Western Union’s Q1 Performance Highlights Operational Costs and Growth Challenges

Q1 earnings reflect higher incentive-related expenses and stable revenue amid ongoing regulatory and competitive headwinds.

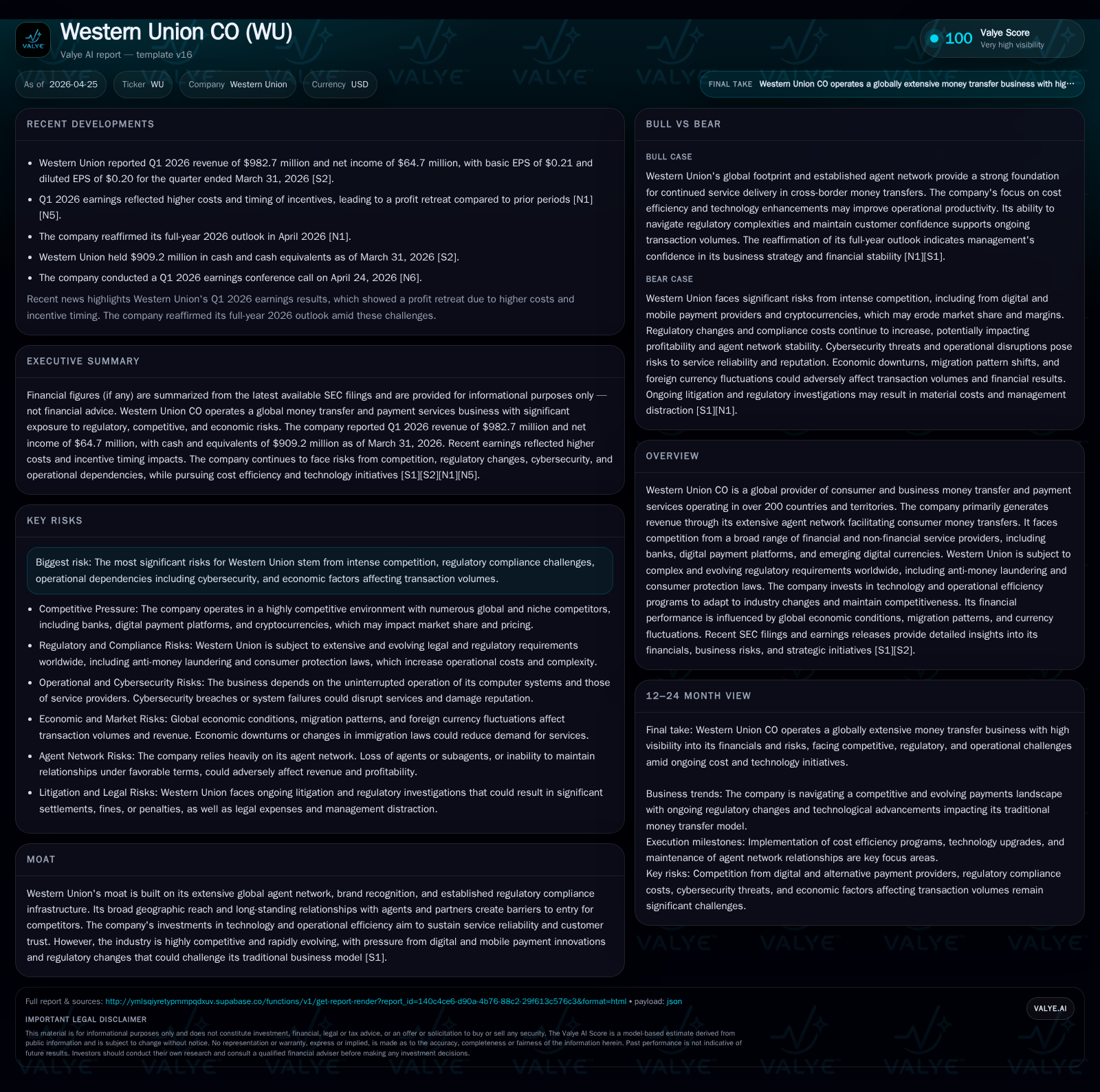

Western Union reported Q1 2026 results marked by a miss on earnings expectations driven primarily by timing of incentive costs, despite largely stable core revenue streams. The company reaffirmed its FY26 guidance, signaling confidence but highlighting the persistent operational and regulatory challenges facing its legacy global money transfer model. Western Union’s extensive agent network remains a competitive strength, yet digital disruption and escalating compliance demands continue to pressure margins and growth potential. Investors should monitor agent network dynamics, digital adoption rates, and regulatory developments closely in the near term.

Latest Quarterly Results and Operational Update

Western Union’s first quarter 2026 results released in the April 24 SEC filings [S2] revealed an earnings miss relative to analyst expectations. The shortfall centered on elevated incentive expenses that were accelerated in timing during the quarter rather than indicating ongoing profitability deterioration [N1][N3]. Revenue remained largely stable compared to prior periods, reflecting resilience in the company’s core agent-facilitated money transfer volumes despite macroeconomic headwinds. Operating income saw modest improvement when excluding one-time expense timing effects.

Importantly, management reaffirmed its full-year guidance for 2026 during post-earnings commentary and supplemental event filings [S3][N7], signaling confidence in navigating current pressures. The cost dynamics underscore a transitional phase where operational investments and incentive programs are front-loaded to support sales or technology initiatives. These near-term cost pressures are juxtaposed against a business model still exposed to variable demand drivers such as global migration patterns and currency fluctuations.

This quarterly update matters now as it encapsulates the ongoing tension between maintaining a vast global footprint reliant on third-party agents while adapting both operationally and technologically to fast-evolving industry competition and regulatory environments.

Western Union’s Business Model and Revenue Drivers

At the heart of Western Union's revenue generation is its expansive global agent network spanning over 200 countries and territories [S1]. This network facilitates primarily consumer-to-consumer money transfers—a transaction style that remains critical particularly in corridors involving remittances tied to migrant workers sending funds home. Fees collected from these transactions constitute the bulk of Western Union's revenue.

The company's competitive moat lies in its entrenched relationships with agents who operate physical payout locations worldwide—a significant switching cost for customers reliant on cash-based disbursements or those with limited access to digital infrastructure. Although Western Union has made strides toward digital channels including mobile wallets and online platforms, cash-to-cash transfers through agents still dominate volumes.

From an operational standpoint, sustaining this extensive agent ecosystem requires continuous investment not only in recruitment but also training, compliance oversight, and commission structures aligned with local market economics. Migration patterns heavily influence demand volumes across its key corridors; thus geopolitical and economic shifts materially impact transaction flows.

Global Remittance Industry Structure and Competitor Assessment

Western Union operates within a fragmented remittance landscape characterized by multi-tiered competition. Traditional competitors include global banks offering cross-border remittance services often bundled with broader banking products. However, the most disruptive forces stem from fintech platforms—including app-based money transfer startups—and digital payment networks leveraging lower-cost infrastructures.

Adding complexity is the rise of digital currencies such as cryptocurrencies that offer alternative value transfer mechanisms bypassing conventional financial intermediaries. These innovations enable faster settlement times at reduced fees but face regulatory hurdles limiting broad adoption presently.

Pricing power across segments is constrained as consumers exhibit high price sensitivity given transaction frequency tied to family support needs. Regulatory regimes across jurisdictions further complicate market entry due to stringent anti-money laundering (AML), know-your-customer (KYC), sanctions screening, and licensing requirements which impose heavy compliance expenditures [S1].

From a capacity perspective analogous to supply chain dynamics, the agent network's size, exclusivity of contracts where enforceable, and retention capabilities represent key bottlenecks constraining rapid geographic expansion or scaling new product offerings swiftly [S1]. Compliance infrastructure functions thus double as both a moat protecting incumbent positions but also as a drag on margin expansion.

Growth Opportunities and Headwinds in Digital Transition

Western Union recognizes digitization as an essential vector for future growth but faces structural headwinds owing to its legacy agent-centric model. The company invests heavily in technology upgrades aiming at enhancing customer experience through app development, automated fraud detection using machine learning algorithms, AI-enabled decisioning for risk assessments, and streamlined onboarding processes for agents.

However, gains from these initiatives may be incremental given customer segments still favor offline cash channels due to perceived convenience or lack of banking access. Younger demographics appear more willing to adopt mobile-first alternatives offered by fintech challengers which threatens Western Union’s historic dominance among certain cohorts.

Investment in technology also raises compliance costs since digital channels require rigorous monitoring under AML/KYC regimes compounded by increasing data privacy regulations globally [S1]. Consequently, margins face compression as incremental spending absorbs gains from operating efficiencies.

Migration flows—the backbone of remittance demand—remain subject to uncertain economic cycles capex funding ceilings to align with evolving regulation alongside competitive incentives will be critical determinants shaping Western Union's growth trajectory.

Regulatory Environment and Compliance Challenges

A defining characteristic of Western Union’s operating environment is its exposure to complex multilayered regulations worldwide designed primarily to combat money laundering, terrorist financing, fraud mitigation, sanctions enforcement, consumer protection laws, and stringent licensing requirements [S4–S9].

The company remains subject to ongoing obligations stemming from previous settlement agreements involving multi-agency scrutiny including the DOJ and FTC. These mandates have increased operational overhead requiring enhanced due diligence protocols across the agent base including mandatory training programs, transaction monitoring systems upgrades, recordkeeping enhancements, consumer reimbursement procedures for fraud victims, agent suspension mechanisms, and independent compliance audits.

Failure by Western Union or any third-party agents/subagents under its umbrella risks severe penalties including fines, license revocations or restrictions on service offerings—all directly impacting revenue generation ability and reputation capital.

Data privacy laws such as GDPR in Europe impose additional burdens regarding customer information handling standards; recent expansions within UK regulatory frameworks add unique domestic layers increasing cost complexity further [S5][S12].

Overlapping regulatory schemes across jurisdictions create challenges around consistency in application leading sometimes to contradictory mandates necessitating costly adaptations affecting profitability negatively without immediate revenue benefit.

Forward-looking Parameters: Guidance and Execution Risks

Management’s April filings confirmed full year 2026 guidance reflecting stable revenue growth trajectory supported by ongoing investments balanced against cost disciplines tethered closely due to current inflationary cost pressures particularly linked to employee incentives [S2][S3][N7]. Key milestones critical for evaluation include renewal or renegotiation outcomes of major agent contracts especially where exclusivity may be curtailed by new legal interpretations limiting latitude previously enjoyed by the firm.

In parallel monitoring adoption rates within newly launched or improved digital products will serve as early indicators whether structural shifts toward technology-led transfers can gain meaningful traction sufficiently quickly enough to alter long-term margins positively.

Execution risks comprise potential workforce disruptions associated with restructuring efforts targeting efficiency gains; failures here could translate into operational instability impacting customer service reliability at agent outlets [N2]. Furthermore regulatory evolution remains a wildcard wherein emerging statutes or enforcement actions might necessitate abrupt business model adjustments incurring unforeseen expenses or curtailing previously planned initiatives impeding growth prospects.

Financial Overview: Profitability, Liquidity, and Capital Structure

Reflecting Q1 performance alongside annual trends drawn from latest company facts data [F1] complemented by SEC disclosures [S2], Western Union shows:

- Revenue decreased by approximately 3.8% year-over-year comparing FY2025 ($4.0507B) versus FY2024 ($4.2097B), indicative partly of macroeconomic headwinds constraining volume growth.

- Operating income improved modestly by around 4.3% year-over-year despite the revenue dip reflecting efficiency initiatives offsetting some cost pressures ($757M vs $726M FY25 vs FY24).

- Net income contracted significantly by about 46.5%, primarily attributable to non-recurring expense timing related impacts flagged during Q1 filings illustrating sensitivity to incentive program scheduling [$499.6M vs $934.2M FY25 vs FY24].

- Operating cash flow showed strong growth (+33.8%) aided by working capital optimization reaching $543.7M supporting liquidity needs.

- Capital expenditures maintained a conservative profile ($38.5M) consistent with investment focus on technology enhancements without aggressive capacity expansion.

- Dividend payments continue at roughly $309M underpinning shareholder return policy alongside buybacks albeit below peak historical levels ($234M) reflecting prudent capital deployment amid uncertainty.

- At quarter-end March 31 2026 cash & equivalents stood robustly at $909M against total debt of $2.33B yielding net debt near $1.43B sustaining manageable leverage ratios supportive of refinancing flexibility if required.[F1]

|

| FY | Revenue (USD B) | Op Income (USD M) | Net Income (USD M) | Rev YoY % | OpInc YoY % | Net YoY % |

|---|---|---|---|---|---|---|

| 2025 | 4.05 | 757 | 500 | -3.8% | 4.3% | -46.5% |

| 2024 | 4.21 | 726 | 934 | |||

| 2023 | 4.36 | 818 | 626 | |||

| 2022 | 4.48 | 885 | 911 |

Historical performance (annual)

|

| FY | Rev ($bn) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 4.1 | 500 | 544 | 757 | -3.8% | -46.5% |

| 2024 | 4.2 | 934 | 406 | 726 | -3.4% | +49.2% |

| 2023 | 4.4 | 626 | 783 | 818 | -2.6% | -31.3% |

| 2022 | 4.5 | 911 | 582 | 885 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

|

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 309 | 235 | 505 |

| 2024 | 322 | 186 | 369 |

| 2023 | 349 | 308 | 760 |

| 2022 | 364 | 370 | 550 |

Source: SEC companyfacts cache [F1].

This financial profile highlights solid underlying operations buttressed by ample liquidity positioning but simultaneously outlines margin fragility subjected to discrete costs related notably to incentive programs reflecting transitional dynamics in operating models.

Conclusion

Western Union’s Q1 report underscores enduring challenges confronting established global remittance providers balancing large scale physical networks with pressures imposed by technological innovation and intensifying regulatory oversight globally. While core transactional volumes via agents maintain stability supported by entrenched market positions especially in developing economies reliant on cash payouts, secular trends towards digitization accompanied by escalating compliance costs present persistent margin headwinds.

Execution risks center around maintaining agent network integrity amid competition legally limiting exclusivity agreements while successfully accelerating user shift towards digitally-enabled payment modalities that promise higher margins but require patient capital deployment paired with effective risk management frameworks highly attuned to evolving regulatory imperatives.

Financially well-capitalized with adequate liquidity buffers providing runway for strategic initiatives sets Western Union on cautious footing respecting both opportunity potentials juxtaposed against realistic constraints within complex global operating environments.

Investors should track future quarterly updates focusing specifically on updates around: agent contract renewals under jurisdictional contestability; digital transfer adoption metrics evidencing disruptive potential; adjustments stemming from further regulatory developments; plus operational efficiency realization post-incentive expense cycles signaling stabilization beyond temporary noise indicated in recent quarters.

-- This analysis synthesizes available public disclosures without offering investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments