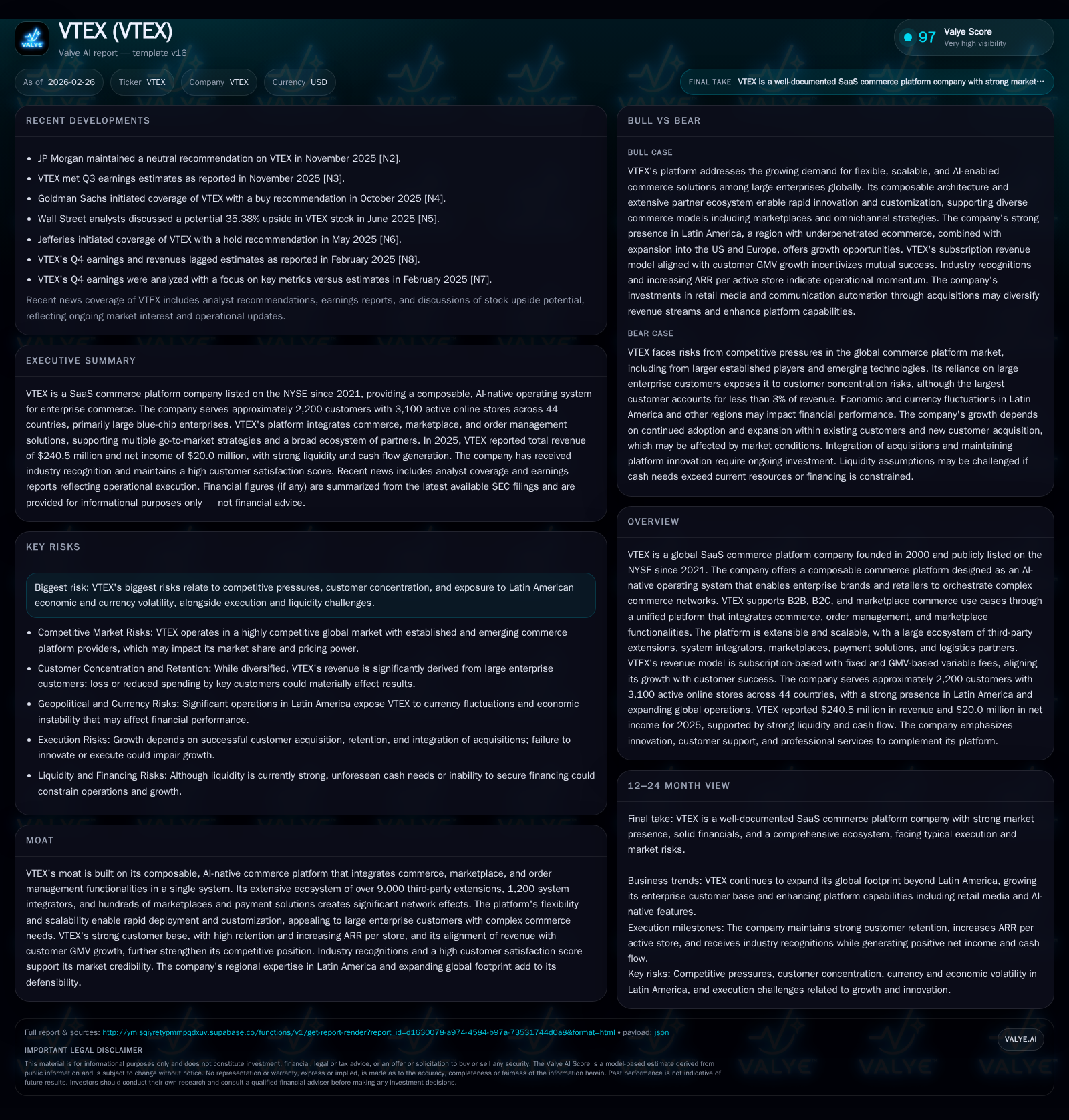

VTEX Strengthens Global Enterprise Commerce with AI-Driven Platform and Sustained Profitability Growth

VTEX expanded its international footprint and enterprise customer base, achieving double-digit revenue growth and record profitability through AI innovation and strategic reinvestment in 2025.

Founded in 2000, VTEX offers a composable commerce SaaS platform integrating commerce, marketplace, and order management systems tailored for large enterprises. While historically dominating Latin America’s underpenetrated eCommerce market, VTEX is rapidly scaling its US and European presence, focusing on high-value customers contributing increasing annual recurring revenue. Its revenue model links with client GMV growth, supporting a sustainable expansion despite macroeconomic headwinds in Latin America. Notably, the company reported 12.5% revenue growth in 2024 and achieved record profitability in 2025 amid strategic reinvestments in R&D and AI capabilities. Capital allocation emphasizes share repurchases without a formal dividend policy, underscoring confidence in long-term enterprise value creation.

Company Overview

VTEX was founded in 2000 and has evolved from its origins as a Brazil-centric player consolidating as a SaaS commerce platform by 2010 to a publicly traded entity on the NYSE since mid-2021 [S1][S5]. It provides an AI-native composable commerce platform that unifies traditional eCommerce with marketplace and order management solutions under one operable system designed for enterprises [S6][S8]. VTEX’s technology supports multiple business models—B2C, B2B, and marketplaces—with extensive third-party ecosystem integration comprising over 9,000 extensions and more than a thousand systems integrators globally [S9][S13].

The platform emphasizes flexibility via low-code customization capabilities while maintaining scalability to meet complex requirements of large brands across various verticals including home appliances, apparel, beauty products, electronics, groceries, and furniture [S14][S18]. In reinforcing omnichannel experiences for clients' end-consumers, VTEX enables integrations ranging from web storefronts to live shopping and conversational commerce—blending human assistance with AI-powered automation [S6][S10][S11].

Historical Growth and Financial Performance

From FY2021 to FY2024 VTEX posted consistent revenue growth from $125.8 million to $226.7 million—an approximate compound annual increase near 21%—anchored primarily by growing subscription revenue aligned with GMV expansion across its client base [F1][S3]. Gross Merchandise Value (GMV), which VTEX uses as a key operating performance indicator given its transaction-based revenue model, climbed to over $20 billion processed through the platform by the end of calendar year 2025 [S1][S3]. This rises amid favorable long-term trends such as increasing digital adoption worldwide but particularly in Latin America where eCommerce penetration remains at an estimated ~11.4% compared to above 16% in the US—a structural tailwind for VTEX’s LatAm-dominant footprint [S17].

Same-store sales (SSS) metrics indicate steady sales volume growth within existing stores—a healthy sign of customer retention and expansion—with FX-neutral SSS rates at +6.8% in 2025 post double-digit gains exceeding +10% annually over previous years [S1]. The number of top-tier customers generating ARR above $250k rose steadily to nearly 160 entities by the end of 2025 with this cohort growing subscription revenues by about +13% YoY [S14][S16]. This reflects an ongoing maturation toward higher-value clients expanding their deployment across multiple online stores.

Historical performance (annual)

| FY | Rev ($mm) | Rev YoY |

|---|---|---|

| 2025 | ||

| 2024 | 227 | +12.5% |

| 2023 | 202 | +27.8% |

| 2022 | 158 | +25.3% |

Source: SEC companyfacts cache [F1].

Note: Operating income and net income shown below are latest figures available for FY25 per filings but prior years are not fully detailed [F1].

In FY25 VTEX achieved non-GAAP operating income of approximately $18.1 million along with net income around $20 million driven by operational efficiencies balanced against an intentional ramp of R&D spending to deepen AI capabilities and expand Retail Media offerings.[S3][F1]

Future Growth Prospects

VTEX identifies several strategic growth vectors:

- Continued geographic expansion beyond Latin America particularly into the U.S. and Europe supported by localized sales teams and regional infrastructure investments [S7][S21]

- Broadening adoption among large enterprise customers who deploy multiple stores across regions—as average number of stores per top-100 customer doubled from about two to five between 2017-2025—signaling room for further cross-selling opportunities [S22]

- Growth of emerging product lines such as Retail Media advertising integrated natively within their commerce ecosystem providing brands ways to monetize digital shelf space [S11]

- Accelerating B2B digitization fueled by composable architecture allowing clients to build bespoke workflows quickly leveraging VTEX IO customization platform [S3]

- Leveraging embedded AI functionalities spanning pricing optimization to personalized consumer journeys enhancing conversion rates and operational efficiencies directly within the platform stack [S18]

These factors collectively aim to capture continued global ecommerce expansion projected by analysts to rise from approximately $6.5 trillion in GMV during 2025 to over $8 trillion by late decade [S1][S17]. However challenges persist including intense competition from global cloud commerce incumbents plus risks associated with Latin American economic volatility that could temper spending among core customer segments .

Forecasts / Milestones / Expectations

While formal forward guidance is limited,[N1] milestones to watch include:

- Further acceleration of subscription revenue growth internationally supported by enterprise account wins and expansions.

- Scale-up of Retail Media monetization efforts driving higher recurring revenues beyond core commerce functions.

- Incremental margin improvements through automation leveraging AI investments balancing top-line reinvestment strategies.

- Maintaining or improving gross merchandise value velocity alongside expanding store counts globally. Monitoring quarterly GMV trends on FX-neutral basis will be critical given currency sensitivity especially versus USD.

Returns & Capital Allocation

The firm reported an approximate return on equity around ~8.6% calculated using FY25 net income versus equity [F1], indicating moderate profitability consistent with SaaS companies focusing on reinvestment phases. Free cash flow generation approximates $32 million; cash balances remain solid at about $15.7 million year-end FY25 while current assets cover current liabilities with ratio exceeding three times favoring liquidity [F1][S15].

Capital allocation programs have emphasized share repurchase initiatives—highlighted multiple authorizations since listing culminating in a renewed plan for up to $50 million authorized in early 2026 maturing Feb’27—while dividends have not yet been declared reflecting reinvestment priorities at this stage [S4][S15]. Repurchases exhibit management confidence aiming to optimize capital structure while supporting stock liquidity.

Competitive Moat & Industry Positioning

VTEX’s moat derives predominantly from its advanced composable SaaS architecture combining critical commerce functionalities—marketplace onboarding, distributed order management—with scalability customized via low-code tools catering predominantly to complex enterprise ecosystems [S9][S18]. The expansive partner network comprising thousands of ISVs facilitating seamless integrations creates a formidable network effect enhancing switching costs for customers reliant on this interconnected platform.

Market recognition such as repeated Customer’s Choice distinctions from Gartner voice highlights user satisfaction underpinning strong retention.[S17] Its leadership position within Latin America positions it well to capitalize on rapid regional ecommerce penetration catch-up while steadily diversifying geographic exposure internationally mitigates concentrated sovereign risks.[S16]

Risks and Challenges

Chief risks noted include:

- Escalating competition from multinational SaaS commerce players targeting large enterprises worldwide potentially compressing pricing power.

- Currency fluctuations impacting reported results due to significant revenue base within volatile Latin American currencies despite FX-neutral reporting adjustments.[S17]

- Execution risk associated with scaling new product lines like Retail Media while managing technology complexity inherent to broad composability model.

- Concentration risk as largest clients still contribute disproportionally though diversified portfolio lessens single account dependency ([less than 3% top customer concentration reported]) [F1][S14].

Conclusion

VTEX stands as a compelling example of a regional SaaS leader transforming into a global multi-product commerce platform anchored by deep technological innovation focused on enterprises’ evolving needs for flexible yet comprehensive digital commerce solutions. Its financial trajectory signals solid growth complemented by expanding margins even during reinvestment cycles focused on AI-enhanced product development.

While macroeconomic sensitivities tied primarily to Latin America temper outlook volatility somewhat, the firm’s shift toward global markets expansion coupled with accelerating traction among high-value customers opens avenues for sustainable longer-term growth in line with worldwide ecommerce evolution.

Disclaimer: This analysis is based solely on available public filings and disclosures through February 26th, 2026. It does not constitute investment advice or recommendations but aims to provide grounded insight into VTEX’s business fundamentals and strategic position within digital commerce technology.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments