which holds approximately 70% of combined voting power via Class A and B shares as of end-2025—anchoring strategy alignment and ensuring continuity in management [S1][S7]. Further reinforcing the group's stability is the intercompany pooling agreement that consolidates premiums, losses, and expenses among Donegal Mutual and other subsidiaries. This mechanism confers diversification benefits usually associated with larger insurers while preserving Donegal’s regional agility.

Historical Performance and Growth Drivers

From FY2022 through FY2025, Donegal exhibited steady revenue growth punctuated by an inflection point in FY2024-25:

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|

| 2025 | 978 | 79 | 70 | -1.2% | +56.0% |

| 2024 | 990 | 51 | 67 | +6.7% | +1049.3% |

| 2023 | 927 | 4 | 29 | +9.3% | +325.9% |

| 2022 | 848 | -2 | 67 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | ROE% |

|---|---|---|

| 2025 | 26 | 12.4 |

| 2024 | 23 | 9.3 |

| 2023 | 0.9 | |

| 2022 | -0.4 |

Source: SEC companyfacts cache [F1].

Revenue expansion from FY2022 to FY2024 was driven by organic growth within targeted state markets alongside underwriting rate increases aimed at offsetting inflationary claims costs [F1][S8]. The slight revenue dip in FY2025 coincided with tactical tightening of personal lines new business volumes amid cost pressures but net income surged materially due to improved pricing adequacy coupled with disciplined expense management leveraging operating leverage benefits [F1][S11].

Operating cash flow remained robust throughout this period with positive inflections paralleling earnings strength, contributing to free cash flow availability after minimal capex expenditures historically below $2 million annually prior to FY2016 [F1][S28]. Equity increased steadily reflecting retained earnings accumulation supporting solvency requirements.

Competitive Positioning and Moat

Donegal's distinct competitive advantage arises from its strategic focus on smaller to medium-sized regional markets where deep local market knowledge creates a durable moat [valye_report_excerpt.moat]. Unlike more geographically sprawling insurers burdened by higher fixed costs or dilutive acquisitions, Donegal leverages centralized back-office functions such as accounting, data processing, investment management, and claims administration — realizing economies of scale without losing touch with regional nuances crucial for profitable underwriting.

The pooling arrangement with Donegal Mutual not only stabilizes underwriting results by sharing risk but also promotes disciplined profitability-focused culture throughout the group — an uncommon feature for insurers of comparable scale relying instead on riskier diversification strategies or rapid expansion through acquisitions [S1][S19].

Another pillar is Donegal's tightly knit network of roughly two thousand independent insurance agencies incentivized through profit-sharing arrangements and stock purchase plans that foster agent loyalty while aligning interests toward growing quality book of business rather than plain volume chasing [valye_report_excerpt.moat][S10]. Their fully automated portals simplify policy issuance workflows enhancing the agents' ease-of-doing-business -- a key retention factor given rising competition for agency shelf space from national carriers or technology-enabled entrants [S10].

Underwriting Discipline Amid Industry Challenges

The property-casualty insurance industry has faced rising loss severity over recent years propelled by social inflation effects — courts awarding larger judgments with expanded coverage interpretations — alongside macroeconomic pressures including inflation driving higher medical treatment costs, automobile repair parts shortages exacerbated by supply chain disruptions, plus labor cost escalations impacting property claims repair timelines [S1][S12][S14]. These factors impose significant reserve uncertainty risks.

Donegal addresses these challenges through robust underwriting discipline characterized by:

- Selecting mostly standard or preferred risks avoiding problem accounts;

- Applying tiered predictive modeling based on enterprise-wide data analytics including AI-enriched catastrophe models assessing probable maximum fire losses at granular county levels across states [S13][S23];

- Maintaining agile rate management programs regularly adjusting pricing reflective of emerging claims trends without unduly sacrificing customer retention;

- Employing payroll audits for workers' compensation exposure validation enhancing pricing accuracy;

- Exercising portfolio optimization including exiting unprofitable markets such as commercial insurance lines in Georgia and Alabama where profitability targets proved elusive despite prior penetration efforts [S11];

- Utilizing layered reinsurance programs designed to contain net risk retentions despite recent market capacity contraction leading to elevated retention levels particularly after hurricane seasons [S12][S24].

While reinsurance mitigates catastrophe exposures deriving from hurricanes impacting Mid-Atlantic/Southern states or hail/tornado events predominantly affecting Midwest operations; all these are subject to natural variability intensified possibly due to evolving climate patterns introducing unpredictability not entirely capturable by historical loss signals [S1][S12].

Growth Prospects

Donegal views its most promising avenues as profit-driven organic expansions rather than acquisition-fueled size increments given the current footprint has untapped opportunities especially within underpenetrated states or specific classes like commercial auto or multi-peril segments where risk selection capabilities provide competitive advantage [valye_report_excerpt.overview][S8][S19]. New product offerings benefit from upgraded rating methodologies incorporating third-party data sources augmenting segmentation precision enabling differentiated pricing tailored per local loss experience profiles.

The company continues developing technology infrastructure including cloud migration for Guidewire systems along with gradual deployment of GenAI-enhanced tools boosting underwriting automation, predictive analytics depth, fraud detection sophistication while simultaneously reducing vendor costs arising from legacy platform maintenance burdens [S21][S23]. This ongoing digital evolution should enhance agility permitting faster responses to emerging market dynamics or regulatory shifts which may otherwise constrain portfolio composition flexibility.

Regulatory scrutiny remains a backdrop concern especially regarding permissible rating criteria use; political/consumer pressure against credit scoring or AI-driven decision models could compel adjustments limiting actuarial sophistication thus potentially compressing margins over time if alternative methods prove less predictive of loss outcomes [S9][S16].

Forecasts & Milestones / What To Watch

Explicit forward-looking guidance or milestones were not disclosed recently; however investors should monitor:

- Progress on Guidewire cloud migration scheduled through calendar year increments;

- Deployment scale-up of GenAI-based risk modeling tools balanced against observed operational disruptions or cost overruns;

- Underwriting margin trends through quarterly results signaling effectiveness of price adequacy initiatives amidst evolving loss cost inflation;

- Reinsurance renewals indicating whether cost/capacity conditions remain favorable relative to prior years impacting retentions borne;

- Regulatory developments impacting pricing models notably around use of automated decision-making algorithms;

- Market responses to continued agency consolidation trends emphasizing relationship strength with regional/national agency clusters overseen via dedicated national accounts teams enhancing distribution expandability potential [N1][N3][N2].

Capital Allocation & Financial Returns

Donegal maintains disciplined capital stewardship prioritizing dividend payouts consistent with underwriting profitability while preserving balance sheet strength evidenced by equity rising steadily from $483 million in FY22 to $640 million by FY25 accompanying net income rebound substantiates sensible retention strategies fostering growth without excessive leverage exposure [F1][S25].

Dividend distributions increased modestly aligned with earnings improvements totaling approximately $25.7 million paid during FY2025 compared with $22.7 million in prior year Correspondingly free cash flow generation approximated $70 million balancing steady-state capital needs against shareholder returns effectively.

Stock repurchase activity has largely been absent recently suggesting preference for deploying cash towards organic growth investments rather than financial engineering; this approach reduces execution risk inherent in acquisitions though might modestly constrain rapid scalability prospects typical for mid-tier insurers operating regionally.

Return on equity measured approximately at about 12.4% in the latest fiscal year reflects a healthy return profile balancing underwriting profits complemented by conservative investment income strategies focusing mostly on high-grade fixed maturity instruments minimizing volatility exposure common to equity-heavy portfolios seen at peers [F1].

Risks Summary

Key risks faced persistently include:

- Heightened severity trends worsened by costly litigations fueled further through third-party litigation financing which can inflate claim settlements beyond reserves causing adverse reserve development impacting earnings unpredictably;

- Exposure concentration within limited geographic footprint particularly Pennsylvania through Michigan states making financial outcomes sensitive to localized catastrophic events or regulatory shifts impacting rate approvals/refund obligations;

- Inflationary pressures impacting replacement costs for auto parts/building materials labor prolonging claim settlement cycles inflating claim reserves unexpectedly;

- Potential inadequacies or cost increases in reinsurance purchasing influenced by external market factors reducing coverage breadth raising downside risk;

- Sudden regulatory actions limiting use of rating characteristics integral for differentiation representing material headwinds for future profitability if alternatives fall short;

- Technology project execution risks associated with major cloud/GenAI system rollouts impacting operational efficiency or customer experience temporarily if disruptions arise unexpectedly,

- Increasing competitive dynamics intensified by larger insurers possessing greater technological resources deploying advanced AI/automation potentially eroding agent loyalty compelled accelerated innovation investments urgently needed.

Management appears cognizant addressing these factors proactively through analytics enhancements enterprise-wide strict expense controls agency engagement programs along with focused portfolio pruning actions demonstrating commitment toward sustainability rather than aggressive top-line chase prone to volatility spikes common elsewhere in P&C sector.[valye_report_excerpt.risks]

Conclusion

Donegal Group exemplifies a regional insurer balancing longstanding industry challenges—social inflation pressures along evolving climatic catastrophe exposure—with strategic focus on underwriting discipline augmented by technological advances enabling data-driven risk selection/premium adequacy enhancements critical amid competition intensified by large-cap carriers’ resource advantages.

While recent revenue softness cautions vigilance around personal lines exposure management during inflationary conditions,the robust improvement in profitability underscores successful navigation within complex environment maintaining agent partnerships leveraging unique pooling arrangements support diversified yet focused book construction underpinning attractive operating returns balanced against prudent capital deployment signaling thoughtful long-term value preservation priorities.

Stakeholders monitoring execution progress regarding technology modernization completion milestones alongside emerging regulatory actions surrounding rating methodologies will gain deeper insight into sustainable competitive positioning trajectory as donegal proceeds cautiously governing capital allocation cautiously favoring organic growth pathways over acquisitive expansion uncommon for insurers this size yet reflective of management’s strategic prudence.

This document is intended solely for informational purposes reflecting publicly available data as of early March 2026; it does not constitute investment advice nor recommendations regarding any securities issued by Donegal Group Inc.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments