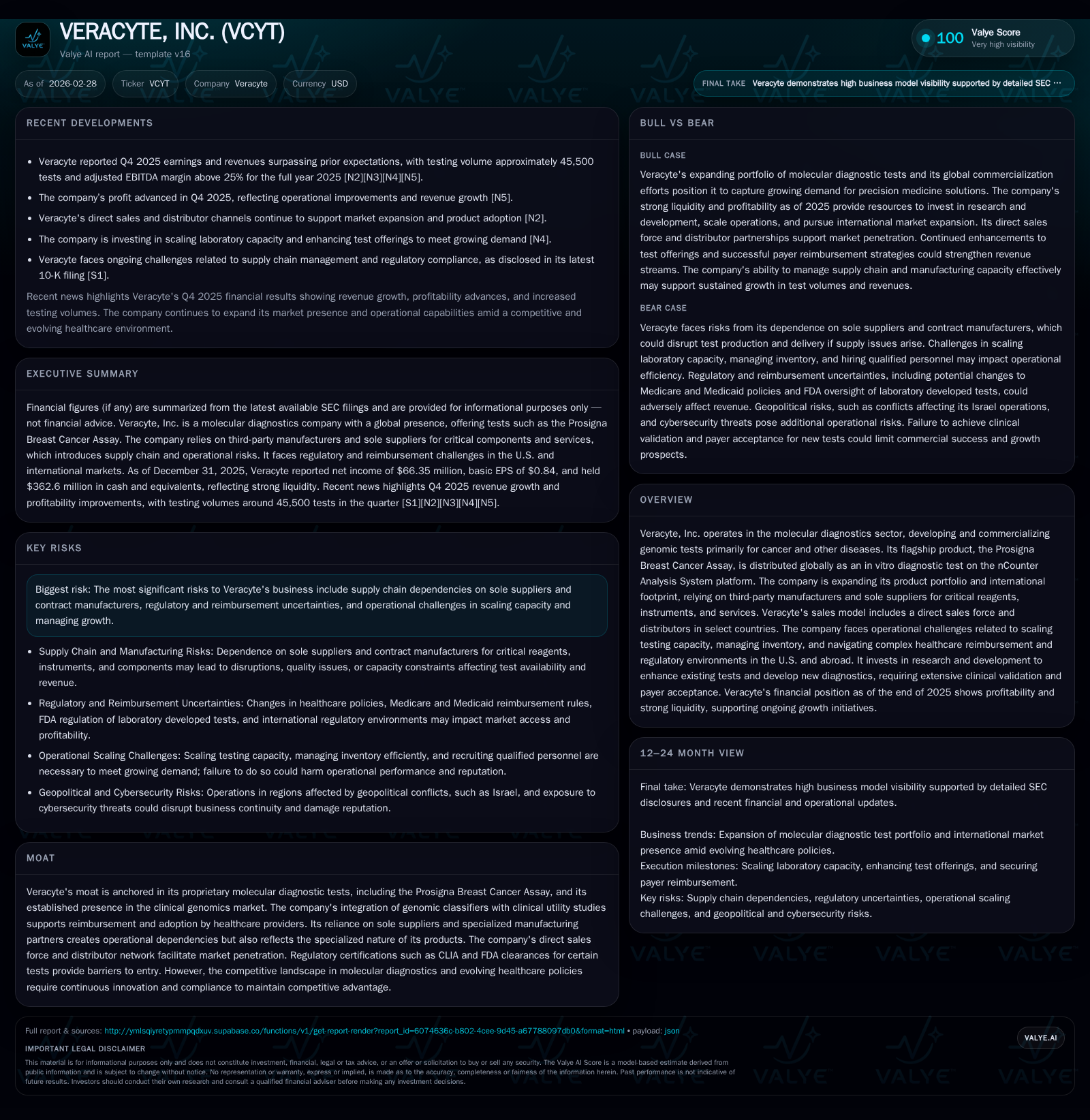

Capital Efficiency and Growth Challenges at Veracyte in 2025

Veracyte showcases marked profitability and cash flow improvements in 2025 while contending with operational scaling and global expansion hurdles.

In fiscal year 2025, Veracyte, Inc. pivoted from a period of steep operating losses to substantial profitability and strong cash flow generation, underscoring a significant business turnaround. This financial upswing was propelled by increased test volumes, cost controls, and enhanced liquidity management, reflected in an impressive operating income growth of nearly 258% year-over-year. Nonetheless, the firm continues to face inherent industry challenges including sole-supplier dependencies, supply chain complexities, evolving reimbursement frameworks, and the intricacies of international market entry. Strategic capital allocation remains focused on sustaining operational capacity and product innovation amid these constraints.

From Losses to Profit: Veracyte’s Financial Journey Through 2025

Veracyte executed a remarkable financial turnaround in FY2025 after several challenging years characterized by substantial operating deficits. The company reported operating income of $57.8 million for the year ending December 31, 2025—a striking 257.9% increase over the prior year’s $16.1 million [F1]. This trajectory reversed prior losses of $85.8 million in FY2023 and $41.1 million in FY2022, indicating improved operational leverage.

Net income aligned with this positive momentum, rising 174.9% year-over-year to $66.4 million in FY2025 from $24.1 million in FY2024 [F1]. Such profitability expansion evidences tighter cost controls alongside growing revenue streams primarily derived from increased test volume demand and improved reimbursement scenarios.

Operating cash flow presents a similarly encouraging trend—soaring by 81.5% year-over-year to $136.3 million—and reflects enhanced working capital management underpinning liquidity strength (current ratio of 8.15) [F1]. Capital expenditures were moderated down by 14.3%, settling at $9.7 million for FY2025 despite the larger operational scale [F1]. This combination suggests efficiency gains in fixed asset deployment amid scaling pressures.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 66 | 136 | 58 | 10 | +174.9% |

| 2024 | 24 | 75 | 16 | 11 | +132.4% |

| 2023 | -74 | 44 | -86 | 10 | -103.5% |

| 2022 | -37 | 8 | -41 | 9 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 127 | 5.1 |

| 2024 | 64 | 2.1 |

| 2023 | 34 | -7.1 |

| 2022 | -1 | -3.4 |

Source: SEC companyfacts cache [F1].

Note: Latest available revenue figure dates back to Q3-2018; analysis focuses on profit and cash metrics as per latest filings [F1].

Supply Chain Dependencies and Operational Scaling Challenges

Veracyte’s molecular diagnostic testing relies heavily on critical raw materials such as reagent kits and diagnostic instruments sourced predominantly from sole suppliers [S1]. This exclusivity creates pronounced operational risk—any disruption within these suppliers’ production or quality control could directly constrain Veracyte’s ability to meet test demand or deliver timely results.

Moreover, scaling capacity entails navigating intricate inventory management demands that require precise forecasting amidst variable global supply chain dynamics [S1]. Expired inventory controls and reagent shelf life impose additional complexity in stockholding strategies critical for maintaining margins.

The company operates its flagship Prosigna Breast Cancer Assay on third-party IVD platforms like Nanostring's nCounter Analysis System [S1], binding Veracyte’s expansion capability to external platform support for clinical registration and reagent supply continuity.

These dependencies underscore sector-specific vulnerabilities common among clinical genomics firms dealing with highly specialized lab consumables coupled with stringent CLIA certification constraints limiting where tests may be performed.

Global Expansion Strategy and Diagnostic Product Innovation

Veracyte continues internationalizing its product footprint with the Prosigna assay available globally as an in vitro diagnostic (IVD) test [S1]. However, aligning products to heterogeneous international regulatory standards and local standards of care presents adoption challenges that could throttle growth prospects.

Expansion into new geographic markets entails negotiating diverse reimbursement pathways necessitating clinico-genomic utility evidence packages supported by ongoing clinical validation studies [S1]. Such genomic classifiers are pivotal in driving physician adoption by demonstrating predictive accuracy combined with cost-effectiveness relative to existing standard-of-care diagnostics.

Veracyte also depends on distributor partnerships across Europe, Asia and Latin America for commercial penetration alongside collaborations with clinical laboratories for localized testing services provision [S21]. Optimizing these distribution channels while maintaining quality consistency is vital for sustainable global revenue ramp.

Evolving Reimbursement Landscape and Regulatory Environment

The company holds FDA clearances for several tests but must continuously manage regulatory risks related to labeling requirements applied to its reagents classified often as RUO or IUO (Research/Investigational Use Only). Improper classification or enforcement could jeopardize supply continuity or trigger compliance actions [S15].

Navigating U.S.-centered regulations—such as CLIA certification requirements enabling high-complexity lab testing—and federal anti-kickback statutes is critical given their potential to affect billing practices for Medicare and private payers [S7]. These laws require vigilance surrounding remuneration arrangements with healthcare providers to avoid False Claims Act violations which carry high penalties [S5][S7][S25].

Internationally, disparate certification regimes necessitate careful product registration logistics while managing local payer mix complexities 영향해 reimbursement timelines impacting sales adoption curves.[S17]

Capital Allocation: Cash Flow Strength, Dividends, and Buybacks

Despite the sizeable net income surge in FY2025 to $66.4 million (ROE approximately 5.1%) [F1], Veracyte has not initiated dividend payments or share repurchases historically nor announced such plans recently [S19]. Instead, it emphasizes retaining earnings to support product pipeline investments plus commercial infrastructure scaling.

Robust free cash flow generation—approximately $126.6 million after subtracting capex from CFO—affords a solid liquidity runway that supports R&D outlays required for developing novel diagnostics while sustaining manufacturing capacity expansions amid supply chain securing efforts [F1][S19].

Given ongoing capex moderation alongside revenue growth indications reported publicly (though dated) [N1][N2], capital discipline appears calibrated to balance growth versus operational risk mitigation.

Market Expectations and Key Milestones to Monitor

Explicit forecasts remain undisclosed publicly; however analysts should track scalability of manufacturing relationships that affect kit availability directly tied to volume ramp-ups reported during recent earnings calls [N3]. Timing approvals or adaptations of existing tests onto alternative IVD platforms will indicate progress unlocking new regional markets beyond current reach [S1].

Expanding contracted laboratory networks especially across physician-owned labs offering Prosigna services may create incremental sales channels impacting top-line trajectory over medium term.[S21]

Adoption metrics tied to reimbursements under evolving managed care payer policies will also be telling markers reflective of broader healthcare payment environment influences.

Risks on the Horizon: Supplier Reliance, Compliance, and Competitive Pressures

Supplier concentration remains a significant vulnerability with sole-source dependency constraining both volume scaling agility and product cost structure stability; transitioning suppliers is non-trivial given proprietary reagent compositions tailored for specific assays [S1][S5].

Regulatory compliance complexity spans multiple domains—anti-fraud legislation including False Claims Act scrutiny intensified via whistleblower provisions poses legal exposure with potential financial damages as well as reputational risk [S7][S20]. Furthermore uncertainties around evolving AI integration within diagnostics impose both innovation opportunity costs plus potential compliance oversight burdens related to algorithmic transparency [S27].

Intellectual property litigation risk looms large given competitors’ patent portfolios; defending proprietary genomic classifier technology necessitates ongoing legal resources lest infringement claims impair product commercialization rights or require onerous licensing agreements detrimental to margins.[S8][S14][S28]

Competitive intensity is heightened from molecular diagnostics players incorporating next-generation sequencing (NGS) platforms combined with AI-driven pathology interpretations threatening legacy genomic tests’ differentiation unless Veracyte sustains continuous innovation cadence.[S17][S20]

In summary, while Veracyte exhibits impressive financial recovery underscored by strong profitably metrics, consistent cash flow prints and healthy balance sheet liquidity underpinning capital efficiency; its growth trajectory remains contingent upon successful navigation of supplier dependencies alongside regulatory-complex market access demands buttressed by ongoing product innovation investment. The delicate interplay between these factors ultimately sets the stage for both opportunity capture and risk mitigation necessary in the dynamic clinical genomics arena.

Disclaimer: This analysis is provided solely for informational purposes based on available data as of February 28, 2026 ([F1], [N#], [S#]). It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments