Summit Networks’ Shift to a Logistics Platform: Strategic Execution and Acquisition Readiness

Summit Networks concludes internal development and strengthens governance as it pursues an acquisition-driven logistics business model in Asia.

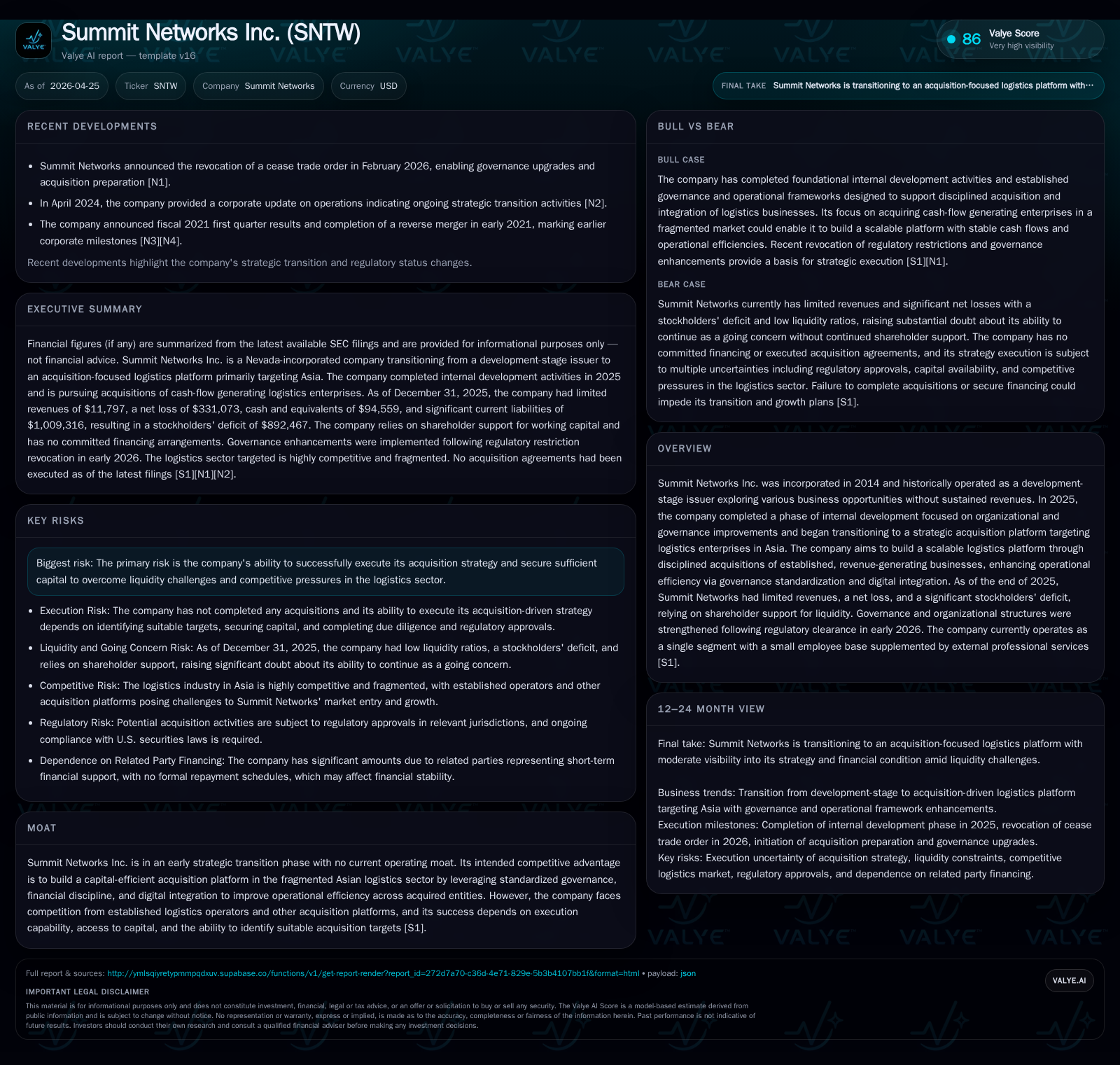

Summit Networks Inc. has transitioned from a development-stage entity to a strategic acquisition platform targeting cash-flow stable logistics companies primarily in Asia. The company completed its internal capability-building phase by the end of 2025, including digital workflow frameworks and governance enhancements, setting the foundation for upcoming acquisitions. Despite these advances, Summit faces significant liquidity constraints, a stockholders' deficit, and no executed acquisition agreements yet, making execution capability and access to capital key risks. Governance upgrades and office relocation in early 2026 reflect efforts to professionalize operations ahead of deal activity.

Latest Operating Update Highlights Internal Development Completion

Summit Networks Inc., historically a development-stage issuer exploring diverse business avenues without sustained revenues, reported the completion of a crucial internal development stage by December 31, 2025 [S2], [S1]. This period focused extensively on building operational capacities through research into internal systems and deployment of scalable digital workflows. These initiatives were explicitly non-commercial and time-limited, culminating with the termination of associated project contracts at year-end 2025. Management confirms that this phase achieved its intended foundational goals, marking a shift from exploratory activities toward readiness for active business moves.

While revenues remained minimal at $11,797 for fiscal 2025 [F1], the importance lies less in current commercial traction and more in having established the groundwork necessary for future acquisitions and integrations. The company’s Q4 2025 filing underscores transitioning from capability-building to executing an acquisition-driven strategy as central to 2026 planning [S2], [S1].

Business Model Transformation: From Exploration to Acquisition Platform

Summit Networks' business model has pivoted sharply from exploratory ventures toward becoming a capital-efficient acquisition platform within the fragmented Asian logistics sector [S1]. The strategy centers on acquiring controlling stakes in well-established logistics enterprises exhibiting predictable cash flow stability rather than cultivating organic growth internally.

Management envisions deploying the digital workflows, governance protocols, and financial discipline frameworks developed during 2025 as integration tools post-acquisition. This approach aims at driving operational efficiencies across multiple acquired entities—a classic roll-up model intended to aggregate scale advantages while maintaining lean overhead through standardized governance.

This transformation represents a move away from Summit’s historical pattern of one-off commercial initiatives without sustained revenue generation towards orchestrating platform growth driven by disciplined M&A activity [S1]. However, a caveat emphasized by management notes that no acquisition agreements have been signed thus far, confirming the nascent stage of transactional execution.

Competitive Dynamics in Asian Logistics and Summit’s Positioning

Asia's logistics industry is characterized by fragmentation with abundant regional operators serving both intercity freight forwarding and last-mile deliveries. Summit enters a crowded arena featuring entrenched providers alongside other consolidation candidates aiming to harness scale effects [S1].

From an analyst's perspective, such sector dynamics offer double-edged implications: fragmentation indicates opportunity for platform consolidation but also magnifies due diligence complexity alongside capital intensity challenges inherent in acquiring credit-worthy targets.

Summit's competitive angle hinges on applying standardized governance structures emphasizing financial prudence combined with selective digital integration—a model seeking differentiation through disciplined operational control rather than service innovation or geographic niche dominance [S1]. This governance-led playbook could unlock margin improvements if successfully applied across diverse acquisitions but requires significant execution rigor amid competitive pressure for suitable targets.

Growth Drivers and Constraints for Summit’s Acquisition Strategy

Key growth drivers rest heavily on consummating strategic acquisitions that provide stable cash flows enabling reinvestment in operational improvements. The foundational year of internal tool-building sets up potential post-merger integration efficiencies critical for platform scalability [S1], [S3].

However, substantial constraints temper enthusiasm:

- The absence of committed external financing or formal acquisition agreements highlights ongoing capital access challenges.

- Liquidity pressures necessitate reliance on shareholder support for working capital—raising doubts about seamless deal funding absent new capital infusion.

- Regulatory clearances turned favorable after February 2026 revocation of prior restrictions facilitate freer operational movement but impose ongoing compliance demands [S1], [S3].

These constraints contribute to execution risk whereby delay or inability to close meaningful acquisitions could stall strategic ambitions.

Governance Enhancements and Organizational Restructuring Post-Regulatory Clearance

Following regulatory easing in early 2026, Summit implemented significant governance reforms including board restructuring with independent appointments (Ross Miller as audit committee chair among others) aimed at bolstering oversight of audit functions, financial controls, and overall strategic review processes [S3], [S26].

Complementing these board-level upgrades was relocation of the principal executive office to Miami, Florida—signaling geographic repositioning aligned potentially with capital markets proximity or logistics market engagement strategies [S3].

A streamlined management structure clarifying executive responsibilities now underpins centralized decision-making necessary for disciplined acquisition assessment and approval workflows [S1], [S10]. This governance sophistication marks a material step in creating investor confidence requisite ahead of active transaction pursuits.

Key Risks Affecting Execution and Capital Access

Despite advancements, Summit’s foundational vulnerabilities remain pronounced:

- Stockholders’ equity deficit stood at approximately -$892k at year-end 2025 illustrating negative net worth—an anchor constraining creditworthiness [F1].

- No committed external financing exists; reliance on shareholder loans (total related-party advances nearing $957k as of end-2025) introduces dependence on continued backing without formalized repayment schedules or cost-of-capital benchmarks [S10].

- Operational risks include ability to identify accretive targets amidst competition from more established platforms possessing deeper pockets or regional expertise.

- Regulatory compliance failures pose reputational risks especially as filings note ongoing disclosure obligations under US securities laws despite limited operating presence.

Management’s going concern disclosures accentuate these execution risks although they emphasize cost control and conservative liquidity management as mitigating factors [S1], [F1].

Next Milestones: Acquisition Pipeline and Capital Strategies

Critical short-term milestones revolve around:

- Signing definitive acquisition agreements evidencing transition from pipeline evaluation into transactional closure phases.

- Announcing financing arrangements tied directly to specific acquisitions rather than general operating purposes signaling functional activation of the capital raise strategy outlined by management.

- Demonstrating due diligence advancement including integration planning which would indicate readiness beyond paper strategies.

- Continued governance refinements ensuring full regulatory compliance amplify institutional credibility necessary for attracting partners.

- Monitoring liquidity events such as further shareholder support or third-party bridge financings providing runway extension.

Observers should interpret these event markers as primary indicators of momentum; failure here heightens probability that strategic transition stalls into mere intent rather than tangible growth vector.

Financial Overview: Liquidity, Losses, and Going Concern Status

Historical performance (annual)

|

| FY | Net ($) | CFO ($) | OpInc ($) | Net YoY |

|---|---|---|---|---|

| 2025 | -331073 | -265848 | -320220 | -236.3% |

| 2024 | -98434 | -57096 | -98434 | -514.0% |

| 2023 | 23778 | -59305 | -165362 | +122.0% |

| 2022 | -108205 | -72049 | -108205 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

|

| FY | ROE% |

|---|---|

| 2025 | 37.1 |

| 2024 | 23.9 |

| 2023 | -4.4 |

| 2022 | 14.2 |

Source: SEC companyfacts cache [F1].

|

| FY | Revenue (USD) | OpInc (USD) | NetInc (USD) | Cash (USD) | Curr Liab (USD) | Equity (USD) |

|---|---|---|---|---|---|---|

| 2025 | 11,797 | -320,220 | -331,073 | 94,559 | 1,009,316 | -892,467 |

Fiscal 2025 results illustrate nominal revenue generation contrasting dramatically with elevated operating expenses driving deep losses near $331k year-over-year worsening by over 230% from prior period levels [F1]. Operating cash flow underscored bleeding at $265k outflows overshadowing modest capex spending around $6.9k consistent with infrastructure buildout but insufficient for core operations scale-up.

Balance sheet metrics indicate a challenging liquidity position with current assets of $112,229 against current liabilities exceeding $1 million, resulting in a low current ratio of approximately 0.11 [F1]. Negative equity further signifies accumulated deficits eroding shareholder value creating heightened risk profiles when considering borrowing capacity or market financing options absent fresh injections from owners.

Management commentary aligns with filing evidencing strategic conservatism emphasizing cost discipline alongside continued dependence on related party funding totaling nearly a million dollars without formal repayment schedules or interest burdens—a stopgap solution pending acquisition closure or capital raise success [S10], [F1]. The going concern qualification confirms material uncertainties around sustainable operations but underlines belief conditional on successful execution of new strategy plan supported by shareholders' backing.

This analysis synthesizes Summit Networks Inc.’s filings through late April 2026 to evaluate its transition from development-stage exploration toward an acquisition-focused logistics platform primarily targeting fragmented Asian markets. While foundational steps including governance upgrades and digital framework completion position the company structurally for acquisitions, severe liquidity limitations coupled with unproven deal execution create substantial risk hurdles. Monitoring subsequent definitive transaction announcements alongside capital raise developments will be pivotal in assessing whether Summit can translate its strategic vision into sustainable operational reality.

This memorandum is prepared solely for informational purposes based on publicly available SEC filings as specified; it does not constitute investment advice nor an inducement to trade securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments