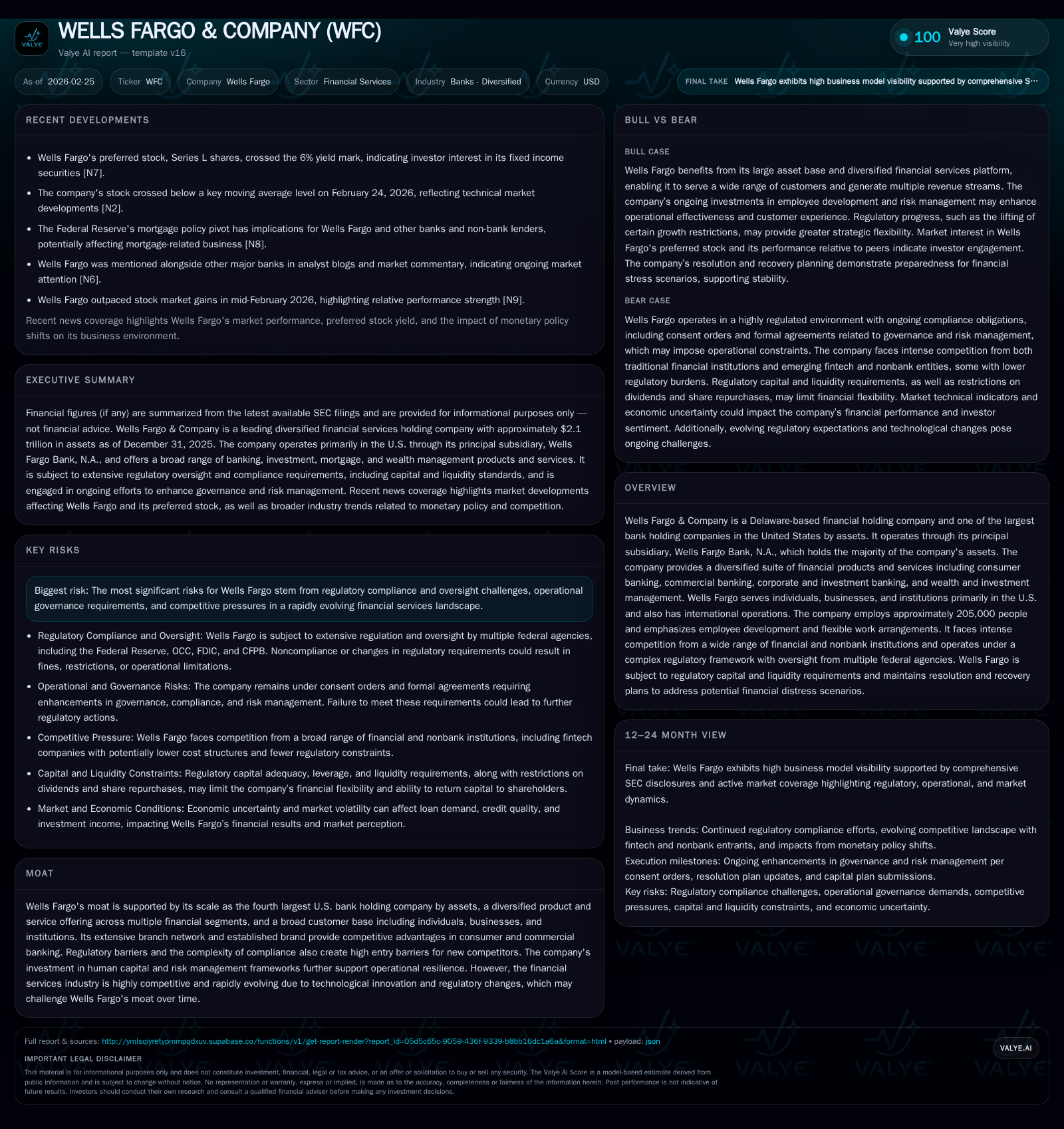

Wells Fargo & Company Shows Resilience Amid Capital and Regulatory Challenges

Wells Fargo balances scale-driven growth with regulatory compliance and capital discipline in a competitive U.S. banking market.

Wells Fargo stands as the fourth-largest U.S. bank by assets, demonstrating steady net income growth despite modest revenue contraction in 2025. The company’s diversified business segments and extensive branch network underpin its competitive moat, although legacy governance challenges and regulatory demands continue to shape strategic execution. Capital management remains disciplined with robust equity levels, sizable share repurchases, and dividend growth aligned with an estimated 11.8% ROE. Upcoming regulatory milestones and macroeconomic uncertainties represent key factors for future operational and financial performance monitoring.

Historical Performance and Business Mix Evolution

Historical performance (annual)

| FY | Net ($bn) | CFO ($bn) | Net YoY |

|---|---|---|---|

| 2025 | 21.3 | -19.0 | +8.2% |

| 2024 | 19.7 | 3.0 | +3.0% |

| 2023 | 19.1 | 40.4 | +45.2% |

| 2022 | 13.2 | 27.0 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, OpInc, Capex, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($bn) | Buybacks ($bn) | ROE% |

|---|---|---|---|

| 2025 | 5.4 | 17.5 | 11.8 |

| 2024 | 5.1 | 19.4 | 11.0 |

| 2023 | 4.8 | 11.9 | 10.3 |

| 2022 | 4.2 | 6.0 | 7.3 |

Source: SEC companyfacts cache [F1].

Wells Fargo & Company has exhibited a nuanced financial trajectory over recent fiscal years marked by resilient profitability despite headwinds impacting top-line growth. With revenues approximately stable around $85 billion from FY2017 through FY2019 ([F1]), the company’s net income notably improved from $13.2 billion in FY2022 to over $21 billion by FY2025, representing an 8.2% rise year-over-year between 2024 and 2025 ([F1]). This increase signals effective cost management and/or improved loan portfolio quality during a challenging interest rate environment.

The loan portfolio near the $1 trillion mark at year-end 2025 underscores its significant role in driving net interest margins (NIM). The bank’s geographic concentration primarily within the U.S., particularly through Wells Fargo Bank, N.A., exposes it to regional economic cycles but leverages its deep commercial banking footprint ([S1], [S5]). The evolution toward a diversified segment mix encompassing Consumer Banking & Lending, Commercial Banking, Corporate & Investment Banking, and Wealth & Investment Management solidifies cross-selling opportunities but also distributes regulatory complexity ([S5], [S12]).

| FY | Revenue ($B) | Rev YoY % | Net Income ($B) | Net YoY % | CFO ($B) | Equity ($B) | Div ($B) | Buybacks ($B) |

|---|---|---|---|---|---|---|---|---|

| 2019 | 85.06 | - | - | - | - | - | - | - |

| 2022 | - | - | 13.18 | - | 27.05 | 179.89 | 4.18 | 6.03 |

| 2023 | - | - | 19.14 | +45% | 40.36 | 185.74 | 4.79 | 11.85 |

| 2024 | - | - | 19.72 | +3% | 3.04 | 179.12 | 5.13 | 19.45 |

| 2025 | - | -1.6% | 21.34 | +8% | -19.00 | 181.12 | 5.43 | 17.52 |

*Note: Revenue data prior to FY2022 unavailable; Operating income and Capex data not available.

Regulatory Environment and Risk Management Progress

Wells Fargo continues to operate under a complex regulatory landscape shaped by historical governance lapses that culminated in Federal Reserve Board (FRB) consent orders focusing on governance oversight improvements ([S7]). The landmark removal of asset growth limits imposed since early-2018 was confirmed in mid-2025, evidencing progress in compliance remediation efforts ([S7], [S22]). Nonetheless, stringent formal agreements on anti-money laundering (AML) reforms with the Office of the Comptroller of the Currency (OCC) remain active as of late-2024 ([S22]).

The company maintains adherence to Basel III capital frameworks complemented by supplemental leverage ratio mandates along with liquidity coverage ratio (LCR) requirements—benchmarks critical for systemic risk mitigation among G-SIBs like Wells Fargo ([S13], [S19]). Stress testing exercises mandated annually assess resilience to severe economic downturns, serving as pillars for recovery planning ([S9]). The "living will" resolution plan designed for orderly failure scenarios is regularly updated ensuring preparedness for potential systemic shocks ([S9], [S17]).

Capital Structure and Liquidity Framework

Capital management at Wells Fargo reflects disciplined strategy balancing robust equity cushions against efficient leverage usage while complying with regulator-prescribed thresholds such as prompt corrective action triggers ([S4], [S13]). As of December 31, 2025, the company reported stockholders' equity of $181 billion alongside assets totaling roughly $2.1 trillion predominantly held within Wells Fargo Bank, N.A., its principal subsidiary ([F1], [S1], [S6]).

Key structural features include a Support Agreement linking the Parent holding company with its Intermediate Holding Company (IHC) and affiliated subsidiaries facilitating regulated internal asset transfers that ensure operational liquidity during stress situations without excessive intercompany restrictions unless certain triggers are breached ([S6], [S17]). This agreement embodies a single point of entry approach aimed at preserving material operating entities intact through distress events ([S10]).

Liquidity buffers are maintained through high-quality liquid assets aligned with LCR standards overseen by the FRB and OCC ([S13], [S19]). The Parent’s capacity to service debt obligations, fund dividends, or pursue buybacks is regulated via these mechanisms ensuring capital adequacy without jeopardizing subsidiary strength ([S19], [S21]).

Recent Financial Results and Trends

Fiscal year 2025 revealed promising earnings gains despite pressures on revenue streams which declined about 1.6% compared to prior year levels ([F1]). The net income advance of approximately +8% indicates enhanced operational efficiency or benefits from credit quality improvements possibly linked to reduced provision expenses or fee-based income contributions.

Conversely, operating cash flows delivered a negative swing exceeding sevenfold decline from positive $3 billion in FY24 to negative $19 billion in FY25 highlighting potential working capital outflows or significant loan portfolio adjustments warranting focused analysis ([F1]). This dichotomy signals divergence between accrual accounting profits versus real-time cash realization that may involve mortgage portfolio repositioning given Federal Reserve policy pivots affecting lending activity ([N9], [N13]).

Equity base remained largely stable around $181 billion underpinning an estimated return on equity near the healthy level of approximately 11.8%, consistent with peer averages while indicating prudent capital utilization ([F1]).

Dividends, Share Repurchases, and Capital Allocation Priorities

Capital return practice at Wells Fargo reflects methodical dividend increases alongside substantial share repurchasing programs supporting shareholder value enhancement within federally mandated limits.[F1] Dividend payments grew steadily from $4.18 billion in FY22 to over $5.4 billion in FY25 complemented by aggressive buyback execution escalating from $6 billion up to over $17 billion in the same timeframe.

These activities occur under tight scrutiny from regulators emphasizing sustainable payout ratios aligned with ongoing capital needs especially amid periodic FRB stress tests constraining distributions if adverse conditions persist ([S7], [S19]). The bank’s current payout pattern balances rewarding investors while retaining capital flexibility necessary for operational contingency funding.

Forward-Looking Themes and Market Expectations

While Wells Fargo has not issued explicit forward guidance recently publicly available, market commentary highlights attention toward preferred stock yields which crossed above significant yield thresholds (e.g., >6%), providing alternative return instruments amid uncertain macroeconomic backdrops with mixed sentiment across broad financial stocks including Wells Fargo ([N7], [N12], [N14]). Analysts remain keenly focused on margin expansion opportunities through lending repricing capabilities coupled with asset growth prospects contingent on favorable interest rate environments ([N8], [N10]).

Regulatory developments such as potential changes in community reinvestment assessments or AML enforcement approaches may influence strategic resource allocation decisions moving forward.

Strategic Challenges in Competitive and Regulatory Contexts

Wells Fargo faces sustained pressure from emerging fintech disruptors leveraging technology-enabled direct-to-consumer platforms reducing reliance on traditional branch banking models while benefiting from less onerous regulatory overheads—a dynamic reshaping competitive contours for legacy institutions (, [S15]).

Maintaining regulatory compliance culture improvements alongside technology modernization investments remains pivotal to safeguarding operational resilience ([S7], [S8], [S24]). Balancing legacy infrastructure scalability against digital innovation imperatives requires navigating risk governance structures that have historically attracted intense regulator attention.

Key Metrics to Monitor for Upcoming Quarters

Analysts should track deposit growth rates as indicators of liquidity strength versus systemic outflows possibly induced by digital currency adoption or fintech competition; charge-off trends signaling credit environment health; liquidity coverage ratio movements revealing buffer adequacy; resolution plan updates reflective of stress readiness; and any announced adjustments to capital return policies informing shareholder yield considerations.

Monitoring sensitivity to Federal Reserve monetary policy moves will provide further clarity on margin sustainability given loan repricing lags typical within large diversified bank portfolios.

This analysis synthesizes publicly available data without offering investment recommendations or price forecasts and rests solely on documented facts as per cited sources through February 25, 2026.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments