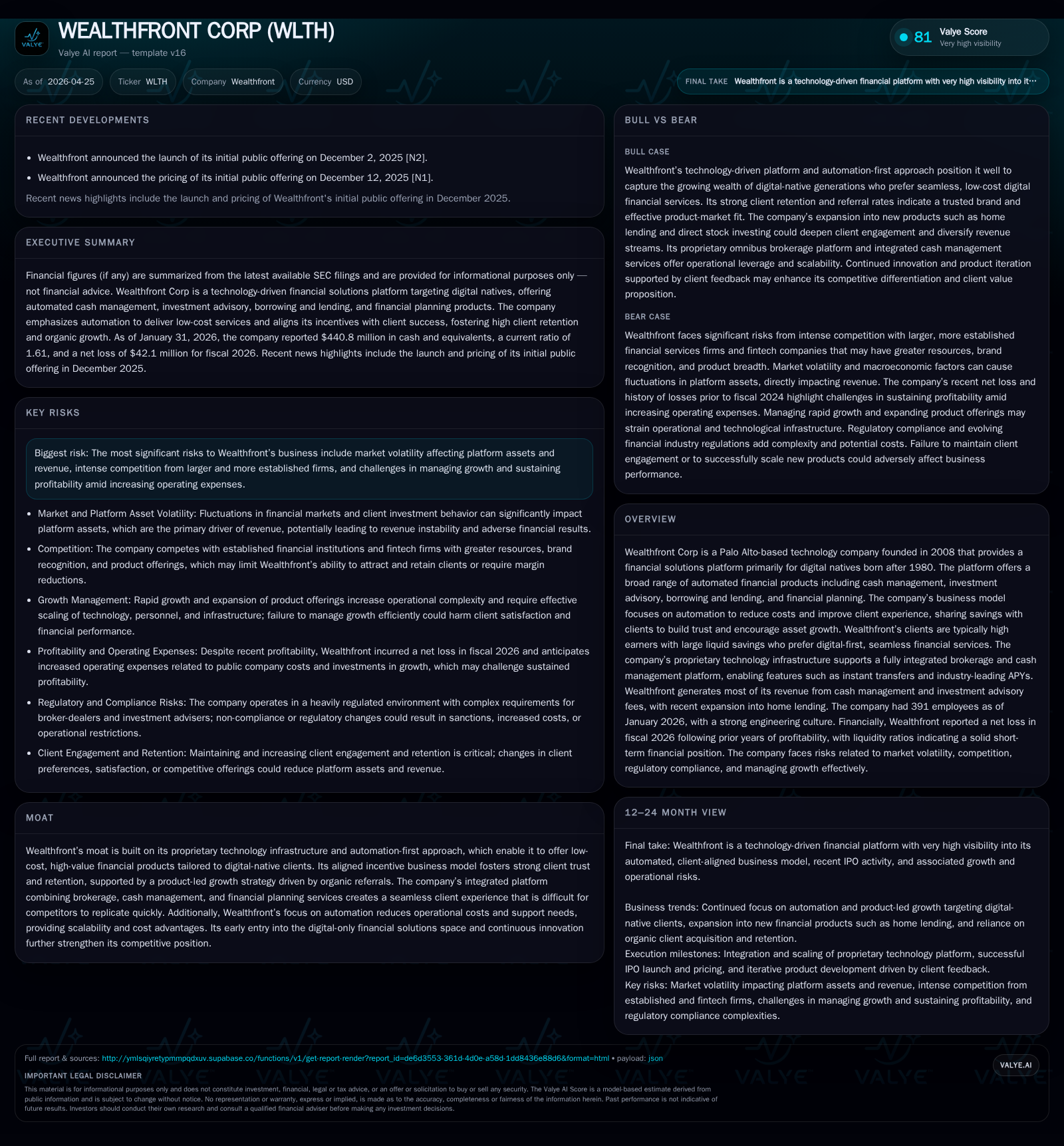

Wealthfront’s Q3 Update Signals Growth Challenges in Digital Wealth Management

Wealthfront’s latest quarterly filing reveals early signs of slowing growth as the company navigates competitive and market pressures with its automation-driven financial platform.

In its Q3 2026 10-Q filing, Wealthfront disclosed continued revenue growth paired with deceleration relative to prior periods, alongside an expanding workforce reflecting ongoing investment in platform scalability and product development. The company’s automation-first business model underpins a low-cost, integrated financial platform targeted at digital natives, fostering organic growth primarily through client referrals. However, macroeconomic uncertainty and intensifying competition from both traditional incumbents and fintech disruptors pose challenges to sustaining momentum. Key near-term indicators include client engagement levels and adoption of new product features, which will signal whether Wealthfront can leverage its technology moat to maintain industry relevance and accelerate expansion.

Q3 2026 Operating Update: Indicators of Growth Moderation

Wealthfront's latest quarterly filing (10-Q dated January 23, 2026) illuminates subtle shifts in its operating trajectory, providing an early signal that the company's historically rapid expansion may be tempering. While total revenue grew from $226.2 million for the first nine months of fiscal 2025 to $268.9 million for the same period in fiscal 2026, the pace of this increase has shown signs of deceleration compared with previous periods [S2]. Concurrently, employee headcount expanded from 318 to 376 over twelve months ending October 31, 2025 — a clear indication that Wealthfront continues to invest heavily in its engineering, product development, and operational staff to support future scaling [S2].

Management commentary within these filings hints at the growing challenge of balancing sustained top-line growth with rising operating expenses related to deepening platform capabilities. The accompanying March 11 event filing (8-K) confirms these dynamics without material changes to strategic focus but signals attentiveness toward optimizing cost structures while pursuing growth [S3]. In aggregate, these disclosures portray a maturing digital wealth management firm navigating the inflection point between rapid startup growth phases and longer-term sustainable scale.

Business Model Overview: Automation and Aligned Client Incentives

At its core, Wealthfront leverages a proprietary technology infrastructure designed around an automation-first philosophy that permeates product delivery, internal operations, and client interactions [S1]. This approach enables the company to operate at some of the industry's lowest cost bases while maintaining seamless service quality—a distinct advantage amid competitive pressures seeking scale economies.

Wealthfront’s revenues primarily derive from two pillars: cash management services—including sweep programs—and investment advisory fees calculated as a percentage of assets under management net of fee waivers [S1]. Notably absent are transactional fees or conflicted human advice models; instead, Wealthfront explicitly aligns its success with clients’ financial outcomes. This not only builds robust trust but fuels an organic referral engine wherein more than half of new clients over recent years originate through existing client recommendations—a rarity among digital-native financial platforms [S1].

This business model thrives on high user retention supported by transparent pricing that shares operational savings back to clients. The cycle is iterative: lower costs lead to better returns for clients which strengthens trust and prompts additional asset inflows and word-of-mouth growth. Such alignment contrasts significantly with incumbent wealth managers often burdened by legacy cost structures and commission conflicts.

Product Portfolio and Service Quality: A Fully Integrated Platform

Wealthfront’s product suite exemplifies breadth combined with integration—a significant differentiator in digital wealth management targeting tech-savvy digital natives born post-1980 [S1],. Beyond automated investing portfolios, the platform offers cash sweep programs that deliver competitive annual percentage yields (APYs), borrowing solutions such as personal lines of credit (PLOC) enabled through partnerships with custodial banks like RBC Clearing & Custody [S1], and comprehensive financial planning tools embedded within the same interface.

The seamless client experience derives from end-to-end automation reducing reliance on manual intervention in product launches or service fulfillment. This architecture facilitates rapid iteration cycles while maintaining quality control standards typically challenging for firms attempting to integrate disparate offerings or outsource components.

From a sector perspective, such integration raises switching costs by embedding clients deeper into one ecosystem—beneficial given digital natives’ preference for unified mobile experiences paralleling their interactions across entertainment or commerce platforms. Furthermore, scalable automation supports future expansion without linear increases in support costs—a key metric for profitability progression.

Industry Dynamics and Competitive Environment

The digital wealth management space where Wealthfront competes is characterized by intense rivalry spanning large well-capitalized incumbents (traditional wealth managers with extended brand reach) as well as nimble fintech entrants innovating rapidly in niche product areas [S1],. This dual-front competition compresses margins while elevating client expectations around seamless experiences blended with transparent fee policies.

Wealthfront’s early mover advantage—building an integrated platform focused exclusively on digital-native investors—constitutes a notable moat rooted in proprietary technology and experience-driven automation capabilities. Yet challenges persist: platform asset levels remain susceptible to macroeconomic volatility that can swiftly alter advisory fees; larger competitors wield substantial marketing budgets capable of undermining organic referral momentum; regulatory standards continuously evolve potentially impacting operational scope.

Despite these pressures, Wealthfront's fully automated approach paired with aligned incentives differentiates it sufficiently in a crowded market. It eschews costly human advisory models while maintaining a trust-based engagement vital for long-term retention.

Growth Drivers and Constraints on Expansion

Key catalysts underpinning future Wealthfront growth stem from further enhancements in automation-enabled product offerings combined with deepening adoption among its core digital-native clientele [S1], [S2]. The drive to extend feature sets—in areas such as lending products or advanced financial planning algorithms—could unlock incremental wallet share while attracting adjacent customer segments narrowly underserved by incumbents anchored in legacy models.

However, several constraints loom large. First is moderating new client acquisition due partly to saturation effects within target demographics and partly owing to intensifying competition diluting attention. Second involves market cycles inducing asset value fluctuations that directly impact investment advisory fee revenue streams. Third are scaling costs associated with maintaining platform security and regulatory compliance—necessary burdens amid rising cybersecurity threats frequently highlighted in industry risk disclosures [S1].

Management's recent remarks underscore a cautious yet proactive posture balancing investment spend against measured returns—echoing industry-wide recognition that late-stage growth phases increasingly prioritize operational efficiency without sacrificing innovation velocity.

Key Performance and Execution Signals to Monitor

Looking ahead, critical indicators include shifts in client referral rates which historically have underpinned organic growth sustainability; finer grained metrics around adoption rates for recently launched financial products; attrition statistics reflecting customer satisfaction levels; and qualitative guidance on expense management strategies revealed during quarterly updates post Q3 FY26 filings [S2], [S3].

Further milestones such as rollout timing for enhanced borrowing features or integrations with third-party financial tools will also serve as barometers for execution discipline and competitive differentiation. Meanwhile, any commentary addressing responses to regulatory changes or emerging cybersecurity challenges will offer insight into the firm’s resilience frameworks.

In sum, Wealthfront stands at a juncture requiring careful navigation between solidifying technological moats while asserting continued relevance to evolving client needs—all amidst an environment marked by shifting macro-financial conditions.

This analysis reflects information current as of April 2026 based strictly on SEC filings provided. It aims to offer an objective assessment of Wealthfront Corporation's operating context without providing investment advice or forecasting outcomes.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments