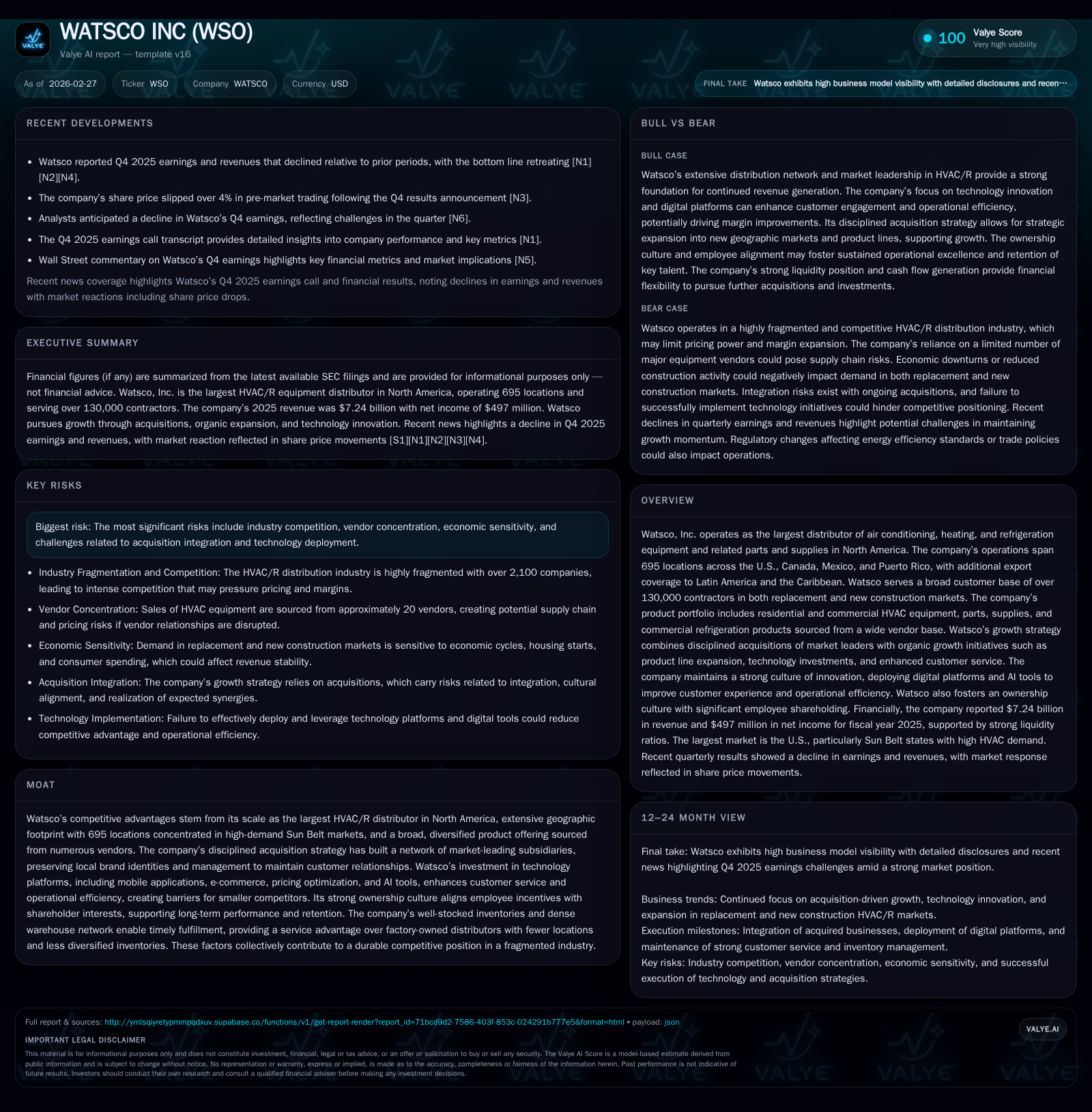

Watsco’s Growth Moderation Highlights Supply Risks and Capital Allocation Discipline

After decades of robust expansion, Watsco faces top-line pressures in 2025 amid supplier concentration and industry competition.

Watsco Inc remains the dominant HVAC/R distributor in North America with a diversified footprint of 695 locations serving over 130,000 contractors. The company’s historical revenue growth has been driven by disciplined acquisitions, organic expansion, and technology investments. However, fiscal 2025 saw a 5% revenue decline with operating income down almost 8%, reflecting headwinds such as supplier concentration risks particularly with Carrier and Rheem, and economic sensitivity. Watsco’s capital allocation continues to favor dividends and opportunistic buybacks supported by solid free cash flow generation, but challenges in integrating acquisitions and evolving technology platforms will test future growth prospects.

Overview

Watsco Inc is the largest distributor of HVAC (heating, ventilation, air conditioning) and refrigeration equipment plus related parts and supplies across North America. Its extensive network spans 695 locations distributed mainly across key growth regions in the U.S., Canada, Mexico, and Puerto Rico with coverage extending into Latin America and the Caribbean. Serving over 130,000 contractors engaged both in replacement markets—which demand rapid availability—and new construction projects, Watsco boasts a dominant footprint anchored in high-demand Sun Belt states such as Florida (102 stores) and Texas (89 stores) that benefit from robust population growth and energy-efficiency incentive programs [S1][S4][S5].

Founded in Florida in 1956, Watsco's revenues have expanded from a modest $64 million in 1989 to over $7.2 billion by year-end 2025 [F1][S25]. This growth has stemmed from a dual-pronged strategy combining targeted acquisitions of well-established regional distributors along with organic expansion through broadening product lines and technology investments that enhance customer service capabilities.

Historical Performance

The past several years showcase Watsco's capacity for steady scaling but also reveal emerging pressures. Its revenues peaked at $7.6 billion in FY2024 before retreating approximately 5% to $7.24 billion for FY2025 [F1]. This top-line contraction is mirrored by softer operating income that declined nearly 8% to about $720 million, while net income followed suit dropping roughly 7.3% to just under $497 million [F1].

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 7.2 | 497 | 570 | 720 | -5.0% | -7.3% |

| 2024 | 7.6 | 536 | 773 | 782 | +4.6% | -0.0% |

| 2023 | 7.3 | 536 | 562 | 795 | +0.1% | -10.8% |

| 2022 | 7.3 | 601 | 572 | 832 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 474 | 535 | 17.9 |

| 2024 | 424 | 743 | 20.2 |

| 2023 | 383 | 526 | 24.1 |

| 2022 | 332 | 536 | 31.8 |

Source: SEC companyfacts cache [F1].

Revenues fell for the first time after multiple years of generally positive gains; margins compressed marginally amid inflationary pressures.

Operating cash flow declined sharply by more than one quarter (-26%) from $773 million down to about $570 million while capital expenditures ticked up to $35 million [F1]. Despite this pressure on cash flows, free cash flow remains strong near half a billion dollars—sufficient to support robust dividend payments which have escalated steadily over recent years.

Return on equity holds at around an efficient mid-to-high teens level (~18%), evidence of disciplined deployment of capital even as profit metric softness emerged last year [F1].

Business Model and Competitive Position

Watsco's scale affords advantages contesting a fragmented industry populated by over two thousand small- to mid-sized wholesalers specializing in HVAC distribution that collectively serve an estimated wholesale market of approximately $74 billion annually in the U.S., per third-party IBISWorld analysis cited within SEC filings [S25]. On an installed basis (including contractor value-add), the residential market reaches roughly double that figure.

Carrier Global Corporation dominates Watsco’s vendor portfolio accounting for nearly two-thirds (62%) of total product purchases alongside Rheem at approximately an eighth (8%), resulting in significant supplier concentration risk given their combined weight at nearly three-quarters of sourcing volume [S1][S20]. Carrier offers numerous brands including Bryant, Payne, Tempstar among others plus private-label lines like Grandaire exclusive to Watsco. Rheem contributes classic brand products as well as private-label offerings from Nordyne—a subsidiary—strengthening vendor partnerships but exposing Watsco to dependencies on OEM supply reliability.

Distribution agreements including exclusivity provisions reinforce territorial control strategies while maintaining acquired brands’ local identities preserve customer loyalty established pre-acquisition [S1][S8][S20]. The dense network supports quick fulfillment onsite via company trucks or outsourced logistics enhancing service responsiveness—a critical factor especially for emergency replacement demand.

Growth Prospects

Watsco aims to sustain its growth through:

Acquisitions: The company has completed dozens of regional tuck-in deals historically including recent additions like Hawkins HVAC Distributors and Southern Ice Equipment expanding presence geographically or into complementary refrigeration verticals [S16][S22]. Acquisitions remain central though integration complexity and risk persists including potential customer attrition or operational controls gaps as highlighted under risk factors [S14][S21].

Organic Initiatives: Expanding product portfolios beyond traditional HVAC equipment into related parts & supplies plus commercial refrigeration products broadens wallet share among contractors already serviced; private-label product development supplements this effort [S7][S8].

Technology Investment: A technological edge aimed at improving customer experience and operational efficiency includes mobile applications (iOS/Android), e-commerce platforms tailored for contractor interaction, pricing optimization software managing thousands of pricing records dynamically, advanced business intelligence reporting tools, and AI-enhanced customer service modules leveraging both internal data sets and external innovation partnerships under Watsco Ventures LLC auspices [S8][S11]. Notably digital platforms such as OnCall Air® sales and financing improve end-customer acquisition.

However headwinds loom: the tight supplier roster amplifies vulnerability to supply chain interruptions or pricing hikes partly due to geopolitical tensions affecting components sourced primarily from China and Mexico; proposed tariffs or regulatory changes might increase costs leading potentially to price inflation impacting demand elasticity adversely [S20]. Additionally competitive pressure is intensifying not only from other independents but manufacturer-owned distribution systems wielding factory direct sales advantages though often lacking broad inventory depth or geographic coverage compared with Watsco’s scale advantages [S21]. Economic cyclicality impacting new construction activity also weighs on demand patterns.

Financial Outlook & What To Watch

Although explicit management guidance was not detailed in recent filings,[N1] signals include:

- Continuing selective acquisitions targeting niche leaders or entry into adjacent verticals,

- Monitoring integration effectiveness given historical acquisition breadth,

- Investment pacing on technology projects balanced against cost control objectives,

- Response strategies against supply chain fluctuations especially relating to core Carrier/Rheem products,

- Dividend consistency reflecting confidence in underlying cash flows while managing leverage conservatively ([F1],[S10]).

Watching quarterly results for signs of stabilization or recovery following FY2025 revenue contraction will be crucial along with margin trends amid inflationary cost pressures.

Capital Allocation & Returns

Watsco exemplifies disciplined capital stewardship prioritizing shareholder returns alongside reinvestment:

- Dividends paid increased materially from $332 million in FY2022 to nearly $474 million in FY2025 demonstrating commitment to returning cash even when earnings dipped last year [F1][S13][S23].

- Share repurchases have been opportunistic facilitated through At-The-Market offering programs providing flexibility without mandating rigid buyback schedules[S13][S16].[N12]

- Capital expenditures remain moderate relative to overall operating cash flow supporting infrastructure maintenance plus technology upgrades without excess capex leverage exposure—FY2025 CAPEX rose modestly YoY yet stayed below CFO significantly ensuring healthy free cash flow generation exceeding $500 million annually ([F1]).

- With equity totaling nearly $2.8 billion by end FY2025 against net income just shy of half a billion, ROE hovers around mid-to-high teens reflecting solid efficiency despite near-term earnings softness ([F1]).

Liquidity remains strong evidenced by a current ratio above four times indicating ample coverage of short-term obligations ([F1],[S10]). Continued access to credit lines provides financial flexibility should strategic acquisition opportunities arise enhancing long-term growth optionality.

Risks & Uncertainties

Key risks flagged by management cover:

- Supplier concentration risks heavily weighted towards Carrier & Rheem; disruption could affect operations materially especially if regulatory compliance on refrigerants or environmental factors impact manufacturing quickly without alternative sources ready [S14][S20].

- Trade policy shifts increasing tariffs or supply constraints particularly involving Chinese/Mexican components may inflate input costs reducing competitive pricing ability.

- Integration risks linked with recent/future acquisitions including cultural alignment issues or loss of key customers/employees could impair financial performance.

- Competitive dynamics include both deep-pocketed local/national distributors plus manufacturers' captive channels potentially eroding market share through pricing pressure.[S21]

- Cybersecurity remains an ongoing threat enterprise-wide amplified by automated attacks using AI tools though mitigation efforts are ongoing.[S21]

- Exposure to natural disasters prevalent in core warm-weather Sun Belt regions requiring contingency planning.[S27]

- Goodwill impairment risks inherent given significant intangible asset base (~33% of assets); adverse changes might compel write-downs.[S14]

Conclusion

Watsco retains a commanding position in the North American HVAC/R distribution industry built through scale-driven advantages, a broad geographic network centered on growth corridors, strong vendor relationships anchored by major brands like Carrier and Rheem, as well as innovation-led improvements adding competitive differentiation via digital transformation. Nevertheless fiscal-year results confirm headwinds challenging recent growth momentum marked by declining revenues and profits adapting amidst supply concentration vulnerabilities alongside macroeconomic pressures. Capital allocation remains prudent embedding healthy dividends supported by substantial free cash flow despite these cyclical pressures. Future performance will hinge on execution across managing supplier risk exposures effectively while continuing disciplined acquisitions integration plus expanding technology-enabled service delivery cultivating contractor loyalty amid vigorous competition. Investors should monitor interim earnings announcements closely along with progress reports on innovation initiatives coupled with macro trade developments impacting key input costs.

Disclaimer: This report is prepared solely for informational purposes without any recommendation on investment decisions regarding WATSCO INC securities. Readers should conduct their own due diligence and consult professional advisors if needed.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments