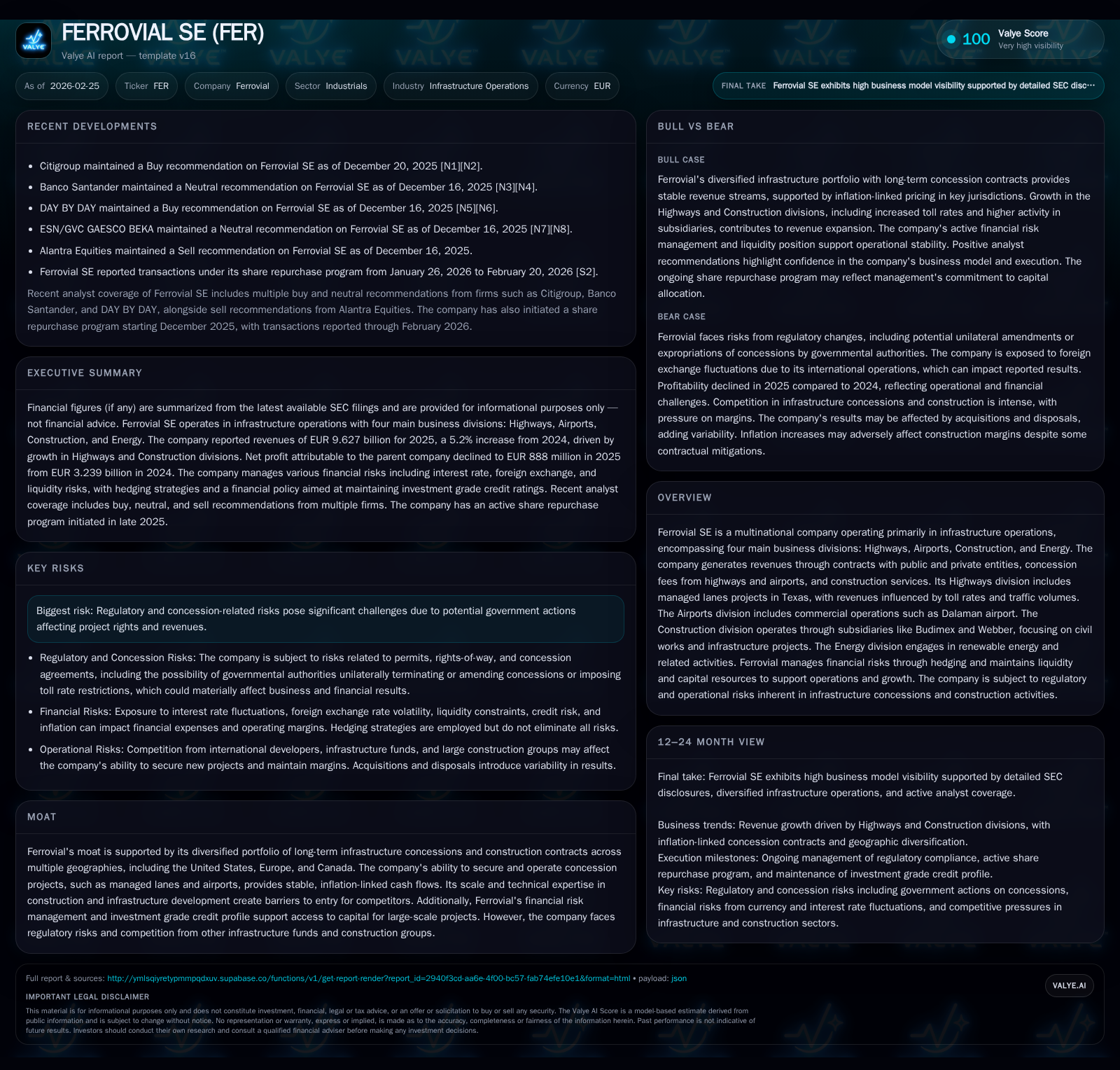

Ferrovial SE’s 2025 Growth Sustains on Infrastructure Concessions and Strategic Capital Allocation

Ferrovial leverages its diversified infrastructure portfolio and disciplined capital management amid regulatory challenges.

Ferrovial SE posted revenue growth of 5.2% in 2025, underpinned by stable concession cash flows in highways and airports alongside construction contributions. Net income declined substantially due to non-recurring impacts, but the company maintained strong operating cash flow and disciplined capital investment. Its competitive moat rests on long-term concessions across the U.S., Europe, and Canada, supported by technical expertise and financial prudence. Key risks include regulatory uncertainties impacting concession terms and toll rates.

Historical Performance: Revenue Growth Amid Earnings Volatility

Ferrovial SE recorded consolidated revenue of approximately €9.63 billion for the full year ending December 31, 2025, representing a year-over-year increase of about 5.2% from €9.15 billion in 2024 [F1]. This topline resilience principally derives from its core infrastructure operations segmented into Highways, Airports, Construction, and Energy businesses [S5]. The Highways division’s revenues are anchored by managed lanes projects in Texas (notably NTE, LBJ), where toll rates tied to inflation provide relatively steady income streams despite minor traffic fluctuations detailed in SEC exhibits [S13]. Airports add concession fees notably from Dalaman airport commercial activities, while the construction segment—operating through subsidiaries Budimex (Poland) and Webber (North America)—saw improved activity backing operational performance [S23].

Despite top-line gains, net income contracted sharply by approximately 67% from €3.49 billion in 2024 to €1.15 billion in 2025 [F1][S17]. The decline reflects the impact of non-recurring expenses and unfavorable financial results including derivatives losses and foreign exchange effects amid global volatility [S17]. Notwithstanding this earnings drop, Ferrovial sustained solid cash flow generation from operations (€1.93 billion in 2025 vs. €1.29 billion prior year), evidencing underlying business strength supported by the concession model's long-term visibility [F1][S22].

Historical performance (annual)

| FY | Rev ($bn) | Net ($bn) | Rev YoY | Net YoY |

|---|---|---|---|---|

| 2025 | 9.6 | 1.1 | +5.2% | -67.0% |

| 2024 | 9.1 | 3.5 |

Source: SEC companyfacts cache [F1].

Note: Some line items are omitted where multi-year comparability is limited in the structured SEC XBRL dataset; trend columns are shown only when comparable history exists.

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 15.0 |

| 2024 | 43.0 |

Source: SEC companyfacts cache [F1].

Future Growth Prospects: Infrastructure Concessions Drive Stability

Ferrovial’s growth outlook bases heavily on its diverse portfolio of concession assets across multiple jurisdictions primarily in the U.S., Canada, Europe, and Poland [S5][S6]. The firm enjoys a strategic moat through long-term contracts that typically link fee structures to inflation metrics offering a partial natural hedge against cost pressures; for example, certain contracts embed clauses mitigating margin compression risks related to inflation exposure especially in the construction segment [S4][S5].

In highways, ongoing expansion projects on Texas managed lanes such as North Tarrant Express (NTE) highlight growth catalysts supported by consistent traffic volume trends and inflation-linked toll increases [S13][S16]. The Airports business benefits from gradual recovery post-pandemic with airlines passing fuel cost increases partly onto customers—though demand elasticities pose downside risk to footfall and revenues [S13]. Renewable energy investments within the Energy division contribute incremental capex demands but align with sustainability goals fostering long-term value creation [S14][S24].

At the project level, Ferrovial continued advancing its ReadIT 2027 innovation strategy focused on digital transformation including Intelligent Transportation Systems and predictive geotechnical monitoring through partnerships like MIT collaboration enhancing operational resilience amid climate challenges [S1][S24]. This forward-looking research underpins competitive differentiation beyond raw asset ownership.

Forecasts / Milestones / Expectations: Watch for Concession Traffic & Regulatory Developments

While explicit financial guidance is not stated in the filings reviewed, key milestones revolve around ramping up traffic volumes on new managed lanes assets and successful operation of airport concessions amid travel demand normalization [N1][S27]. Additionally, upcoming maturity of corporate bonds (notably a €780 million issue maturing May 2026) poses refinancing considerations though mitigated by ample liquidity and revolving credit facilities extending to early 2030s [S11][S12].

Investors should monitor: (i) traffic trends on key highways franchises in Texas including pricing flexibility under concession agreements; (ii) regulatory decisions affecting toll setting or contract terms potentially impacting cash flows; (iii) progress deploying technology-driven efficiency gains aligned with ReadIT initiatives; and (iv) capital deployment efficiency balancing acquisitions against divestment proceeds notably from recent sales of stakes in Heathrow Airport Holdings and AGS airports [N1][S23].

Returns / Capital Allocation: Prudent Management Amid Market Volatility

Ferrovial’s return profile for FY 2025 shows an approximate return on equity (ROE) near 15%, down from exceptionally high prior year levels due to lowered net income but still reflective of efficient equity utilization within a capital-intensive infrastructure model [F1]. Cash flow analysis reveals operating cash flow at roughly €1.93 billion contrasted with capex outflows circa €0.89 billion invested across divisions including significant stakes acquired incrementally (e.g., an additional 5% stake in highway operator 407 ETR for over €1.27 billion partially offset by divestment proceeds totaling about €1.15 billion) demonstrating active portfolio pruning and rebalancing for value optimization [S23].

Liquidity remains robust with cash equivalents exceeding €4.2 billion at year-end providing substantial buffer ahead of upcoming debt maturities totaling several hundred million euros annually through late decade mainly related to project-level borrowings which are ring-fenced without recourse beyond project assets ensuring group-level risk containment [F1][S7][S19]. Corporate bonds totaling roughly €2.65 billion carry low coupons reflecting sound credit standing confirmed by BBB rating grades with stable outlooks from both Standard & Poor’s and Fitch agencies highlighting market confidence in financial management discipline [S20].

The dividend policy emphasizes steady shareholder returns balanced against reinvestment into innovation-driven growth opportunities underpinning sustainability commitments as articulated through ReadIT pillars spanning Innovation Levers, Focus Areas, and Fundamentals encompassing cybersecurity compliance alongside environmental considerations central to newer infrastructure design standards emphasizing climate resilience [S24].

Industry Context Commentary

The infrastructure sector remains intensely competitive with Ferrovial facing rivals ranging from global infrastructure funds backed by pension monies seeking inflation-linked yield profiles to large multinational construction groups aiming to vertically integrate project equity ownership with execution capabilities [S6]. Success hinges on financing capacity to bid competitively for concessions anchored on realistic hurdle rates, technical operational excellence particularly leveraging data analytics for dynamic toll pricing optimization, alongside mitigating geopolitical/regulatory intervention risks that can abruptly alter contract economics through expropriations or rate caps commonly cited challenges within regulated infrastructure domains.

Summary

Ferrovial SE’s fiscal year 2025 exhibited solid revenue expansion driven by its diverse infrastructure portfolio despite significant earnings pressure stemming mainly from non-recurring factors impacting profitability metrics temporarily. Maintaining ample liquidity reserves paired with disciplined capital allocation enabled the company to invest strategically while sustaining operational robustness across highways, airports, construction projects, and energy sectors worldwide.

Long-term prospects remain linked closely to inflation-indexed concession contracts providing predictable cash flows buffered against some macroeconomic volatility while ongoing investments into technology infrastructure aim at fortifying competitiveness via digital transformation initiatives.

Regulatory vigilance will remain critical given inherent operational exposure across multiple jurisdictions susceptible to government interventions affecting concession rights or toll frameworks.

This report is intended solely for informational purposes reflecting available company disclosures as of early 2026 without conveying investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments