Zillow Group's Strategic Resilience Amid Profitability and Rising Real Estate Tech Competition

Zillow’s Q4 profit turnaround underscores its ability to navigate evolving market dynamics while facing mounting competitive pressures.

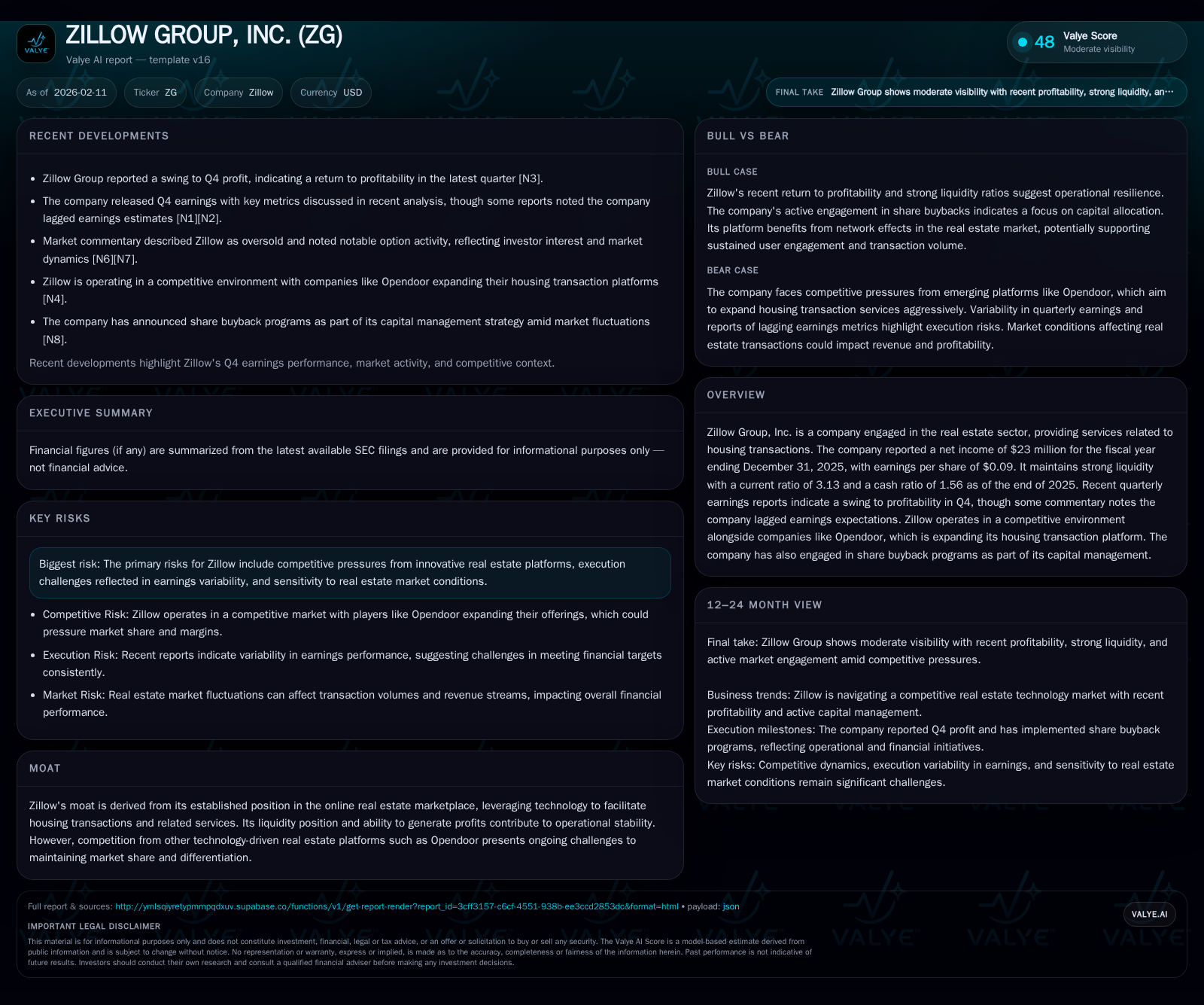

Zillow Group, Inc. swung to profitability in Q4 2025 with a net income of $23 million and EPS of $0.09, signaling operational progress despite lagging some market expectations. The company boasts robust liquidity, supporting its capital strategy that includes active share buybacks. However, Zillow faces intensifying competition from platforms like Opendoor, which are broadening their real estate transaction capabilities. Moving forward, Zillow’s established online presence must continuously evolve to sustain its moat amid execution challenges and market sensitivities inherent in the housing sector.

From Red to Black: Dissecting Zillow’s Q4 Profit Turnaround

The close of 2025 brought a pivotal moment for Zillow Group as it shifted from losses to a reported net income of $23 million for the full year, culminating in fourth-quarter earnings per share of $0.09 [F1][N1]. This financial swing back into the black after periods marked by profitability swings signals operational leverage beginning to take root within its business model. Yet the profitability was accompanied by an important caveat: the company's Q4 results fell short of analyst estimates [N2]. Such a gap between actual performance and expectations highlights granular execution challenges — perhaps linked to managing costs or capitalizing fully on market demand.

This nuanced outcome suggests Zillow is straddling a critical inflection point; while it has demonstrated the capacity to achieve profit in a tough environment characterized by changing consumer behaviors and macroeconomic headwinds, sustaining momentum will require further precision. The company’s commentary around these results quietly acknowledged areas necessitating improvement, underpinning an ongoing narrative of measured progress rather than outright breakthrough.

Capital Fortification: Assessing Zillow's Liquidity and Buyback Moves

Beyond operational income metrics lies a story of balance sheet strength that fortifies Zillow's strategic options. As of December 31, 2025, the firm commanded a current ratio north of 3.1 with approximately $768 million in cash and equivalents alone [F1]. A cash ratio near 1.56 further underlines an enviable liquidity buffer that provides resilience against market volatility or unexpected disruptions.

This abundant liquidity has enabled management to initiate share buyback programs reported recently [N9], reflecting deliberate capital redeployment intended to enhance shareholder value while signaling confidence in internal outlooks amidst uncertainty. Such buybacks often serve multiple roles: a counterbalance during share price dips, an expression of belief in intrinsic value, and an efficient use of excess cash flows when organic expansion avenues may be constrained or risky.

This combination of robust liquidity plus active capital management practices thus frames Zillow as conservatively prepared yet opportunistic — poised to navigate both incremental growth investments and shareholder returns within a market partial to shifts in consumer spending and financing availability.

Market Dynamics and Player Positioning: Zillow Amidst Rising Competition

Even as Zillow strengthens its internal footing, external forces loom large. The competitive terrain is reshaping under pressure from technologically agile rivals such as Opendoor, which analysts have likened to an "Amazon" for housing transactions due to its broadening platform reach beyond mere listings toward full transaction facilitation [N6][N13].

Opendoor’s strategy underscores a pivotal trend: real estate marketplaces are no longer static portals but increasingly integrated ecosystems encompassing buying, selling, financing, and even homeownership lifecycle services. This evolution challenges Zillow’s traditional model built primarily on listing aggregation complemented by ancillary revenue streams — compelling it to innovate rapidly or risk erosion in relevance.

While Zillow still enjoys strong brand recognition and significant user engagement through its website and apps, the rivalry emphasizes how critical speed-to-market and product depth now are to moat sustainability (more on that ahead). Moreover, shifting consumer preferences for seamless end-to-end solutions elevate the stakes for platform completeness rather than sole reliance on discovery tools.

Moat or Mirage? The Durability of Zillow's Online Real Estate Edge

Zillow’s moat rests on its pioneering role as a leading online real estate marketplace leveraging technology at scale [valye_report_excerpt.moat]. This foundation affords advantages such as brand familiarity, extensive property data sets, and integrated tools for home buyers and sellers. The company’s profitability combined with strong liquidity supports an operational stability rare among peers navigating cyclical markets.

However, this moat is anything but unassailable. Increased competition from innovative tech-centric entrants threatens encroachment into both customer bases and service offerings. Rapidly advancing competitors who can offer more frictionless transactional experiences or better price transparency could challenge Zillow’s differentiation.

Liquidity cushions provide breathing room for investment into R&D or strategic pivots but cannot substitute genuine platform evolution. Execution risks remain visible through uneven earnings performance episodes — indicative that sustaining edge demands not just scale but continued technological leadership coupled with nimble adaptation to fast-changing market ecosystems.

Revenue Streams Unveiled: What Powers Zillow’s Business?

Delving beneath headline profits reveals multiple revenue pillars shaping Zillow’s economic engine [S1][F1]. These encompass residential services including home buying/selling support; mortgage-related fees; revenues from sales operations tied closely to transaction facilitation; rental listing fees; plus advertising revenues generated from display ads on its platforms.

In aggregate, these diverse streams produce complex growth dynamics: residential services remain core but face margin pressure due to competitive discounting and technology investments. Mortgage services fluctuate with interest rate cycles impacting loan origination volumes. Sales revenues depend heavily on transaction velocity within fluctuating housing markets while rentals offer recurring fee potential albeit with less scale relative to other segments.

Advertising revenue benefits from sustained user traffic but contends with shifting digital ad spends amid competitor platforms vying for similar budgets. Taken together, this portfolio demands intricate balancing acts between cross-segment synergies while managing exposure to individual business cycle swings within real estate sectors.

Risk Radar: Execution, Market Sensitivity, and Innovation Challenges

The layered complexities give rise to multiple risk vectors facing Zillow [valye_report_excerpt.risks][N2][S1]. Chief among these is execution variability manifested through lumpy earnings coupled with cost management in an intensely competitive environment. Precision in scaling innovations without diluting margins will continue testing management acumen.

Sensitivity to real estate macro conditions introduces pronounced cyclicality risks — factors such as interest rate shifts, housing supply constraints versus demand imbalances directly influence transaction volumes critical for revenue realization across segments. Additionally, technological disruption fueled by competitors’ innovation speed could undermine customer loyalty or platform preference if not met effectively.

The confluence of these factors underscores that vigilance around strategic investment choices paired with agile responses remains mandatory lest transient headwinds develop into longer-term structural pressures.

Looking Ahead: Strategic Imperatives for Zillow in 2026

As Zillow steps into 2026 post-profit turnaround yet preempted by elevated expectations borne from industry shifts [N3][N7], several imperatives crystallize:

- Continued sharpening of tech-enabled end-to-end solutions enhancing user experience beyond what legacy listings portals offer,

- Commitment to judicious capital deployment balancing share repurchases with investments fueling competitive differentiation,

- Deeper integration across mortgage, sales, rentals segments driving cross-selling efficiencies,

- Focus on data analytics refinement accelerating insight-driven customer engagement,

- Proactive mitigation plans for identified execution risks ensuring consistent profitability trends,

- Stretching brand cachet through partnerships or expansions tapping adjacent real estate service verticals.

Navigating these themes will test how effectively Zillow translates regained profitability into sustainable long-term positioning within an ecosystem evolving toward holistic housing transaction facilitation. While challenges abound—including formidable competitors seeking Amazon-like ubiquity—Zillow's blend of financial fortitude plus longstanding digital marketplace incumbency equips it uniquely if strategic discipline prevails.

This analysis synthesizes publicly available data including recent quarterly disclosures [N1][N2][S1] alongside third-party commentary relevant through early 2026. It aims to provide detailed contextual understanding without offering investment recommendations or price forecasts.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments