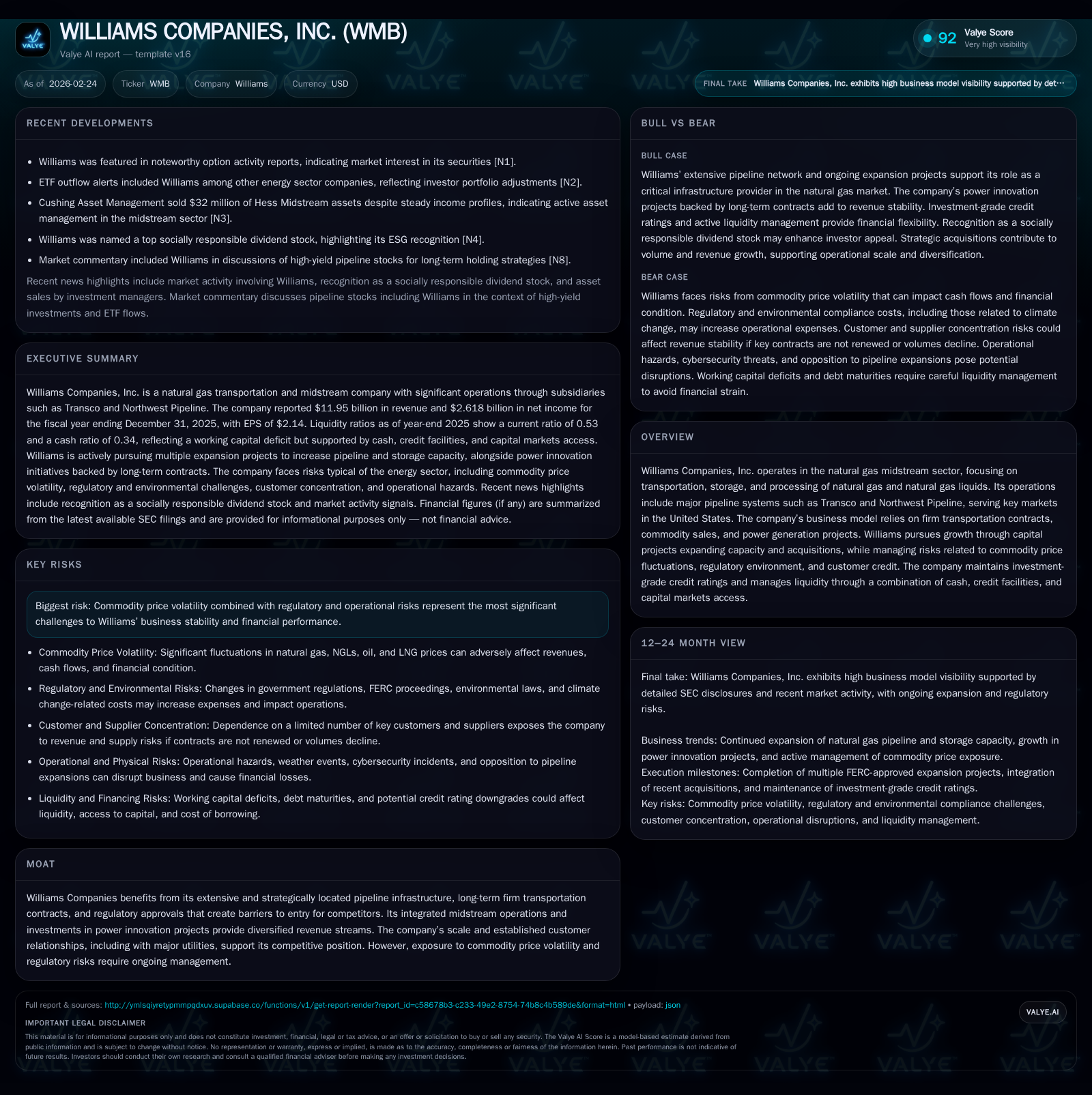

Williams Companies Advances Major Expansion Projects While Managing Elevated Capex and Regulatory Risks

Williams Companies, Inc. drives growth through strategic pipeline expansions and power innovation projects, supported by strong operating cash flow and disciplined capital allocation amid regulatory and market challenges.

Williams Companies has delivered robust revenue and operating income growth driven by capacity expansions and acquisitions, with significant capital projects scheduled between 2025 and 2030 to increase firm transportation capacity substantially. The company maintains investment-grade credit ratings and a consistent dividend policy despite heightened capital expenditures. Key risks include regulatory scrutiny, commodity price volatility, customer concentration, and execution risks on large-scale infrastructure projects.

Historical Financial Performance

Williams Companies has shown solid financial growth over the last four fiscal years ending December 31, 2025. Revenues increased from approximately $10.97 billion in FY2022 to nearly $11.95 billion in FY2025, representing a strong year-over-year growth of 13.8% from FY2024 to FY2025 [F1]. Operating income demonstrated volatility but ultimately rose by 25.7% in FY2025 to about $4.20 billion following a dip in FY2024 due to margin pressures linked to commodity price fluctuations.

Net income mirrored this pattern with a decline in FY2023 offset by recovery to $2.62 billion in FY2025, up 17.7% compared to the prior year [F1]. Cost discipline contributed to these results including modest decreases in depreciation expense relative to revenue.

Historical performance (annual)

| FY | Rev ($bn) | Net ($bn) | CFO ($bn) | OpInc ($bn) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 11.9 | 2.6 | 5.9 | 4.2 | +13.8% | +17.7% |

| 2024 | 10.5 | 2.2 | 5.0 | 3.3 | -3.7% | -30.0% |

| 2023 | 10.9 | 3.2 | 5.9 | 4.3 | -0.5% | +55.1% |

| 2022 | 11.0 | 2.0 | 4.9 | 3.0 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Capex. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($bn) | Buybacks ($mm) | FCF ($bn) |

|---|---|---|---|

| 2025 | 2.4 | 0 | 1.0 |

| 2024 | 2.3 | 0 | 2.4 |

| 2023 | 2.2 | 130 | 3.4 |

| 2022 | 2.1 | 2.6 |

Source: SEC companyfacts cache [F1].

Operating cash flows have remained robust near the $5 billion mark annually, increasing nearly +19% year-over-year to $5.9 billion in FY2025 despite a significant rise in capital expenditures associated with expansion projects [F1]. The elevated capex reflects Williams’ commitment to growth through pipeline capacity additions and power innovation initiatives.

Business Overview

Williams operates primarily in the natural gas midstream sector, including transportation, storage, processing, and marketing of natural gas and natural gas liquids (NGLs). Its infrastructure features major pipeline systems such as Transco—one of the largest interstate pipelines serving the Eastern United States—and the Northwest Pipeline connecting key supply basins like Haynesville Shale and DJ Basin with demand centers.

The company’s revenue model depends heavily on long-term firm transportation contracts that provide stable fee-based income insulated from commodity price volatility; however, it also engages in commodity sales and derivatives introducing some earnings variability tied to market conditions [S1]. The midstream industry currently faces heightened regulatory scrutiny including FERC rate case proceedings and environmental compliance mandates impacting project approvals.

Growth Outlook & Capital Projects

Williams is advancing several major capital projects aimed at expanding transmission capacity:

- Gillis West Expansion: Expected Q2-2026 service adding approximately 115 Mdth/d capacity from Louisiana to Texas.

- Southeast Supply Enhancement: Anticipated as early as Q3-2027, expanding Transco’s footprint by roughly 1,597 Mdth/d across Southeastern states.

- Power Express Project: Targeted for Q3-2030 commissioning adding about 689 Mdth/d localized within Virginia.

- Pine Prairie Phase IV Expansion: Focused on storage enhancement aiming for Q4-2028 readiness with an additional working gas capacity near 10 Bcf.

- Additional reliability enhancements such as Overthrust Westbound Compression Expansion.

These large-scale projects are underpinned by firm transportation agreements securing revenue streams despite regulatory challenges [S2]. Williams retains flexibility to adjust capital spending responsive to economic conditions while investing in LNG export infrastructure expansion aligned with global gas demand trends [S10]. Recent acquisitions like Saber enhance gathering volumes supporting margin growth.

Financial Position & Capital Allocation

Williams maintains investment-grade credit ratings: BBB+ Stable from S&P; Baa2 Positive Moody’s; BBB Positive Fitch—an important factor for funding its multi-billion-dollar capex pipeline [S7][S8][S12]. As of December 31, 2025, total long-term debt stood at approximately $29.4 billion including subsidiaries’ obligations [S12]. Short-term liquidity comprises around $70 million cash plus access to revolving credit facilities totaling $3.75 billion net of commercial paper outstanding [S4][S5].

The current ratio is low (~0.53), reflecting elevated current liabilities mainly due within one year [F1]. Nevertheless, Williams expects operating cash flows sufficient for debt service and capital investments barring severe market disruptions.

Dividend policy remains shareholder-friendly with quarterly dividends increased modestly in early FY2025 from $0.475 to $0.50 per share [S10][F1]. There were no share repurchases during FY2025 or FY2024 as reinvestment into growth assets took precedence over buybacks.

Risk Factors

Key risks facing Williams include:

- Commodity price volatility affecting margins on commodity sales despite fee-based transport revenues [N6][S1].

- Elevated regulatory risk involving FERC oversight on rates and permitting delays combined with environmental compliance costs tied to climate regulations [S11][S14][S15].

- Customer concentration risk illustrated by major clients such as Duke Energy representing about 9% of Transco revenues; loss or renegotiation of contracts could materially affect cash flows [S6][S16].

- Credit risk exposure requiring vigilant counterparty assessments amid producer financial stress potentially impairing receivables recoverability.

- Execution risks on large capital programs given multi-year horizons extending beyond Q3-2030.

- Operational hazards including cybersecurity or physical disruption risks impacting safety or reputation.

Outlook & Considerations for Investors

Investors should monitor progress on key projects like Southeast Supply Enhancement and Power Express alongside regulatory developments impacting tariff structures or environmental compliance costs affecting project economics.

Cash flow adequacy relative to sustaining high capex levels will be critical for maintaining dividends without excessive leverage increases amid evolving credit markets.

Contract renewals or new awards will influence medium-term profitability while upstream production trends feeding Williams’ system directly affect throughput volumes underpinning gathering and processing segments.

Disclaimer

This analysis is based solely on publicly available SEC filings and reputable news sources cited herein; it does not constitute investment advice or recommendations regarding securities mentioned.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments