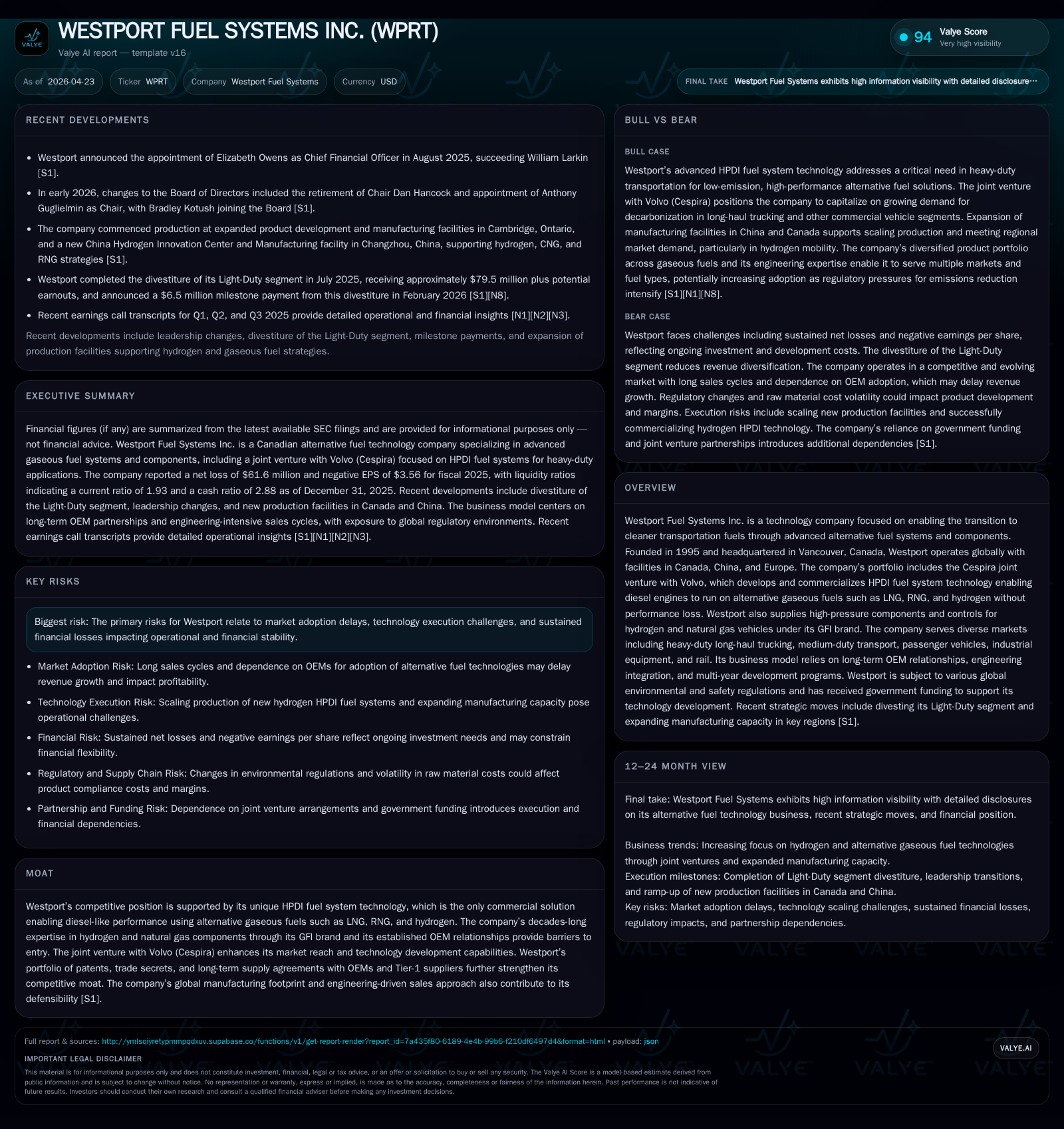

Westport Fuel Systems Narrows Losses as HPDI Technology Gains Ground

Westport's latest quarterly filing highlights operational transitions and growing traction of its HPDI technology through Cespira amid hydrogen market challenges.

In its April 2026 quarterly update, Westport Fuel Systems reported a notable decline in revenue reflecting the conclusion of its transitional manufacturing services with the Cespira joint venture and a slowdown in hydrogen-related sales. Despite this near-term softness, the increase in Cespira’s revenues by 80% in 2025 underscores growing OEM adoption of Westport’s proprietary HPDI fuel systems, critical for delivering diesel-level performance on alternative gaseous fuels. Operational restructuring involving the relocation of manufacturing bases to Canada and China is expected to enhance capacity and efficiency heading into 2026. However, market adoption bottlenecks—especially related to hydrogen infrastructure—and ongoing liquidity concerns remain key constraints to be monitored.

Latest Quarterly Update Highlights Operational Transition

Westport Fuel Systems’ most recent Form 6-K filing dated April 21, 2026 ([S2]) reveals a pronounced operational transition that defined its late-2025 performance. Total revenue sharply contracted by 74% year-over-year for Q4 2025 to $1.88 million from $7.28 million as the Heavy-Duty OEM segment revenue plunged to zero following the end of a transitional services agreement (TSA) with the Cespira joint venture in June 2025 ([S1], [S2], [S3]). This TSA had previously underpinned significant contract manufacturing revenue but ceased as Cespira established its own manufacturing footprint.

The High-Pressure Controls segment showed some stability with $1.88 million in Q4 sales—a modest increase over Q4 2024 but still down from prior years due mainly to continued drag from the early-2025 slowdown in hydrogen infrastructure development ([S1]). The segment was also disrupted by relocation of its manufacturing capacity from Italy to new plants in Canada and China in Q3-Q4 2025. This operational shakeout caused temporary shutdowns affecting shipment volumes, though production restarted late in Q4 and output efficiency improvement is anticipated through 2026 ([S1]).

This creates a near-term throughput lull but positions Westport’s core High-Pressure Controls platform for more scalable growth given its expanded global footprint. Meanwhile, Cespira—the joint venture where Westport holds a majority stake—reported robust revenue growth of $77.4 million in FY2025 (+80%), underlining advancing commercialization of the HPDI fuel system technology primarily targeting heavy-duty long-haul trucking ([S1], Valye Report Excerpt). However, Cespira remains unprofitable as it incurs inventory provisions and onerous contract losses while investing heavily in product launches and engineering services ([S15]).

Westport’s Business Model: High-Pressure Alternative Fuel Systems and OEM Partnerships

Westport’s commercial model revolves around the design, development, and manufacture of advanced high-pressure direct injection (HPDI) fuel systems enabling diesel engine platforms to run on cleaner gaseous fuels—including LNG (liquefied natural gas), RNG (renewable natural gas), and hydrogen—without sacrificing diesel-equivalent performance metrics such as torque or efficiency ([S19]). This offering is uniquely commercialized through the Cespira joint venture with Volvo Group that consolidates scale engineering capability and global OEM sales reach.

In parallel, Westport's High-Pressure Controls segment supplies engineered high-pressure components including valves, regulators, electronic control units (ECUs), filters, and sensors under its GFI brand. These products serve OEMs across diverse markets including passenger vehicles to industrial equipment leveraging gaseous fuels such as hydrogen or methane derivatives ([S19], [S18]).

Westport maintains deep collaborative relationships with Tier-1 suppliers and major OEMs enabling lengthy multi-year engineering integration programs characterized by high switching costs once production validation phases are cleared—offering durability to its competitive advantages (, [S19]). Its portfolio of patents around HPDI combustion processes combined with trade secrets in pressure management underpin an intellectual property moat that deters replication absent substantial technical investment ([S11]).

Competitive Position and Industry Structure

Within the broader clean transportation ecosystem—where battery-electric vehicles (BEVs), fuel cell electric vehicles (FCEVs), cleaner diesel engines, hybrids, and biofuels vie for adoption—Westport occupies an exclusive niche by offering HPDI systems that allow existing diesel platforms to convert seamlessly to alternative gaseous fuels without performance compromise ([S20]). This niche is critical notably for heavy-duty trucking applications where energy density and range remain limiting factors for BEVs.

However, competition is multifaceted: incumbent OEMs continue investing heavily in electrification; Chinese manufacturers exert pricing pressure particularly on commoditized component lines; fuel cell players push hydrogen-based solutions requiring different hardware entirely; meanwhile regulatory regimes evolve unevenly across regions influencing adoption rates ([S5], ).

Westport navigates these industry dynamics leveraging a differentiated value proposition emphasizing fuel flexibility (LNG/RNG/hydrogen compatibility) integrated within existing vehicle powertrains—a compelling proposition against dedicated fuel cell stacks or pure battery replacements within certain segments. Yet penetration remains constrained by infrastructure gaps especially for hydrogen refueling networks ([S10], [S11]).

Growth Drivers: Commercialization of HPDI Technology through Cespira

The formation of Cespira JV with Volvo represents Westport’s pivotal growth engine. By transferring heavy-duty HPDI business into this entity along with key manufacturing assets, engineering teams, and customer contracts, Westport aims to harness scale economies critical for winning large OEM program awards globally ([S1], ).

Cespira’s FY2025 revenues surged +80% driven primarily by volume expansion with initial OEM customers deploying HPDI fuel systems aiming at regulatory compliance and operational cost savings afforded by gaseous fuels ([S15]). Engineering service revenues grew alongside product sales reflecting ongoing system integration efforts tied to upcoming European emissions standards.

The roadmap includes further R&D enhancements progressing multi-fuel capability expansions while leveraging Volvo’s industry stature for wider market penetration especially within long-haul trucking—a sector aggressively transitioning due to tightened CO2 norms combined with rising diesel fuel costs ([N1], [S19]). Capital contributions planned for Cespira are decreasing markedly ($11 million expected from Westport in 2026 vs $21.7 million in 2025), implying improved cash flow dynamics at the JV level ([S23]).

Constraints: Market Adoption Challenges and Hydrogen Infrastructure Dynamics

While Westport’s technologies are technologically defensible and strategically aligned with decarbonization imperatives, uptake remains pressured due to multiple external factors.

Firstly, the hydrogen market slowdown evident since early 2025 impacted High-Pressure Controls sales as slower infrastructure buildout delays volume expansion for hydrogen ICEs and fuel-cell vehicles relying on these components ([S1], [N3]). The complexity of shifting bulky liquid/pressurized gas logistics infrastructure limits rapid scalability relative to liquid fuels like diesel.

Secondly, economic incentives influencing total cost of ownership pose uncertainty. Natural gas price volatility vis-à-vis diesel alters fleet owner calculus toward conversion projects amid uneven government subsidies globally ([S10], [S22]). Public policy shifts can either accelerate or stall adoption unpredictably.

Thirdly, intensifying competition from BEVs increasingly favored for medium-duty segments combined with emergent next-generation biofuels introduces risk that some market segments may bypass gaseous fuel alternatives entirely. Lastly, supply chain sensitivities including raw material costs for specialized components potentially compress margins or cause procurement delays ([S14], [S17]).

Looking Ahead: Key Milestones and Execution Risks

Critical upcoming inflection points include:

- Scaling production volumes at newly commissioned Canadian and Chinese facilities throughout 2026 aimed at fulfilling backlogged orders post-relocation disruptions ([S2], [S3]).

- Continued ramp-up of Cespira OEM programs beyond first customers capturing share within long-haul truck market segments sympathetic to LNG/Hydrogen powertrains.

- Monitoring capital raise outcomes crucial for alleviating substantial doubt about going concern status given ongoing operating losses despite narrowing trends ([S1], [S6], [S22]).

- Vigilance regarding competitive technology developments potentially threatening HPDI relevance.

Management emphasizes prudence around liquidity; ongoing negotiations seek equity or debt funding yet market conditions inject execution risk that could hamper growth investments or require strategic pivots if financing fails ([S1], [N3]).

Financial Profile: Trends, Liquidity, and Capital Structure

Fiscal year ended December 31, 2025 data illustrates fundamental operating pressures beneath strategic gains:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -62 | -14 | 3 | -182.2% | |

| 2024 | -22 | 7 | -25 | 17 | +56.1% |

| 2023 | -50 | -13 | -46 | 16 | -52.1% |

| 2022 | -33 | -32 | -50 | 14 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -89.6 | |

| 2024 | -10 | -15.9 |

| 2023 | -29 | -31.0 |

| 2022 | -46 | -16.0 |

Source: SEC companyfacts cache [F1].

Net losses widened YoY partially due to increased equity losses from investments like Cespira despite reductions in operating expenses.[S1][F1] Capital expenditures dropped steeply by 84% YoY reflecting completion of relocation capex projects.[F1] Free cash flow turned positive ($4.49M) supported by asset divestitures but operating cash use increased over prior year.[F1] Debt remains modest relative to cash reserves but insufficient liquidity forecasted beyond one year absent successful capital raises flagged as material uncertainty under accounting rules.[S6][S22]

Overall financial posture reflects typical deep investment phase companies balancing strategic restructuring against persistent top-line contraction exacerbated by emerging market risks.

This analysis relies exclusively on company-submitted SEC filings combined with secondary earnings transcripts covering April 2026 updates without extrapolation beyond verified disclosures. It aims at presenting an operational perspective validating strategic positioning amid current headwinds rather than predicting future stock behavior or investment outcomes.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments