Pursuit Attractions & Hospitality’s Financial Realignment and Growth Prospects Post-Divestiture

Following the sale of its Flyover flying theater business, Pursuit refines its capital structure and navigates evolving operational dynamics to stabilize and pursue growth.

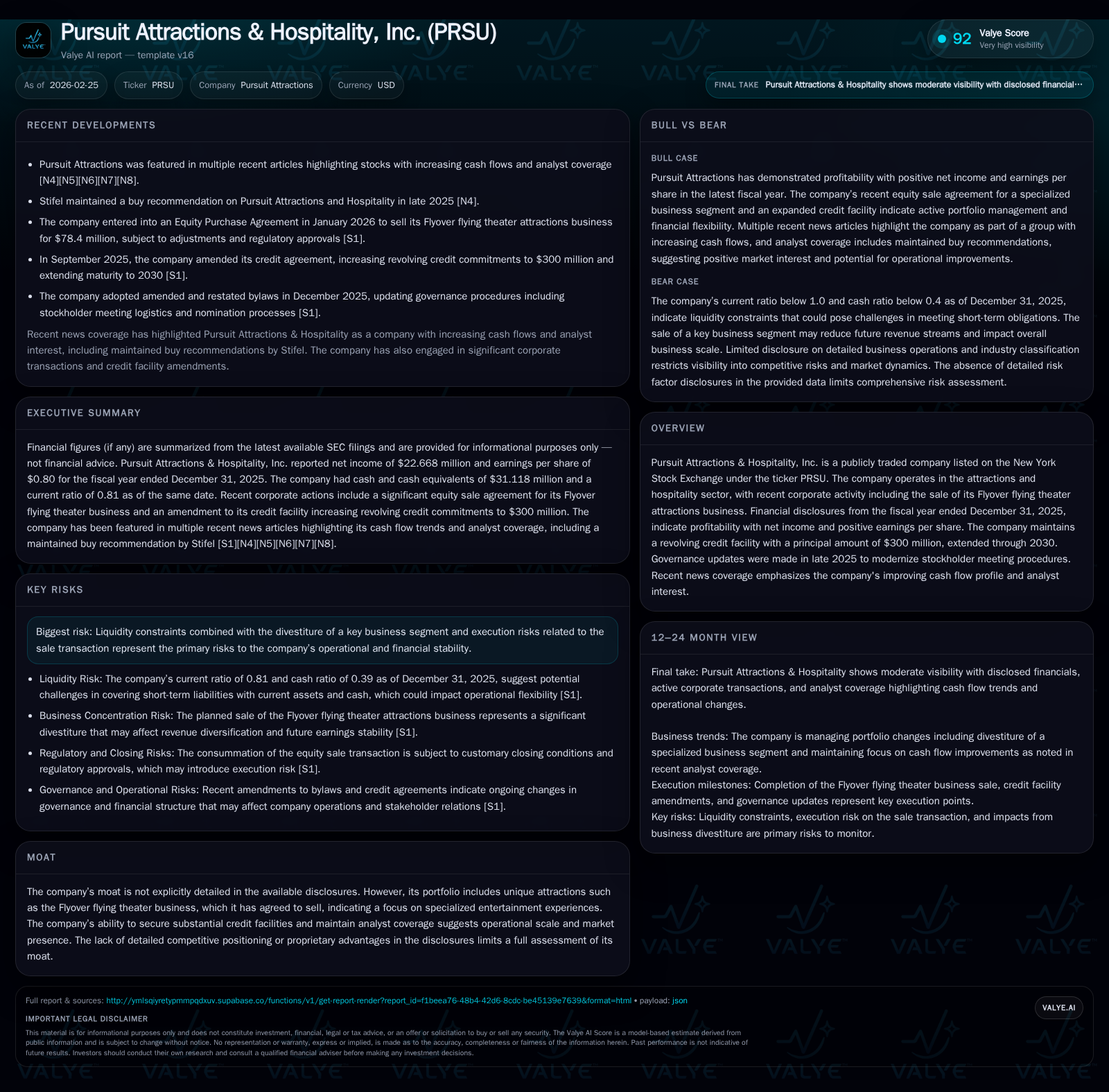

Pursuit Attractions & Hospitality, Inc. has recently completed a significant corporate transition by agreeing to sell its Flyover flying theater attractions, reshaping its strategic focus. The company’s fiscal 2025 results show sustained profitability amid this divestiture, bolstered by an expanded revolving credit facility extending through 2030 that enhances liquidity. While operating cash flow is improving notably, the company faces execution risk tied to the sale transaction closure alongside liquidity constraints reflected in a sub-1 current ratio. Pursuit's capital allocation remains conservative, with modest buybacks resuming and no dividends since 2022. Market watchers will track the closing of the Flyover deal and subsequent earnings releases as key near-term catalysts.

Evolution of Revenue and Profitability: Historical Performance Overview

Pursuit Attractions & Hospitality’s financial profile over recent years reveals a trajectory marked by noticeable volatility but trending toward operational stabilization. Fiscal year 2025 witnessed revenue reaching approximately $1.064 billion USD, marking a solid increase of about 9.5% compared with the prior year [F1]. However, net income contracted sharply by nearly 94%, down to $22.7 million USD in FY2025 from a robust $368.5 million USD in FY2024 [F1]. This divergence suggests one-time gains or asset-related accounting effects influencing previous year results and points toward mixed underlying profitability despite top-line expansion.

Operating income showed a rebound pattern culminating near $92.5 million USD as of Q3 2024, indicating progress from prior losses including the significant negative operating income recorded in 2020 [F1]. Notably, the company's current ratio stood at a lean 0.81 as of end-2025—a liquidity concern flag given short-term liabilities exceeding current assets slightly—highlighting ongoing working capital management challenges within this capital-intensive sector.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 23 | 75 | -93.8% | ||

| 2024 | 369 | 56 | +2201.0% | ||

| 2023 | 16 | 105 | 108 | 76 | -31.0% |

| 2022 | 23 | 73 | 69 | 67 |

Source: SEC companyfacts cache [F1].

Note: Some line items are omitted where multi-year comparability is limited in the structured SEC XBRL dataset; trend columns are shown only when comparable history exists.

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 10 | 3.9 | |

| 2024 | 70.1 | ||

| 2023 | 29 | 36.9 | |

| 2022 | 0 | 6 | 159.8 |

Source: SEC companyfacts cache [F1]. | Note: Latest full-year OpInc not available beyond Q3'24

Strategic Divestiture of Flyover Flying Theater: Implications and Context

In January 2026, Pursuit entered into an agreement to divest its Flyover flying theater attractions business for approximately $78.4 million USD in cash consideration subject to typical post-closing purchase price adjustments [S19]. This sale marks a deliberate pivot away from specialized immersive entertainment assets towards a streamlined core portfolio emphasizing hospitality and attractions segments with presumably steadier cash generation profiles.

The transaction includes customary representations, warranties, and covenants with protections such as a $10 million termination fee payable should the buyer fail to consummate the purchase after Pursuit’s readiness is confirmed [S14]. Notably, representation warranties insurance secured by the purchaser adds an extra layer of risk mitigation concerning indemnity exposures post-close.

This divestiture presents both an opportunity for Pursuit to enhance liquidity and de-risk portfolio complexity but also introduces execution risk dependent on timely regulatory approvals and buyer performance during closing phases anticipated no later than May 21, 2026 [S19]. Failure or delay here could destabilize current financial projections.

Capital Structure Enhancements: Revolving Credit Facility and Debt Profile

Pursuit successfully amended its credit arrangement in late September 2025 to boost revolving commitments by $100 million USD, lifting the total revolving credit line to $300 million USD with maturity extended through September 2030 [S9][S15]. This refinancing offered multiple enhancements including removal of an additional credit spread margin on borrowings tied to SOFR rates, optimizing interest expense costs.

The amendment also incorporated Inversiones Turísticas Arenal S.A., along with affiliates, as co-borrowers and guarantors expanding collateral coverage which improves covenant flexibility under the loan agreement [S9]. Such structuring maneuvers bolster liquidity headroom enabling tactical funding for capital expenditures or working capital needs typical in hospitality operations where seasonality often requires reserve buffers.

Given these terms, Pursuit’s long-dated revolving facility positions it well against near-term maturities while maintaining financing agility tailored for asset-heavy operational requirements characteristic of attraction management platforms.

Liquidity Trends and Cash Flow Dynamics Amid Operational Changes

Operational cash flow generation gained notable momentum with FY2023 net CFO at approximately $105 million USD growing from $73 million USD in FY2022—a rate acceleration of nearly 43% year-over-year—with FY2025 continuing this trend though exact latest CFO figure is not stated explicitly but inferred positive from free cash flow calculation [F1][N6].

Capital expenditure outlays rose concurrently by approximately one-third YOY in FY2025 totaling about $75 million USD reflecting ongoing investment into maintained or new attraction facilities critical for experience-based revenue streams [F1]. Despite increased capex absorption, free cash flow remained positive near $29.7 million USD suggesting disciplined spending amidst growth initiatives.

Analyst commentary during early 2026 underscores growing market confidence around Pursuit's improving liquidity framework which is crucial given hospitality subsector cyclicality demanding ready access to both liquid reserves and revolving sources under rapid consumer traffic shifts triggered by economic cycles or travel trends [N6][N7].

Future Growth Outlook: Opportunities, Constraints, and Execution Risks

Absent explicit forward guidance from Pursuit’s disclosures beyond standard SEC filings, future growth prospects must be extrapolated cautiously based on disclosed strategic moves including divestiture completion timelines and announced operational updates [N6][S14]. Potential growth drivers include redeployment of sale proceeds toward higher-margin core segments alongside operating efficiencies fostered by a simplified portfolio.

Constraints manifest primarily through liquidity pressures underscored by a sub-1 current ratio (0.81), reflecting tight working capital positioning paired with execution risk tied directly to successful closure of the Flyover business sale scheduled before mid-2026 closing deadline [F1][S14][S19]. Regulatory approvals could impose delays adding operational uncertainty.

Competitive pressures remain implicit risks given lack of detailed moat elements in reported filings; reliance on scale benefits evidenced via revolving facility size partly offsets this but underscores necessity for continued innovation or differentiation within experiential offerings across diversified markets.

Financial Returns and Capital Allocation Policy: Dividend and Buyback Trajectory

Pursuit has maintained a conservative capital return policy in recent years characterized by suspension of dividends since fiscal year-end 2022 and limited buyback activity resumed only modestly in FY2025 with repurchases summing approximately $10 million USD—contrasting with zero buybacks during preceding years except sporadic minor programs in early pandemic periods [F1][S25].

Such discipline aligns with reinvestment priorities typical for hospitality operators navigating portfolio transformation phases requiring retained earnings preservation bolstered through credit facility access rather than distribution increases.

Equity growth over the past few years—from $14.5 million USD equity base in FY2022 to nearly $582 million USD reported end-2025—reflects accumulated retained earnings combined with possible balance sheet adjustments related to transactional restructuring although placeholding exact contributions is speculative without further details [F1]. Current ROE remains conservative near four percent indicative of asset-heavy industry norms balancing stable returns against capital intensity.

Legal, Regulatory, and Risk Factors in Transition

Risk disclosure documents underscore several notable corporate governance updates implemented late in calendar year 2025 designed to modernize stockholder meeting processes incorporating remote communication capabilities as well as nomination procedural refinements compliant with prevailing SEC proxy rules—the Universal Proxy Rules—increasing procedural robustness under institutional investor scrutiny frameworks [S25].

Principal lingering risks focus heavily on liquidity constraints combined with transaction execution uncertainties related to the Flyover divestiture process including potential regulatory hurdles or counterparty default scenarios subject to contractual remedies such as termination fees outlined earlier [S4][S6][S14].

Legal contingencies spanning standard litigation claims are detailed per Note 18 disclosures cross-referenced multiple times suggesting ongoing monitoring without material adverse effect currently anticipated but warranting vigilance from governance perspectives ahead of asset ownership changes [S4].

Key Metrics to Monitor: Market Expectations and Upcoming Milestones

Investors should pay close attention to markers including official closing dates for the Flyover sale expected no later than May 21, 2026; any announcements regarding regulatory approval status; quarterly earnings reports outlining post-divestiture operational performance; updated guidance should it be issued; plus ongoing liquidity ratio movements reflecting working capital management efficacy [N6][N7][S19].

Analyst commentary particularly from early February conveys optimistic views centered on escalating cash flow trajectories juxtaposed against cautious appraisal due to pending structural changes signifying relevance for valuation calibration going forward within hospitality-focused asset managers’ peer context.

Disclaimer: This report is intended solely for informational purposes based on available public filings and news sources as cited herein. It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments