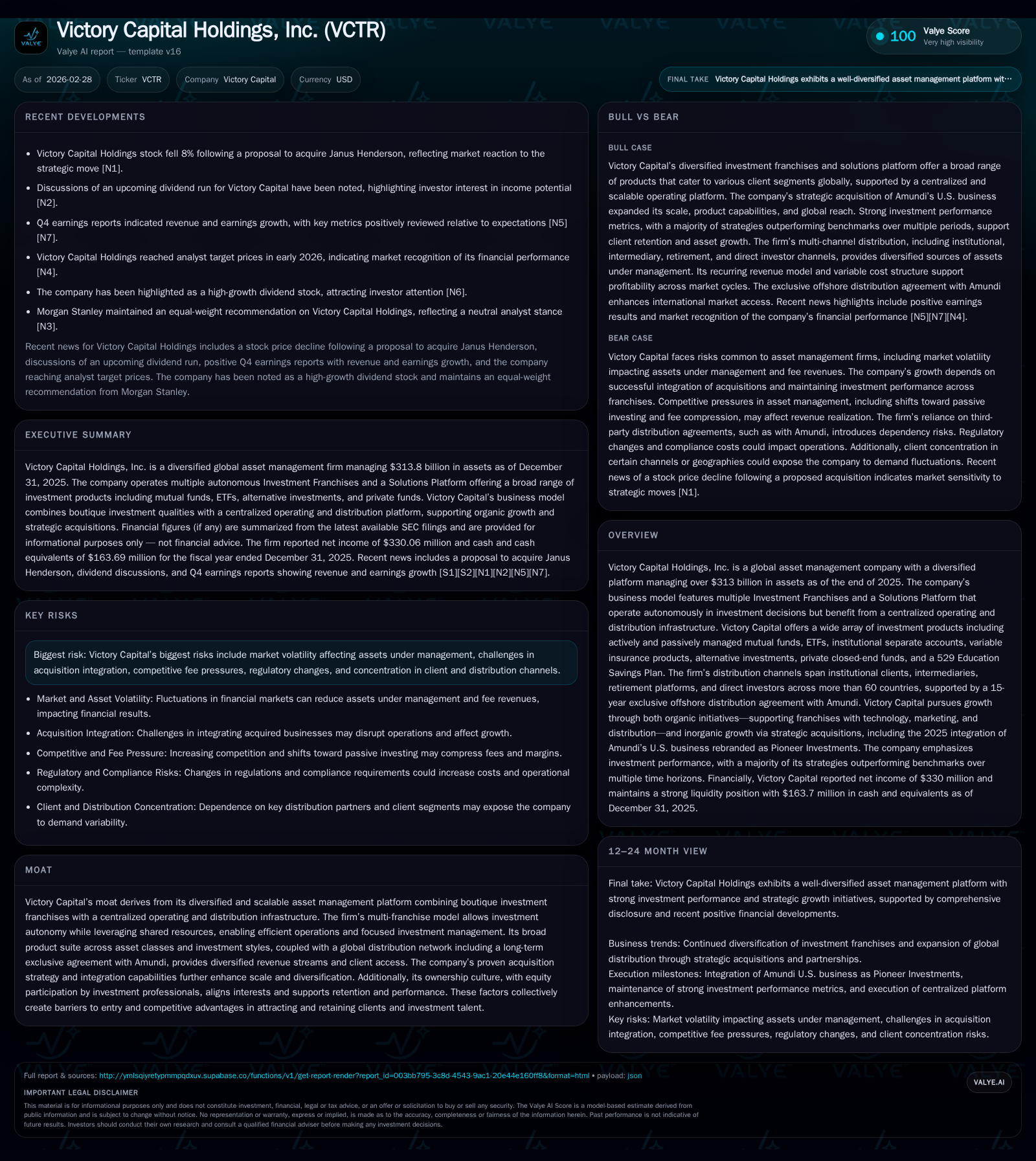

Victory Capital’s Scale and Acquisition Strategy Propel Asset Growth With Integrated Boutique Platform

Victory Capital leverages a multi-franchise, centralized platform to expand assets under management through acquisitions and organic growth, balancing investment autonomy with operational efficiency.

Victory Capital Holdings, Inc. has demonstrated significant growth in assets under management (AUM), reaching $313.8 billion by the end of 2025, driven largely by its acquisition of Pioneer Investments and strong organic flows. The firm operates a diversified model blending autonomous boutique franchises with a centralized distribution and operations platform, supporting 187 investment strategies across multiple asset classes and geographies. Financially, Victory improved operating income and net income year over year through 2025 while maintaining disciplined capital allocation with dividends and share repurchases. Debt refinancing extended maturities and improved interest margins, supporting financial flexibility for ongoing operations and acquisitions.

Historical Growth and Performance

Victory Capital Holdings has exhibited notable expansion since its formation following the management-led buyout in August 2013 when it managed $17.9 billion in assets. By December 31, 2025, total client assets reached $316.6 billion with assets under management (AUM) at $313.8 billion, reflecting substantial scale achieved partly through the April 1, 2025 acquisition of Amundi’s U.S. asset management business rebranded as Pioneer Investments [S1].

Financial results for FY 2025 include operating income of $478 million supported by expanded revenues aligned with AUM growth; net income increased to $330 million from $289 million in FY 2024 representing a roughly 14% year-over-year rise; operating cash flow stood at $385 million; capital expenditures remained modest at approximately $4.2 million; shareholder equity totaled about $2.42 billion yielding an approximate return on equity of 13.6% based on net income relative to equity [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 330 | 385 | 478 | 4 | +14.3% |

| 2024 | 289 | 340 | 428 | 1 | +35.5% |

| 2023 | 213 | 330 | 328 | 5 | -22.6% |

| 2022 | 276 | 335 | 399 | 5 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 157 | 196 | 381 |

| 2024 | 101 | 104 | 339 |

| 2023 | 85 | 139 | 325 |

| 2022 | 69 | 101 | 330 |

Source: SEC companyfacts cache [F1].

Business Model

Victory Capital operates a multi-franchise asset management platform comprising autonomous Investment Franchises alongside a Solutions Platform delivering specialized strategies such as multi-asset portfolios, quantitative models, thematic outcomes, and factor-based approaches [S12]. Each franchise maintains independent investment decision-making within established mandates while leveraging centralized functions including sales distribution, marketing support, compliance oversight, technology infrastructure, and operational efficiencies [S1], [S19].

The product suite includes actively managed mutual funds, passive ETFs under the VictoryShares brand, institutional separate accounts, variable insurance products (VIPs), alternative investments like private closed-end funds, Collective Investment Trusts (CITs), UCITS funds targeting international clients, separately managed accounts (SMAs), unified managed accounts (UMAs), proprietary ETF model strategies, and a Section 529 Education Savings Plan [S1], [S12].

Distribution channels cover U.S. institutional investors primarily through consultants and asset owners; intermediaries including broker-dealers, retirement platforms and Registered Investment Advisors (RIAs); direct retail investors via digital platforms; plus international clients served through an exclusive offshore distribution agreement with Amundi that provides access across over thirty-five countries globally [S12], [S17], [S20].

Past Drivers of Growth

Growth drivers include strategic acquisitions integrated onto the platform that evolve into organic growth engines; strong investment performance resulting in inflows; expanded penetration across institutional and retail channels domestically; and broadening global client base leveraging proprietary multi-asset solutions [S1], [S12], [S21].

Significant milestones:

- The Pioneer Investments acquisition in early Q2-2025 nearly doubled AUM.

- Gross client flows totaled approximately $60 billion in FY2025 with net outflows limited to about $4.5 billion despite market volatility.

- Approximately two-thirds of funds carry four- or five-star Morningstar ratings indicative of competitive performance supporting investor retention [S1], [S22].

Future Growth Prospects

Victory’s future expansion depends on:

- Continuing strategic bolt-on acquisitions that enhance product breadth or geographic reach while preserving franchise autonomy.

- Leveraging the exclusive global offshore distribution partnership with Amundi to deepen international client engagement.

- Driving organic inflows via innovation within thematic outcomes and quantitative strategies alongside traditional active mandates within the Solutions platform.

- Investing in data analytics and AI tools aimed at improving sales effectiveness across diverse distribution channels [S17].

Challenges include integration complexities arising from recent elevated acquisition-related expenses ($104 million recorded in FY2025), evolving regulatory environments globally affecting cross-border marketing compliance, competitive fee pressures especially for passive ETFs, and concentration risks stemming from reliance on large intermediary platforms subject to changing mandates or preferences [S11], [S14], [S23].

Key Milestones & Expectations

While explicit forward guidance remains limited beyond recent earnings disclosures indicating FY2025 results exceeded estimates with positive momentum entering early FY2026 [[N1],[N2],[N5]], key areas to monitor include:

- Progress on integrating any announced acquisition proposals such as Janus Henderson.

- Organic net flow trends post-Pioneer acquisition impact.

- Operating margin improvements driven by scale efficiencies.

- Fee rate evolution balancing shifts toward lower-cost ETFs.

- Regulatory developments impacting fund governance or disclosure requirements.

Financial Returns & Capital Allocation

Revenue streams are predominantly recurring fees linked directly to AUM levels across specialized asset classes commanding premium fees relative to commoditized index products [S13]. Operating expenses are largely variable—principally incentive compensation tied to revenues—enabling automatic scaling aligned with market conditions.

Free cash flow approximated $381 million in FY2025 after capital expenditures focused primarily on technology upgrades rather than extensive infrastructure investments [F1]. This strong cash generation supports consistent shareholder returns:

- Dividends paid increased significantly from $101 million in FY24 to $157 million in FY25.

- Share repurchases accelerated markedly reaching nearly $196 million in FY25 reflecting confidence despite integration spending.

Debt refinancings extended revolving credit facility maturity through September 2030 and term loan maturity through September 2032 while reducing interest rate margins—actions that preserve liquidity buffers critical for ongoing operations and acquisition financing needs [S6], [S7], [S8].

Strategic Differentiators & Competitive Positioning

Victory Capital’s hybrid model combining boutique franchise autonomy with centralized operational scale provides nimbleness coupled with efficiency advantages uncommon among large monolithic firms or stand-alone boutiques alike. High employee ownership aligns incentives fostering talent retention—a key advantage amid intense competition for investment professionals across financial hubs [S10], [S21], [S22].

The exclusive global offshore reseller arrangement with Amundi offers privileged placement opportunities internationally that smaller peers may find difficult to replicate.

High concentrations of Morningstar four- or five-star ratings confirm solid benchmark-relative outperformance maintained across multiple timeframes reinforcing credibility with institutional consultants who serve as gatekeepers for inflows [S22], [S25].

Remaining challenges include fee compression catalyzed by passive investing trends; geopolitical uncertainties influencing cross-border sales; potential integration distractions impacting franchise focus; plus increasing regulatory complexities affecting product design or marketing disclosures potentially slowing speed-to-market advantages.

Risks Summary

Primary risks encompass:

- Market volatility affecting AUM-dependent revenues altering near-term profitability outlooks.

- Execution risk related to acquisition integration given recent restructuring costs alongside personnel retention considerations.

- Heightened fee competition necessitating continuous operational discipline paired with product innovation adapting offerings without sacrificing margins.

- Client concentration risk notably reliance on large intermediary platforms whose shifting mandates could trigger material redemptions.

- Expanding regulatory requirements spanning multiple jurisdictions increasing compliance overhead possibly diluting returns.

These underscore the importance of ongoing prudent capital deployment alongside maintaining rigorous governance practices [S15], [S23], [S24].

Conclusion & What to Monitor Next

Victory Capital exemplifies building scale through transformative acquisitions integrated into a flexible multi-brand architecture combined with centralized operational leverage—a hybrid model premised on delivering investment autonomy supported by efficiency synergies rare among peers.

Investors should track integration progress without dilution of performance cultures; organic net flow patterns amid macroeconomic shifts; margin sustainability amid evolving product mix favoring ETFs; international market penetration leveraging Amundi’s network; plus disciplined capital allocation balancing growth investments versus shareholder returns.

No explicit guidance beyond reported results currently exists but subsequent quarterly disclosures around pipeline acquisitions or margin trends will offer valuable insights into future trajectory.

This analysis is based solely on factual financial information extracted directly from Victory Capital Holdings’ SEC filings ([F1],[S1]-[S29]) and substantiated news reports ([N1]-[N11]) up to early 2026 without speculation or recommendations. It adheres to buy-side research standards emphasizing objectivity.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments