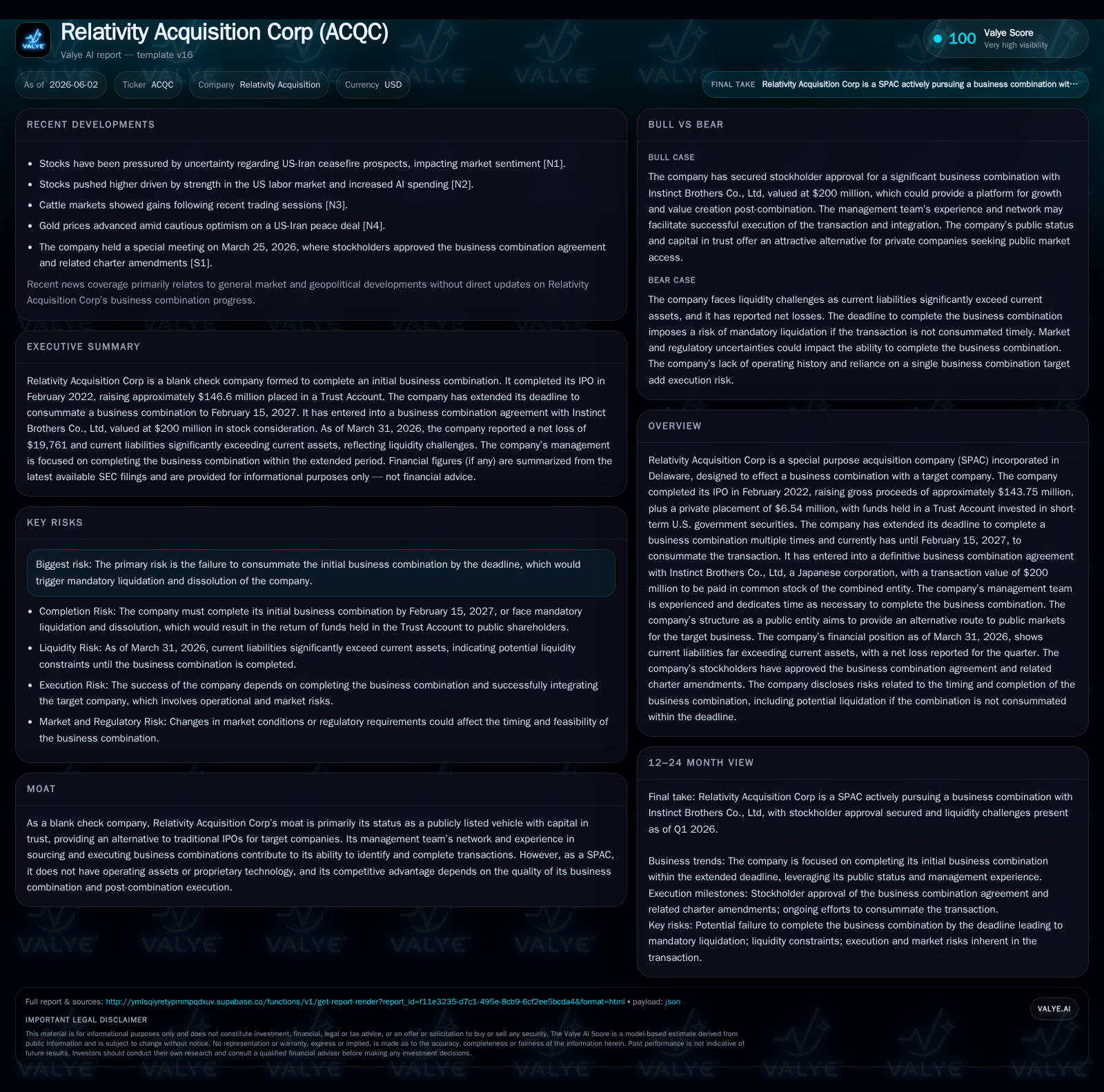

Relativity Acquisition Corp: Evaluating Its Path Forward Amid Mandated Deadlines

The recent quarterly filing reveals a deadline extension for Relativity Acquisition Corp’s business combination alongside notable redemption activity and contingent liability considerations.

Relativity Acquisition Corp (ACQC) extended its window to finalize a business combination until February 15, 2027, following shareholder redemptions that have meaningfully drawn down its Trust Account funds. The company now faces execution risk as it pursues completion of an acquisition of Mazaii Corp Ltd., with management emphasizing compliance and operational readiness despite founder turnover. Given the declining cash held in trust and contingent liability recognition under ASC 450, the SPAC’s strategic path centers on securing shareholder support for amendments and closing the merger within the revised timeline.

Quarterly Operating Update: Extended Deadline and Redemption Activity

In its most recent quarterly report dated June 2, 2026 [S2], Relativity Acquisition Corp disclosed an extension of the deadline for completing its initial business combination. Originally set for February 15, 2024, this "Combination Period" has now been extended to February 15, 2025, affording the company one additional year to finalize a qualifying transaction. This extension follows prior deadline pushes typical within the SPAC lifecycle.

On February 13, 2024, over 90,000 public shares were redeemed at a price approximating $11.32 per share, totaling around $1.02 million withdrawn from the Trust Account [S2]. These redemptions have depleted the Trust Account's liquidity to approximately $712,789 as of March 31, 2026 [S2].

Furthermore, management changes include the resignation of Mr. John Anthony Quelch as of March 27, 2024 [S2]. The filing explicitly notes that his departure was not due to discord concerning company operations or policies, leaving management continuity intact but spotlighting governance transitions during a critical phase.

The SPAC has also advanced deal execution with a non-binding Letter of Intent (LOI) executed on July 11, 2024, targeting an acquisition of Mazaii Corp Ltd., a Canadian entity undergoing reorganization [S2]. This agreement signals active deal sourcing and negotiation progress amidst the tightening timeframe.

Additionally, the company reassessed its contingent liabilities under ASC Topic 450 related to stock redemptions contingent on deal closing success [S2]. Given ongoing uncertainties surrounding consummation timing and shareholder votes, management concluded it is probable that contingent liabilities exist warranting accounting recognition at quarter-end.

Relativity Acquisition Corp’s SPAC Business Model Delineated

Relativity Acquisition Corp operates as a traditional Special Purpose Acquisition Company (SPAC) designed solely as a vehicle to merge with a target private entity and thereby bring it public without a conventional IPO route [S1]. The company filed its IPO in February 2022 raising gross proceeds near $143.75 million plus an additional private placement of approximately $6.54 million [S1]. These proceeds were placed into a segregated Trust Account invested conservatively in short-term U.S. government securities.

Key to ACQC’s model is that it holds no operating business or proprietary assets pre-merger; value hinges entirely on successfully closing a timely business combination. Shareholders have redemption rights allowing exit before close if unsatisfied with merger terms or prospects — creating dual pressures on liquidity and execution speed.

The Sponsor group and senior management team bring experience in sourcing and effecting deals but depend heavily on market sentiment and regulatory approvals to shepherd transactions through complex governance hurdles such as shareholder votes and certificate amendments [S1].

As typical among blank check companies in this cycle, ACQC has had to extend deadline milestones multiple times due to market conditions and transaction pacing challenges common in late-stage SPACs facing investor skepticism amid redemptions [S2].

Trust Account Dynamics and Implications for Stakeholders

One critical sector-specific KPI shaping Relativity Acquisition Corp’s near-term outlook is its Trust Account balance trajectory relative to redemption exercise dynamics. From initial gross proceeds exceeding $146 million at IPO completion in early 2022 [S2], cash held in trust has been systematically drawn down by mandatory redemptions triggered annually or at deal proximate voting windows.

As of March 31, 2026—the latest reported quarter—the cash remaining in the Trust Account was approximately $712,789 [S2], representing a significant depletion from initial IPO funds. Redemption payouts since mid-2024 account for most of this depletion; these are functionally refunds pro rata against the trust pool per public share redemptions.

This erosion materially constrains residual capital immediately available to finance transaction costs or backstop obligations post-combination. It also embodies a significant operational leverage point: the fewer public shareholders electing redemption going forward will influence not only transaction feasibility but also post-deal equity distribution stability.

Complementarily, examination of current balance sheet metrics underscores liquidity pressure inherent in this stage—$14,247 in current assets contrasts sharply with $3.4 million in current liabilities largely encompassing repayment obligations tied to redeemed shares [F1]

Industry Context: SPAC Mechanics and Regulatory Environment

SPACs operate within rigid statutory timelines imposed under SEC guidelines and Delaware corporate law mandating liquidation absent executed business combinations within prescribed windows typically ranging from two to three years post-IPO [S1]. Extensions require attestation from shareholders or board actions enabling few levers beyond negotiated calendar prolongations.

Amid evolving regulatory scrutiny—particularly focused on safeguarding investor capital during extended durations—Relativity Acquisition Corp filed proposals aimed at eliminating residual net tangible asset requirements post-business combination [S3]. Such amendments reflect wider industry debate balancing minimal asset thresholds against increased flexibility needed as SPAC structures mature.

Accounting standards codified under ASC Topic 450 govern contingent liabilities related to possible losses from unsuccessful mergers or redemption spikes. These provisions compel periodic reassessment with recognition thresholds varying from remote through probable scenarios based on deal progress signals.

This regulatory ecosystem frames both operational cadence and financial statement presentation strategies across all active SPACs navigating volatile capital markets while seeking transaction consummation amid often skeptical investors.

Growth Drivers Linked to Successful Business Combination Closure

Growth for ACQC hinges predominantly on executing its proposed transaction with Mazaii Corp Ltd., formalized via a non-binding LOI in mid-2024 [S2]. This step represents tangible forward movement away from mere shell status towards an operating public entity offering.

Extended deadlines provide critical runway enabling thorough due diligence, negotiation depth expansions, and scheduling logistics accommodating shareholder voting cycles while managing evolving market conditions.

Sponsor experience and network relationships stand as crucial enablers here since effectively sourcing quality targets that justify extended launch timelines differentiates successful SPAC outcomes from liquidations common when deals falter or valuations deteriorate [S1]

Completion will unlock avenues for incremental capital deployment fostering business scaling via operational investments post-merger—a pivotal enabler transforming dormant trust reserves into growth capital driving fundamental valuation realization.

Risks Surrounding Deal Completion and Shareholder Redemptions

The paramount risk confronting Relativity Acquisition Corp remains failure to consummate an initial business combination by February 15, 2025 [S2], which would mandate immediate liquidation dissolving value below invested levels.

Heightened shareholder redemption levels exacerbate this vulnerability by draining necessary liquidity potentially deterring counterparties concerned about post-deal float size or equity scarcity impacting market appetite.

ASC 450 contingent liability recording signals management prudence acknowledging increasing likelihood that failure scenarios must be financially reserved against—a stark reminder for stakeholders regarding material uncertainty embedded in forward prospects absent clear transactional closure proof points [S2].

Further complicating risk calculus is evolving governance proposal uncertainty; failure to secure requisite votes eliminating minimum tangible asset thresholds could stall merger completion triggering cascading negative outcomes including reputational damage and higher sponsor forfeiture costs [S3].

What to Monitor Next: Approvals, Amendments, and Market Signals

Attention now centers on several upcoming milestones carrying disproportionate impact for validating strategic direction:

- A forthcoming stockholder vote on propositions including eliminating net tangible asset retention obligations germane to streamlined merger facilitation [S3].

- Progress updates regarding definitive agreements transitioning beyond LOI with Mazaii Corp Ltd., particularly clear indications on pricing mechanism finalization or equity structure provisioning.

- Quarterly disclosures updating contingent liability assessments reflecting evolving merger odds framed under ASC450 accounting criteria.

- Market reception expressed via redemption rates proximate to voting windows scrutinizing sponsor credibility versus investor confidence.

- Sponsor communications clarifying any additional operational changes such as directorship shifts ensuring governance stability amidst execution phases. Monitoring these will deliver measurable signals serving as leading indicators distinguishing between achievable strategic milestones versus potential abortive outcomes intrinsic within late-cycle SPACs.

Synopsis of Financial Position: Liquidity Status Post-Redemptions

Relativity Acquisition Corp’s latest financial snapshot depicts a stark disparity between initial trust fund accumulation following IPO completion near $146 million in early 2022 [S2] versus nominal cash balances just above $700 thousand reported by Q1 2026 quarter-end [S2]. This decline is primarily attributable to executed public share redemptions reducing net available funds integral for financing transaction costs associated with proposed acquisitions.

Current liabilities outpace assets significantly; liabilities numbering roughly $3.4 million incorporate expected cash outflows linked with obligations toward redeeming shareholders rendering short-term liquidity strained absent external funding or successful merger finalization [F1]. Total debt remains negligible reflecting reliance primarily on internally generated resources combined with trust account mechanisms rather than external borrowings [F1].

In sum, ACQC faces a clear imperative: successfully consummate its targeted business combination promptly within outlined extensions or face forced dissolution resulting in limited recovery beyond funds returned through trust mechanisms less transactional costs incurred thus far.

This analysis summarizes key operating developments extracted from recent SEC filings without conjecture beyond disclosed facts. No investment advice or research views are provided herein. Readers should consider all publicly filed documents alongside market conditions before formulating views on Relativity Acquisition Corp's prospects.

Financial position in context

Current assets of $14,247 and current liabilities of approximately $3.4 million imply a current ratio near zero for 2026-03-31 [F1]

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments