Weatherford International Reports Resilient Q1 Performance Supported by Offshore Expansion

Q1 2026 results highlight Weatherford's strategic gains in offshore completions amid ongoing sector cyclicality.

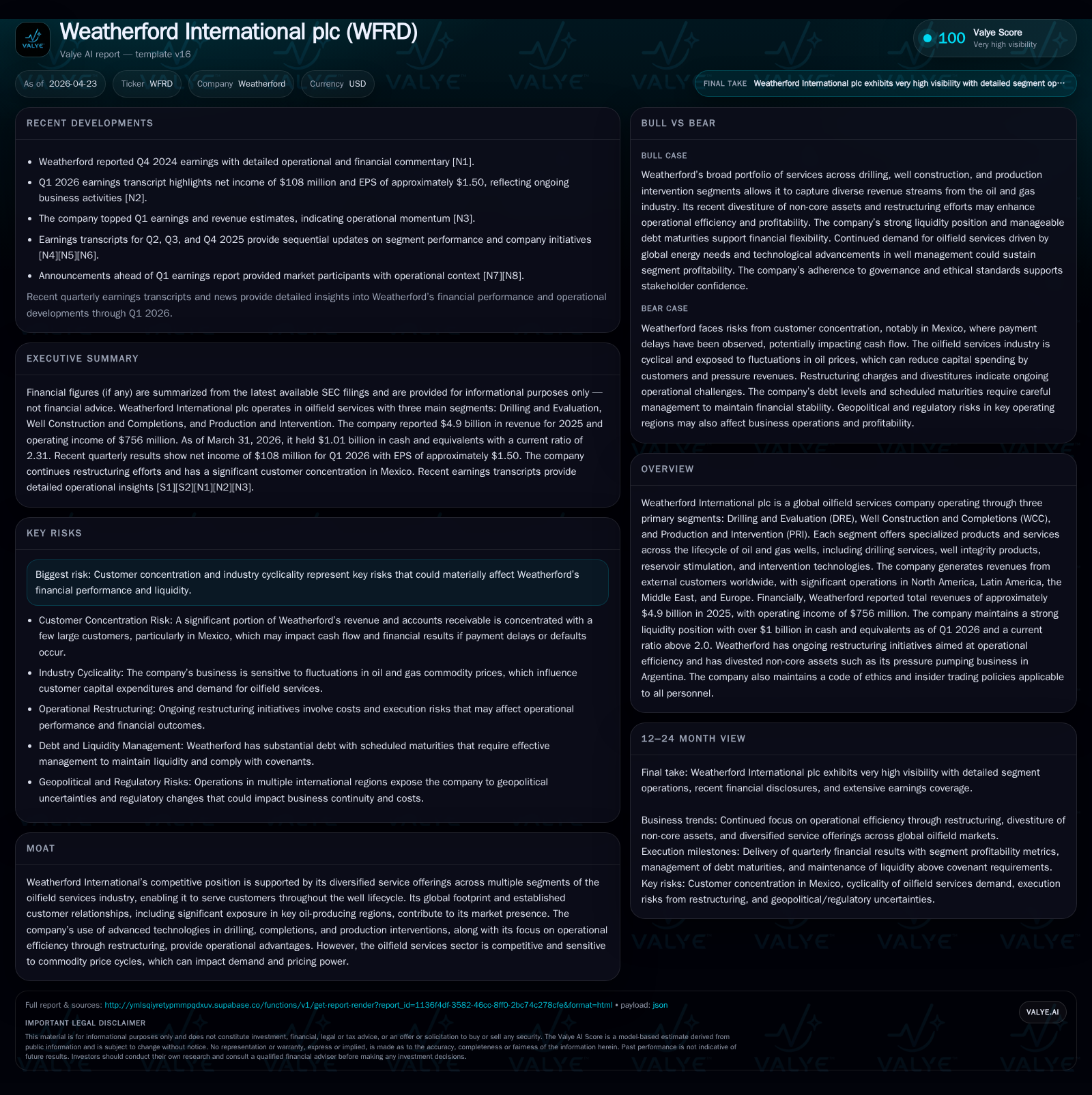

Weatherford International plc delivered robust first-quarter 2026 results with revenues exceeding analyst estimates due primarily to growth in offshore completions. The company’s diversified service lines across the well lifecycle and global footprint, especially in key oil-producing regions, underpin its competitive position despite inherent cyclicality in the oilfield services sector. Operational efficiency efforts and strong liquidity bolster Weatherford’s ability to navigate industry volatility as it targets growth from expanding offshore projects and advanced technology integration.

Q1 2026 Operating Update: Earnings and Strategic Momentum

Weatherford International plc’s first-quarter 2026 filing ([S2]) reveals a resilient performance driven largely by expansion in offshore completions and robust demand across diversified service lines. Reported revenues outpaced consensus estimates ([N3]), reflecting the company's ability to capitalize on an improving offshore market despite broader oil price volatility.

The company’s liquidity position remains healthy, with cash and equivalents exceeding $1 billion as of March 31, 2026 ([F1]). This strong cash buffer supports operational flexibility amid continued market cyclicality. Management commentary highlights ongoing operational efficiencies via restructuring initiatives that have helped contain costs without sacrificing investment in growth areas ([S2],[N2]).

Notably, recent investor communications underscore growth momentum specifically within the Well Construction and Completions (WCC) segment offshore, aligning with geopolitical-driven upstream investment flows ([N14]). This driver is crucial given the capital-intensive nature of offshore projects needing specialized completion technologies to unlock production.

Core Business Model and Segment Quality Across the Well Lifecycle

Weatherford structures its business into three primary reportable segments: Drilling & Evaluation (DRE), Well Construction & Completions (WCC), and Production & Intervention (PRI) ([S1],[S14]). These segments collectively enable end-to-end service coverage throughout the oil and gas well lifecycle—spanning early reservoir assessment to well integrity maintenance and production optimization.

- DRE focuses on drilling services including managed pressure drilling, wireline operations, and drilling fluids aiming at optimizing reservoir access.

- WCC provides essential services for well completion integrity such as tubular running services, cementation products, liner hangers, and advanced completions technologies adaptable to complex environments.

- PRI offers reservoir stimulation designs including artificial lift systems, intervention tools, sub-sea operations support alongside emerging digital solutions.

This vertical integration improves customer retention through high switching costs; clients benefit from a bundled service offering that reduces the complexity of engaging multiple vendors ([S1]). Sustained investments in technology enhance Weatherford’s capabilities particularly in advanced completions and digital interventions where technical differentiation mitigates commoditization risks.

Geographically, the firm is well balanced between North America — representing around 20% of total revenues — and international markets dominated by Latin America, the Middle East/North Africa/Asia region ([S8],[S9]). This geographic diversification cushions against localized downturns but introduces currency exposure and political risk.

Competitive Moat in a Cyclical Oilfield Services Market

Weatherford’s competitive moat derives from its broad service footprint spanning multiple segments of oilfield services coupled with a wide-reaching global network. Its ability to engage customers at various stages across the well lifecycle creates cross-selling opportunities that competitors focused on narrow service niches cannot easily replicate ([S1],[S14]).

However, this sector remains highly cyclical and vulnerable to fluctuations in commodity prices which dictate exploration budgets. Pricing power is subdued during downturns due to intense competition from peers offering similar drilling or completions products. Customer concentration risk also looms large; one Mexican client alone accounted for approximately 24% of outstanding receivables as of year-end 2025 ([S8]), posing collections risk especially given historical late payments documented by management.

Technological innovation serves as a partial hedge against commoditization. Weatherford’s deployment of AI-enabled digital tools for well intervention planning and real-time reservoir monitoring reflects its strategic push towards next-generation value-added services ([N14],[S21]). Yet ongoing restructuring is necessary to maintain cost competitiveness given legacy operational inefficiencies.

Industry Drivers: Pricing Power, Regional Exposure, and Supply Dynamics

The oilfield services industry is strongly influenced by upstream capital expenditure cycles which are exposed to macroeconomic factors including geopolitical tensions such as disruptions near the Strait of Hormuz ([N12]). Such conditions have precipitated higher demand for offshore completions—a focus area for Weatherford evidenced by recent revenue gains ([N14])—as operators seek enhanced reservoir access under complex drilling conditions.

Pricing dynamics remain mixed. While advanced completers can command premium pricing supported by technological differentiation, basic drilling equipment and some intervention tools face margin pressure due to oversupply nuances. Regulatory frameworks differ by region but generally impose operational constraints encouraging providers like Weatherford to invest in compliance infrastructure ([S21]).

Supply chain constraints for specialized equipment—particularly for sub-sea interventions—continue to pose short-term bottlenecks feeding into pricing mix improvements for providers capable of meeting demand promptly ([N14]).

Growth Opportunities and Execution Risks

Key growth levers include expanding offshore drilling projects intensified by geopolitical catalysts; integration of AI-driven analytics for optimized well planning; broadening energy transition-related offerings such as carbon capture support; coupled with continuous internal efficiency drives through restructuring programs noted in the latest filings ([S2],[S21]).

Risk factors remain significant:

- Customer credit exposure linked especially to late-paying major clients,

- Pricing pressures emerging from aggressive competitor bidding,

- Timing uncertainties for capital investments tied closely to crude price forecasts,

- Regulatory changes impacting operating licenses or environmental compliance costs.

Weatherford appears mindful of these execution hazards with stated strategies emphasizing improved receivables monitoring and disciplined capital allocation aimed at preserving financial flexibility ([S21]).

Near-Term Catalysts and What to Watch

Looking forward, critical indicators will include quarterly revenue trajectories particularly from high-margin offshore completions contracts; progress reports on operational restructuring deliverables; updates on any customer concentration mitigation efforts; capital expenditure pacing aligned with contract wins; and advances integrating AI/digital solutions impacting competitive positioning ([N7],[N8],[S3]).

Regulatory or environmental policy shifts affecting key operating locales could also serve as external catalysts or headwinds worth tracking.

Financial Overview Supporting Operational Insights

A summary of key financials provides context for Weatherford’s operating commentary:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 431 | 676 | 756 | 226 | -14.8% |

| 2024 | 506 | 792 | 938 | 299 | +21.3% |

| 2023 | 417 | 832 | 820 | 209 | +1503.8% |

| 2022 | 26 | 349 | 412 | 132 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 72 | 101 | 450 |

| 2024 | 36 | 99 | 493 |

| 2023 | 623 | ||

| 2022 | 217 |

Source: SEC companyfacts cache [F1].

Despite an ~18.8% revenue increase in FY2025 versus FY2024 ([F1]), operating income declined nearly 19.4%, reflecting margin compression possibly due to inflationary cost pressures or mix shifts favoring lower margin volumes. Net income mirrored this downturn at -14.8% YoY while Free Cash Flow approximated $450 million after capex underscoring solid cash generation capability ([F1]).

Weatherford’s debt structure includes long-term Senior Notes maturing mostly post-2030 with manageable near-term maturities ($29 million in 2026) supporting stable leverage profiles ([S4],[S5],[S6],[F1]). Capital allocation has balanced modest share repurchases ($101 million in FY2025) alongside dividend payments ([F1]).

Operating expenses have been controlled through restructuring charges reported recently (~$58 million), signaling management focus on expense discipline amid fluctuating top-line trends ([S23]).

This analysis synthesizes regulatory disclosures alongside market commentary without investment recommendations or forecasts. Financial figures cited are strictly drawn from cited periodic filings or validated data sources. Readers should consider external market developments independently when evaluating Weatherford International plc.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments