VSee Health Leverages No-Code Telehealth Platform Amid Liquidity and Competitive Pressures

Latest quarterly filing reveals ongoing operational challenges despite strategic platform differentiation and niche tele-ICU services.

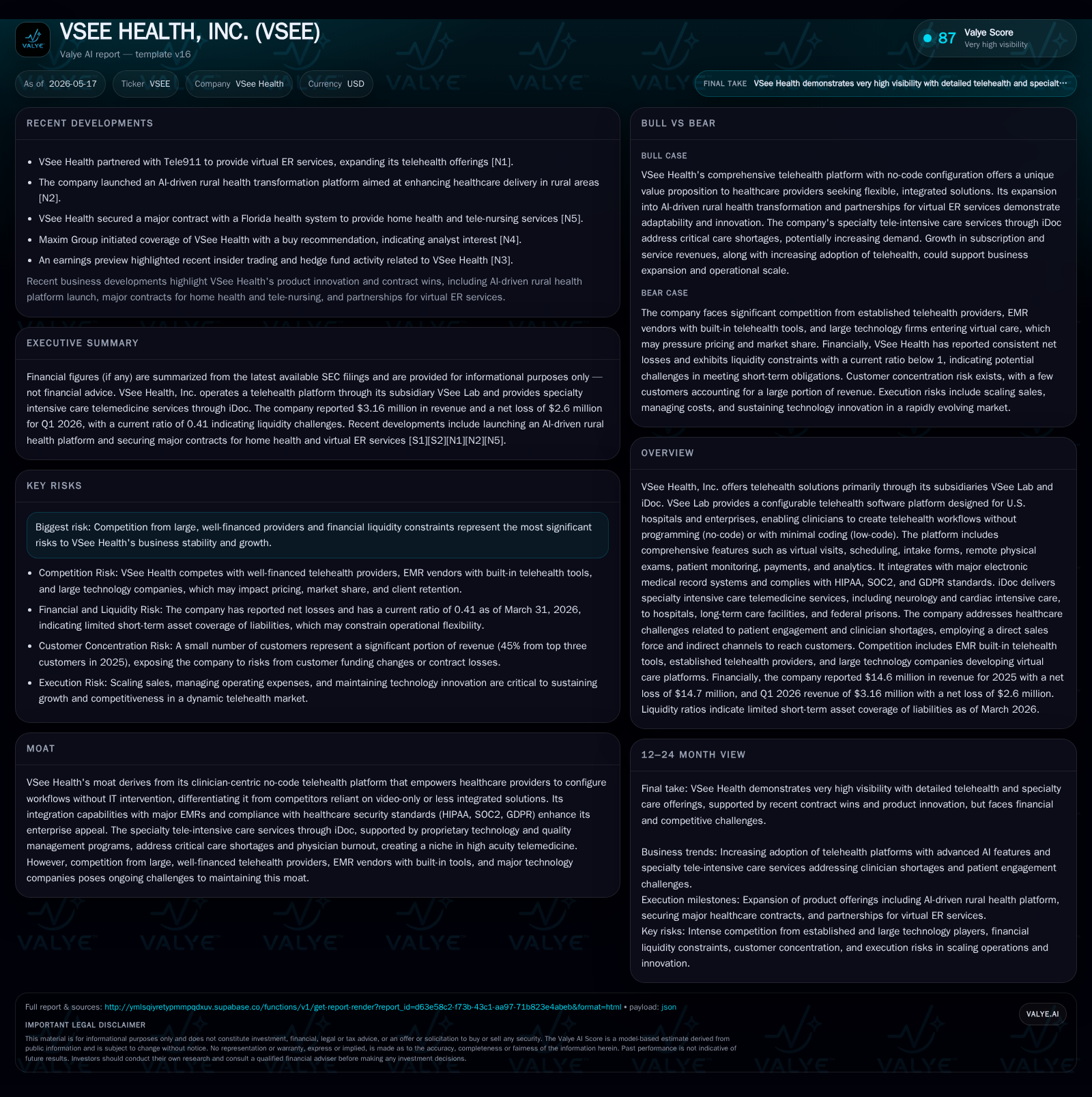

VSee Health, Inc.'s 2026 Q1 filing highlights persistent liquidity constraints and operating losses amid continued investment in its modular telehealth platform and specialty tele-intensive care services. The company’s business model centers on enabling clinicians to configure telehealth workflows through a no-code/low-code software platform integrated with major EMRs, complemented by high-acuity care offerings via iDoc. While this clinician-centric approach and extensive API integrations constitute strategic strengths that differentiate VSee from video-only competitors and home-grown solutions, it faces stiff competition from large, well-financed incumbents and healthcare systems developing proprietary tools. Growth depends on expanding enterprise adoption of its configurable platform and deepening penetration in critical care telemedicine, but financial sustainability remains a concern given ongoing operating losses and suboptimal liquidity ratios.

Recent Operating Update

VSee Health’s latest quarterly filing for the period ending March 31, 2026 [S2] confirms continuation of key operational patterns observed in the preceding annual report [S1]. The company reported no new unregistered securities issuances during Q1 and no defaults on senior securities. Yet management reiterated substantial doubt concerning its ability to continue as a going concern within one year given persistent operating losses and cash flow deficits.

Despite incremental progress raising approximately $8.4 million through financing activities in 2025 [S14], VSee held cash & equivalents of $1.35 million as of March 31, 2026 [F1], underscoring tight liquidity versus elevated current liabilities exceeding $11.7 million [F1], resulting in a constrained current ratio of approximately 0.41 [F1]. This financial backdrop frames the necessity for execution discipline on growth drivers while managing working capital carefully.

Business Model Overview

VSee Health operates principally through two subsidiaries: VSee Lab and iDoc.

VSee Lab delivers a sophisticated telehealth software platform targeting U.S.-based hospitals and large enterprises that enables clinicians to rapidly create or tailor telehealth workflows without programming expertise (no-code) or with minimal coding support (low-code) [S1]. This no-code/low-code paradigm is a strategic differentiator facilitating agility within clinical environments typically hindered by IT delays.

The platform bundles modular software building blocks covering end-to-end telehealth functions: on-demand virtual visits, appointment scheduling, patient intake forms including compliant consent capture, team collaboration tools, remote physical examination interfaces integrated with medical devices, remote patient monitoring dashboards, payment processing including insurance claims, clinical documentation support, administrative controls with analytics on patient satisfaction and operational KPIs.

These components connect natively with leading electronic medical record (EMR) systems such as EPIC and Cerner via HL7/FHIR protocols ensuring interoperability [S1]. Security compliance includes HIPAA adherence supplemented by SOC2 audits and GDPR considerations alongside enterprise-grade access controls like SSO and MFA.

iDoc focuses on delivering high-acuity physician services via tele-intensive care units specializing in neurology (neurointensivists), cardiac surgical/anesthesia intensivists, and pulmonary critical care experts within hospital ICUs as well as offering coverage to long-term care facilities and federal prisons [S1]. This addresses specialized physician shortages exacerbated post-COVID-19 while mitigating clinician burnout through remote expert availability.

Revenue is driven primarily by contractual agreements with healthcare providers—hospitals adopting the software-as-a-service (SaaS) model for VSee Lab platforms—and service contracts for iDoc’s intensivist consultative support. Customer payments reflect subscriptions/licenses for platform access plus fee-for-service or retainer arrangements for critical care physician coverage. Growth hinges on increasing adoption volumes across hospital departments and health systems alongside expanding specialty ICU service penetration.

Industry Structure & Competitive Position

The telehealth market is rapidly evolving with multiple competing strata:

Integrated EMR vendors: Most major EMRs now embed basic telehealth capabilities typically limited to video conferencing links (e.g., Zoom/MS Teams integration). VSee competes here by offering deeper workflow configurability beyond video — enabling rapid customization without IT intervention — which positions it as a complementary extension to EMR functions rather than a pure substitute [S17][S20].

Large Telehealth Providers: Established firms such as Teladoc Health (including InTouch Health) and AmWell hold mature client bases with broad service portfolios. VSee’s emphasis on configurability aims at capturing clients seeking more customizable platforms.

Homegrown Solutions: Some hospitals commission bespoke internal platforms built by sizable engineering teams—often costly with multi-quarter/year timelines. VSee leverages its no-/low-code modular blocks to offer an out-of-the-box alternative promising faster implementation.

Technology Giants & New Entrants: Google Health, Microsoft Healthcare Cloud offerings, Amazon Care initiatives represent significant potential disruptors capable of deploying vast capital into integrated virtual care ecosystems [S20].

Tele-ICU Specialists: Within iDoc’s segment focused on telemetry-based intensivist coverage for critical care units, competitors include Hicuity Health, INTELEICU, enVision (a segment of INOVA). iDoc differentiates itself through purpose-built acute care platforms offering scalable configurable workflows supported by board-certified physician networks optimized for diverse critical care needs [S17].

The competitive moat largely derives from VSee’s clinician-empowering no-code design reducing IT dependency—a notable pain point industrywide—plus extensive API integrations creating ecosystem stickiness with payors and hospital technology stacks. However, entrenched relationships among larger incumbents coupled with resource gaps impose headwinds.

Growth Drivers

Growth vectors rest on several pillars:

Enterprise Expansion: Penetrating additional hospital systems leveraging VSee Lab’s configurable platform addressing unmet needs not fully served by rigid EMR tools or video-only solutions; expanding user adoption of tailored workflows directly translates into increased subscription revenue streams.

Integration Depth & Platform Stickiness: Enhancing API connectivity breadth to payors (insurance), third-party apps (lab results), medical devices (remote monitors), improving switching costs due to integration complexity.

Specialty Tele-Intensive Care Demand: Rising reliance on expert remote intensivists through iDoc driven by nationwide shortage of critical care physicians enhances service contracts; the post-pandemic context accelerates institutional recognition of tele-ICU value in mitigating burnout while improving ICU outcomes.

Regulatory Tailwinds: Ongoing loosening of U.S. telehealth reimbursement policies coupled with increasing state-level acceptance fosters broader adoption windows though this carries patchwork complexity risks.

Risks & Growth Constraints

Material risks encompass:

Financial Sustainability: Continuing operating losses ($9.58 million operating loss FY25) and accumulated deficits ($82.4 million as of FY25) coupled with modest liquidity ($1.35 million cash vs $11.7 million current liabilities) pose short-term solvency pressures that could constrain investment ability subject to capital market access [F1][S1][S2]

Intensifying Competition: Larger players wield significant resources for aggressive pricing promotions or product enhancements potentially eroding VSee’s market share or compressing margins; emerging tech conglomerates further raise innovation bar.

Regulatory Compliance Complexity: Fragmented U.S. state-level regulations around telemedicine delivery modes require continuous operational adjustments; adverse regulatory rulings could impair geographic expansion or increase compliance costs [S6][S10][S12].

Customer Adoption Risks: Entrenched legacy workflows resistant to change plus possible inertia favoring incumbent EMR vendors’ native modules limit rapid uptake; switching entails nontrivial coordination expenses.

What to Watch Next

Attention should focus on:

Quarterly updates revealing any improvements in cash flow dynamics or fresh financing activities reducing going concern doubts.

Client acquisition momentum metrics within hospital systems reflecting the traction of no-code configurable platforms against standard video conference substitutes.

Uptake rates in specialty ICUs served through iDoc reflecting how well the company captures this clinically demanding niche.

Product development announcements confirming further enhancements that broaden workflow automation scope or deepen ecosystem interoperability.

Regulatory developments at federal/state levels that could materially affect reimbursement frameworks or usage modalities impacting revenue growth pathways.

Financial Profile Snapshot

As of March 31, 2026, VSee held approximately $1.35 million in cash versus nearly $11.8 million in current liabilities yielding a current ratio near 0.41—pointing toward liquidity challenges [F1]. Total debt stood modest at roughly $304 thousand against cash reserves indicating low gross leverage but working capital imbalance remains unfavorable [F1].

Full-year 2025 results showed revenue at about $14.6 million but an operating loss near $9.58 million persisted along with net losses around $14.7 million—reflecting ongoing scaling costs post-iDoc acquisition alongside continued investments into product capability [F1][S8]. Such losses mirror industry typical upfront spending profiles but underscore necessity for disciplined financial management alongside growth execution.

Disclaimer: This analysis is based solely upon information available as of the referenced SEC filings dated May 15 and March 31, 2026 ([S2],[S1]), complemented by company factual data ([F1]). It does not constitute investment advice or research views regarding securities of VSee Health Inc.

Financial position in context

As of 2026-03-31, companyfacts shows $1346132 in cash and equivalents [F1]. Current assets of $5mm and current liabilities of $12mm imply a current ratio near 0.41x for 2026-03-31 [F1].

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments