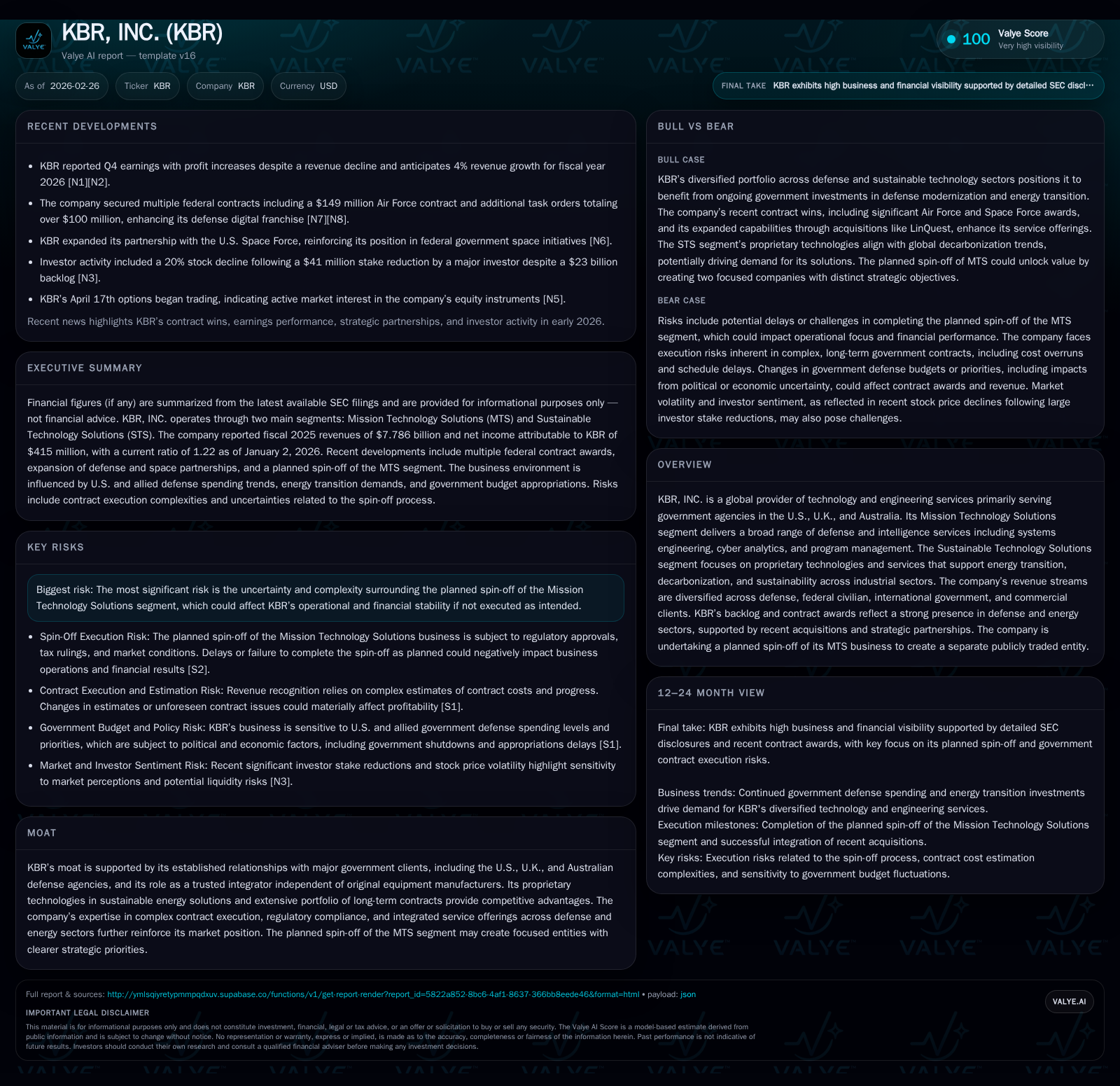

KBR’s 2025 Growth Moderated by Spin-Off Plans and Defense Sector Dynamics

The company posted modest revenue growth with robust operating income gains despite near-term headwinds, while preparing for a major organizational transformation.

KBR, Inc. reported fiscal 2025 revenues of $7.79 billion, a slight 1% increase over 2024, driven by gains in defense and sustainable technology despite softness in some international and science/space programs [F1][S27]. Operating income rose 17.5% to $778 million, supported by operational improvements and acquisitions [F1][S11]. The company is advancing its planned spin-off of the Mission Technology Solutions (MTS) segment, aiming for mid-to-late 2026 completion, which presents both strategic focus opportunities and execution risks [S2]. Its backlog remains strong at approximately $13.3 billion, underpinning stable near-term revenue visibility [S19][S25]. Capital allocation reflects disciplined buybacks and dividend growth, with free cash flow around $420 million, supporting financial flexibility [F1][S12].

Historical Performance: Steady Revenue Growth with Margin Expansion

Over the four-year historical window from 2022 through 2025, KBR reported steady top-line growth driven mainly by its Mission Technology Solutions segment. Revenues increased from approximately $6.96 billion in fiscal 2023 to $7.79 billion in fiscal 2025, representing a compounded annual growth rate near 6%. The MTS segment accounted for roughly three-quarters of revenues during this period, anchored by federal defense contracts primarily from U.S., U.K., and Australian agencies [F1][S4]. In parallel, the Sustainable Technology Solutions business has expanded steadily from about $1.84 billion to $2.21 billion over the same timeframe as energy transition markets develop.

The company's operating income demonstrated marked improvement rising from $343 million in fiscal 2022 up to $778 million in fiscal 2025 (+17.5% YoY in latest year). The margin expansion is attributable to operational efficiencies, better contract mix favoring higher-margin digital/technology services via the LinQuest acquisition (completed August 2024), and price discipline amid inflationary pressures [F1][S11]. Net income followed suit recovering strongly from a loss position in fiscal 2023 (-$265 million) back into positive territory of $415 million in fiscal 2025 aligned with profitable contract execution.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 415 | 778 | 42 | +10.7% | |

| 2024 | 375 | 462 | 662 | 77 | +241.5% |

| 2023 | -265 | 331 | 448 | 80 | -239.5% |

| 2022 | 190 | 396 | 343 | 71 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 84 | 329 | |

| 2024 | 79 | 218 | 385 |

| 2023 | 72 | 138 | 251 |

| 2022 | 66 | 203 | 325 |

Source: SEC companyfacts cache [F1].

Note: CFO data available only for select years; buyback trends show acceleration into fiscal year-end.

Segment Dynamics: Defense Backbone Meets Sustainable Innovation

KBR’s two core reportable segments define its portfolio:

Mission Technology Solutions (MTS): Constitutes about two-thirds of total revenue (~$5.58 billion in FY25), providing integrated engineering, cyber analytics, systems integration and program management services primarily for government defense clients including the U.S. Department of Defense (DoD), NASA, UK Ministry of Defence (MoD), and Australian Defence Department [S4][S5]. Defense customers represented approximately two-thirds of total revenues with a growing emphasis on technology-driven mission support including space domain awareness and intelligence solutions.

Sustainable Technology Solutions (STS): Represents nearly one-third of revenue (~$2.2 billion in FY25), focused on proprietary process technologies aimed at decarbonization across ammonia/syngas production, petrochemicals refining, circular economy initiatives and advisory consulting services targeting energy security challenges globally [S4][S5]. This segment benefits from accelerating demand driven by customers’ climate goals amid regulatory pressures.

Contracts vary across fixed-price, time-and-materials, and cost-reimbursable types—with government contracts predominantly cost reimbursable ensuring stability though requiring strict performance management under FAR/CAS compliance regimes [S19].

Backlog Visibility and Contractual Profile

KBR reported total remaining performance obligations (backlog) at approximately $13.3 billion as of fiscal year-end January 2026 [S19][S25]. Of this amount:

- About 36% is expected to convert into revenue within one year.

- Roughly 41% will realize between years two through five.

- The remaining 23% extends beyond five years, reflecting the long duration nature of select contracts like the Aspire Defence project through to the early 2040s.

The backlog remains heavily weighted towards defense programs backed by multiyear appropriations underpinned by recent Congressional funding including an $839 billion discretionary defense spending bill for FY26 finalized early February along with an authorized NDAA budget totaling approximately $901 billion [S1][S24]. These appropriations provide a relatively firm base but political dynamics continue to inject uncertainty into future budget cycles due to debates on spending priorities.

Internationally, KBR has fortified its presence particularly within U.K. MoD’s Strategic Defence Review framework emphasizing AI development, space superiority and cyber defense enhancements while Australia continues raising defense budgets addressing regional security concerns [S24].

Spin-Off Strategy: Catalyst or Complexity?

A pivotal corporate event on the horizon is KBR's announced plan to spin off its Mission Technology Solutions segment into a separate publicly traded company targeted for mid-to-late calendar year 2026 completion [S2]. This move intends to create two focused entities:

- A leaner Sustainable Technology Solutions entity prioritizing energy transition innovations.

- An independent Mission Technology company concentrating on defense/intelligence services with potential for targeted capital deployment.

While the spin-off could unlock shareholder value through enhanced strategic clarity and operational focus, it also brings considerable execution risk:

- Regulatory approvals including tax rulings must align favorably to maintain tax-free status.

- Market conditions could delay or complicate separation financing.

- Incremental expenses related to infrastructure setup may pressure near-term profitability.

- Management bandwidth diverted during separation might impact ongoing contract delivery effectiveness.

Investors should monitor updates on Board authorization milestones, registration statement filings with the SEC, legal counsel opinions concerning tax implications and progress toward establishing standalone operations infrastructure [S2].[N5]

Financial Health and Capital Allocation

Liquidity remains sound with cash and cash equivalents around $500 million as of January end FY25 while total debt approximates $2.60 billion dominated by Term Loan facilities maturing between August ’27 and January ’31 as well as senior notes due ’28 [F1][S9][S10][S14]. The company is compliant with leverage covenants under its Senior Credit Facility enabling financial flexibility.

Operating cash flow grew impressively (+~40%) reaching high three-hundred millions supported by working capital management Improvements post government shutdown disruptions during late FY25 [F1][N1] Capex spending decreased substantially YoY (down ~45%), totaling $42 million consistent with asset-light business model emphasizing services over heavy capital intensity [F1].

KBR returned capital actively via dividends totaling $84 million (+~7% YoY) alongside accelerated share repurchases aggregating approximately $329 million—reflecting prudent stewardship aligned with maintaining net leverage targets while rewarding shareholders [F1][S12][N5].

Approximate Return On Equity stands robust at ~27.6%, signaling efficient deployment of equity given profitable margin profiles across business lines.[F1]

Risks: Execution Uncertainties Weigh on Outlook

The foremost risk factors remain tied to:

- Successful execution of the MTS spin-off without material disruption or loss of key personnel/contracts being critical yet inherently uncertain due to regulatory dependencies and market volatility risks detailed in filings [S2].

- Government contracting risks such as audits by DCAA/DCMA could retroactively challenge cost allocations or billing rates.[S7]

- Political controversies impacting defense budgets—though FY26 appropriations are supportive, longer-term spending remains exposed to macroeconomic inflation pressures as well as shifts in administration priorities rendering forward visibility limited.[S24]

- Legacy contract closeout matters related to war-time support such as LogCAP III entail ongoing claims resolution posing potential contingent liabilities.[S16]

- Supply chain interruptions or procurement delays can influence project timing especially within international programs driven by diverse geopolitical contexts.[N4]

Overall however KBR’s strong longstanding relationships established with U.S., U.K., Australian governments coupled with its capabilities as an OEM-independent integrator reinforce competitive moats mitigating typical industry cyclicality challenges.

This analysis summarizes available public data as of February 2026 and does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments