UWM Holdings’ Revenue Surge Masks Cash Flow Stress and Wholesale Channel Concentration Risks

Despite robust top-line growth, UWM faces operational cash flow challenges and market sensitivity inherent in its exclusive wholesale mortgage lending model.

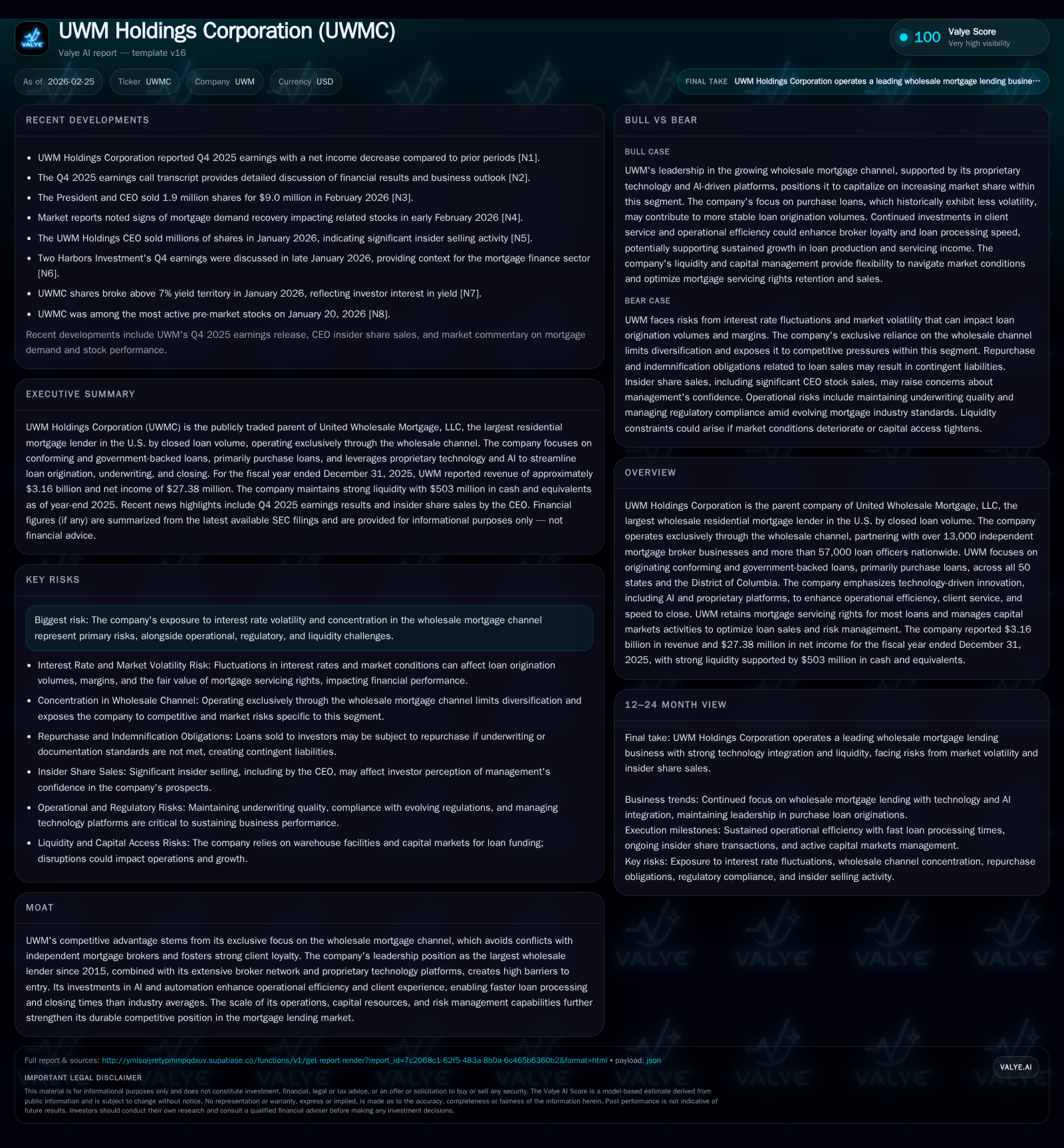

UWM Holdings Corporation, the largest wholesale residential mortgage lender by volume in the U.S., demonstrated a strong revenue increase of approximately 46% in 2025 compared to 2024, reaching $3.16 billion. This growth stems from its exclusive focus on the wholesale channel and investments in proprietary technology tailored for Independent Mortgage Brokers. However, operating cash flow remains deeply negative, with a -$2.65 billion outflow in 2025, underscoring liquidity strain despite a modest net income of $27.4 million. The company's capital structure is supported by diverse warehouse and senior debt facilities, maintaining covenant compliance but facing refinancing timelines. Market sensitivities, particularly interest rate volatility affecting mortgage servicing rights (MSRs) valuation and demand fluctuations in the purchase loan segment, present ongoing risks. Insider share sales by management and litigation exposures add to operational uncertainties.

Company Overview and Market Position

UWM Holdings Corp (ticker: UWMC) is the publicly traded parent of United Wholesale Mortgage, LLC — currently the largest wholesale residential mortgage lender in the U.S. by closed loan volume [S1]. Since its founding in 1986 and IPO via SPAC in early 2021, the company has concentrated exclusively on the wholesale mortgage channel, partnering with over 13,000 independent mortgage brokers and more than 57,000 loan officers nationwide [S1]. This singular focus avoids direct borrower competition common in retail lending, fostering strong broker alignment and loyalty which constitute key competitive moat elements [S1].

The company's product suite centers primarily around conforming loans backed by government-sponsored enterprises like Fannie Mae and Freddie Mac (approximately 90% of loans originated in 2025), along with FHA, USDA, VA government loans and non-agency jumbo products under similar underwriting standards [S1][S2]. Purchase loans dominate originations versus refinancing given preference for volume stability amid interest rate cycles [S1].

Technological innovation — including proprietary AI-driven platforms — is marketed as a differentiator to accelerate loan processing times and enhance broker experience [S1]. Retaining mortgage servicing rights (MSRs) for most loans enhances recurring revenue potential despite exposure to interest rate-driven valuation swings [S1].

Historical Performance: Growth Drivers and Financial Summary

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($bn) | Capex ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 3.2 | 27 | -2.6 | 74 | +46.1% | +90.1% |

| 2024 | 2.2 | 14 | -6.2 | 39 | +65.0% | +208.9% |

| 2023 | 1.3 | -13 | 0.2 | 26 | -44.7% | -131.7% |

| 2022 | 2.4 | 42 | 8.3 | 27 |

Source: SEC companyfacts cache [F1].

Note: Some line items are omitted where multi-year comparability is limited in the structured SEC XBRL dataset; trend columns are shown only when comparable history exists.

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks | FCF ($bn) |

|---|---|---|---|

| 2025 | 79 | -2.7 | |

| 2024 | 40 | -6.3 | |

| 2023 | 37 | 0 | 0.1 |

| 2022 | 37 | 0 | 8.2 |

Source: SEC companyfacts cache [F1].

These figures reflect a notably volatile cash flow profile aligned with mortgage origination cycles and capital deployment requirements for warehouse funding lines [F1]. Revenue saw compounded strong double-digit growth punctuated by a dip in early periods likely reflecting broader macroeconomic headwinds but recovering strongly into full year 2025 (+46% YoY). Positive net income returned after losses in prior periods but remains restrained relative to revenue scale.

Negative operating cash flows underscore significant working capital deployed to fund loans before secondary market sale or securitization [F1][S4], while capital expenditures nearly doubled year-over-year as investments continue into technological infrastructure and platform enhancements [F1]. Dividend payments grew steadily reflecting confidence in distributable cash generation despite negative free cash flow (CFO less Capex approx. -$2.72B) [F1]. The absence of buybacks since FY2022 signals redeployment of capital towards liquidity preservation or operational priorities.

Future Growth Prospects: Opportunities and Limitations

UWM aims to leverage its entrenched wholesale channel network and technology leadership to capture increased purchase mortgage volume across the U.S., stated as covering all states plus DC [S1]. Their wholesale-exclusive model mitigates direct conflicts with brokers' borrower relationships enhancing client retention amid intensifying market competition [S1]. Investment in AI-powered interfaces promises faster closings—an industry-wide bottleneck—and improved broker productivity.

Growth near term will correlate strongly with residential real estate market dynamics: home buying sentiment driven by economic conditions like wage trends, inflation impact on purchasing power, unemployment rates, consumer confidence as well as mortgage interest rates influence borrowing activity extensively [S20]. Purchase loans being less volatile than refinance originations soften cyclical swings but do not eliminate systemic risk.

On the risk side, UWM's concentration solely in the wholesale channel could dampen diversification benefits especially if regulatory changes or disruption hit this distribution avenue disproportionately [S20][N1]. Moreover, MSR portfolio values exhibit sensitivity to rising rates affecting servicing income streams—a key profitability lever—as these valuations fluctuate with prepayment speeds and discount rate assumptions embedded within forecasting models [S1][S20].

Monitoring management’s tactical decisions regarding opportunistic MSR sales versus retention will be critical to assessing risk-return tradeoffs ahead.

Forecasts & Key Milestones

The company has not provided explicit forward guidance for the upcoming fiscal periods within its latest filings or earnings calls observed [N2][S1]. Analysts should watch closely:

- Loan origination volume trends through quarterly updates juxtaposed against secondary market pricing environments;

- Mortgage servicing rights valuation disclosures given their marked impact on earnings volatility;

- Any recalibration of dividend policy or initiation of share buybacks signaling confidence levels;

- Debt maturity schedules notably upcoming notes due between now and early next decade along with associated refinancing plans;

- Regulatory developments affecting wholesale lending channel operations or broker compensation frameworks.

A recently declared Q4 dividend of $0.10 per Class A share payable April signals continuity of shareholder returns despite operational challenges noted [N3][S3].

Returns & Capital Allocation Patterns

While specific return on equity metrics are not uniformly disclosed given GAAP complexities including loan sale gains/losses and MSR fair value impacts [F1], approximate ROE calculated using latest net income ($27.38M) over reported equity (~$5M in earlier years but unlisted recent figure) suggests extremely high leverage should be interpreted cautiously owing to accounting realities.

Capital allocation focuses heavily on sustaining warehouse debt-backed loan origination volumes supported by multiple committed credit lines totaling billions with strict covenants that have been complied with as of latest filings [S5][S7][S9]. Senior unsecured notes issued range from maturities due in next five years up through early next decade maintaining staggered amortization profiles [S6][S11][S19].

Dividend outlays growing steadily reflect prioritizing shareholder distributions even amid negative operational cash flows potentially funded through debt or equity issuance if necessary [F1][S14]. Absence of buybacks post-2022 indicates capital conserved possibly due to uncertain macroeconomic conditions or liquidity preservation strategies.

Regular insider selling—particularly CEO Mat Ishbia's material stock disposals exceeding millions of shares—could imply varying interpretations around insider confidence or personal diversification motives warranting further corporate governance scrutiny [N4][N5][N6][N7].

Industry Context & Competitive Positioning (Analysis)

Wholesale mortgage lending is distinguished from retail models by reliance on independent brokers who connect borrowers with lenders. UWM's embrace of broker exclusivity supports strong network effects vital for distribution scale.

Trade publications highlight that industry incumbents face cost pressures from prolonged elevated interest rates suppressing refinance windows while homebuyer affordability constrains purchase activity broadly; UWM’s emphasis on purchases over refinancing may shield it somewhat from cyclicality typical elsewhere.

Proprietary platforms automating underwriting steps integrated with AI denote best practices shaping competitiveness; however larger players also invest similarly making pace of innovation a continuous imperative.

Overall loan origination profitability is compressed when volume declines coincide with rising funding costs or heightened risk reserves—highlighting the balancing act required across underwriting prudence versus aggressive growth ambitions.

Legal and Regulatory Environment Risks

UWM operates under intense regulatory scrutiny involving consumer protection laws at multiple jurisdictional levels leading to frequent audits or legal challenges typical for large-scale mortgage lenders [S20][S21]. Notably pending class action litigation accuses alleged improper steering incentivization within broker networks though management has obtained dismissals of amended complaints so far; this suits ongoing monitoring given reputational stakes and potential financial implications [S20].

Labor-related class action lawsuits have trended upward consistent with increased employment law litigation nationwide suggesting exposure beyond core mortgage originations merits careful oversight [S21].

Compliance efforts must navigate dynamic federal/state frameworks especially related to borrower disclosures and fair lending regulations maintaining operational risk at forefront.

Final Observations

UWM Holdings presents a compelling case study blending dominant wholesale lending scale built on proprietary technology with inherent exposure to cyclical real estate markets amplified through exclusive reliance on broker channels. Solid revenue escalation masks acute cash flow pressures driven by capital-intensive loan funding mechanisms offsetting net income gains. Liquidity management anchored by layered warehouse credit facilities alongside senior debt instruments underpins ongoing operations although upcoming refinancing needs require strategic foresight. Ongoing legal matters coupled with insider selling activity underscore areas requiring stakeholder vigilance while technology investment commitments are essential for sustaining competitive advantages. Future earnings trajectories will pivot materially on home purchase demand resilience amidst macroeconomic uncertainty plus nuanced MSR valuation sensitivities—a vital bellwether for this sector leader’s financial health.

This report is strictly informational based on disclosed company filings and publicly available sources as of February 25, 2026. It does not constitute investment advice or recommendations. Users should consider consulting professional advisors before making financial decisions involving UWM Holdings Corp or comparable entities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments