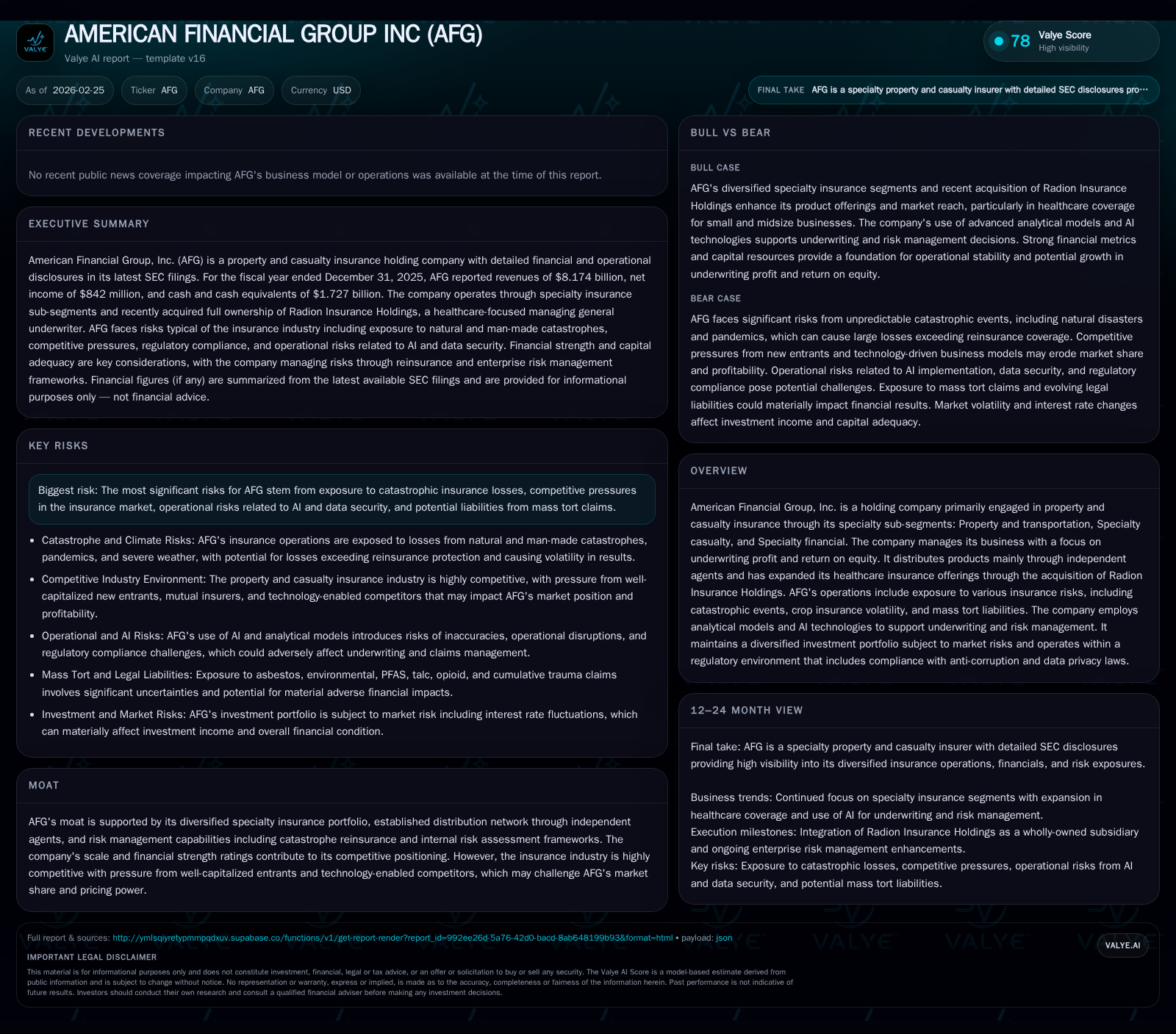

American Financial Group’s Steady Profits and Strategic Risk Mitigation Define Its Outlook

AFG’s underwriting-focused specialty insurance business and disciplined capital management underpin consistent profitability amid escalating catastrophe and regulatory challenges.

American Financial Group posted modest revenue contraction in 2025 following steady growth since 2022, reflecting shifts in premium volumes but supported by its strong independent agent distribution network. Operating income softened slightly, pressured by catastrophe-related claims and investment volatility, yet the company sustained underwriting discipline and risk-adjusted returns. Strategic adoption of AI-enhanced risk analytics aims to strengthen underwriting precision while mitigating emerging operational risks. Dividend payments remain solidly covered by cash flows, with cautious share repurchases resuming, signaling prudent capital allocation. Future growth hinges on expanding specialty healthcare insurance through Radion acquisition alongside evolving competitive and regulatory landscapes.

From Solid Premium Growth to Recent Volume Shifts: AFG’s Revenue Trajectory

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 8.2 | 842 | 1533 | 1073 | -1.8% | -5.1% |

| 2024 | 8.3 | 887 | 1152 | 1124 | +6.3% | +4.1% |

| 2023 | 7.8 | 852 | 1970 | 1073 | +11.2% | -5.1% |

| 2022 | 7.0 | 898 | 1153 | 1123 |

Source: SEC companyfacts cache [F1].

Note: Some line items are omitted where multi-year comparability is limited in the structured SEC XBRL dataset; trend columns are shown only when comparable history exists.

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | ROE% |

|---|---|---|---|

| 2025 | 606 | 99 | 17.5 |

| 2024 | 788 | 0 | 19.9 |

| 2023 | 684 | 213 | 20.0 |

| 2022 | 1213 | 11 | 22.2 |

Source: SEC companyfacts cache [F1].

American Financial Group’s revenue trajectory since 2022 demonstrates consistent expansion of its specialty property and casualty insurance lines before facing a mild contraction in 2025. Revenues rose from $7.04 billion in FY2022 to $8.32 billion in FY2024, reflecting the strength of its independent agent distribution network which remains central to AFG’s go-to-market strategy as referenced in both filings and news reports [F1], [N4], [N5], [S14]. This network enables penetration across Specialty sub-segments — Property & Transportation, Specialty Casualty, and Specialty Financial — helping maintain underwriting scale despite a competitive marketplace.

In FY2025, total revenues edged down modestly by 1.8% year-over-year to $8.17 billion [F1]. This reflects the cyclical nature of P&C insurance premiums amid fluctuating market conditions, including selective underwriting actions to mitigate risk exposures as detailed in regulatory filings [S5]. Such moderation aligns with broader industry trends reported by peers such as Brighthouse Financial and Everest that experienced premium volume softness or revenue pitfalls in Q4 results released around the same period [N1], [N2]. Compared with these peers’ top-line pressures, AFG’s resilience owes partly to its balanced specialty portfolio catering to niche segments less prone to commoditization.

Underwriting Profitability as the Cornerstone: Dissecting Operating Income Trends

Operating income — a key barometer for underwriting discipline — remained relatively stable from FY2022 through FY2023 (around $1.07–$1.12 billion) before declining slightly by approximately 4.5% in FY2025 to $1.07 billion [F1]. The narrowing operating income margin stems largely from elevated loss experience due to natural disasters and resultant claims severity impacting catastrophe lines within property and transportation products [S1], along with deliberate reinsurance expenditure increases aimed at capping risk retention exposure [S12].

Despite these headwinds, AFG sustained an underwriting profit-centric approach; expense ratios held firm as cost management efforts supplemented pricing adjustments for loss cost inflation evident across US insurers during recent quarters [N6], [S10]. A healthy operating ratio is sustained partly through judicious retention limits buttressed by traditional catastrophe reinsurance contracts complemented by fully collateralized catastrophe bonds — providing multi-layered financial protection from severe events posing outsized claims burdens [S1], [S26]. This layered risk transfer strategy is crucial given the heightened unpredictability of weather-related losses magnified by climate change trends.

Managing Catastrophe Risks and Regulatory Weight: Critical Challenges Ahead

Catastrophic events loom as the dominant risk driver for AFG’s underwriting results given their frequency and potential severity spikes caused by climate volatility or geopolitical unrest including terrorism risks highlighted under TRIP coverage frameworks expiring end-2027 [S1], [S26]. Losses from hurricanes or convective storms can affect both property damage and liability exposures contemporaneously—amplifying claims payouts unpredictably within reporting periods.

Beyond catastrophes, crop insurance volatility tied closely to weather anomalies introduces earnings variability; droughts or floods alter yield assumptions while commodity price swings influenced by evolving government policies add further complexity [S5], [S7]. Mass tort liabilities persist as material exposures stemming from historical asbestos/environmental claims plus emerging issues linked to substances like PFAS, talc or opioids that bring protracted litigation risk with an uncertain reserve horizon requiring rigorous actuarial estimation updates periodically reported by management assessments [S8], [S16].

AFG must also grapple with intensifying regulatory scrutiny around AI use within underwriting frameworks—balancing innovation against compliance costs related to privacy laws (CCPA/CPRA/NYS DFS regulations), cybersecurity mandates, and potential legislative changes extending insurer liability for AI-driven decisions or proprietary data mishandling (EU GDPR or U.S.-based expansions) [S6], [S18], [S26]. Failure to anticipate constraints or breaches could precipitate reputational harm and legal exposures.

Investing in AI and Analytics: Enhancing Risk Models Without Losing Prudence

Recognizing the rising intricacy of specialty risks and competition pressures from tech-enabled entrants, AFG has embedded AI-powered analytical models into its underwriting process aiming for improved risk selection accuracy while automating routine tasks noted both in company overview commentary and recent earnings disclosures highlighting technological investments benefiting operational efficiency gains without compromising prudency thresholds [N4], [S6], [S18].

However, reliance on AI systems entails inherent challenges including output bias risks, data quality concerns, oversight governance gaps, cyber intrusion vectors heightened against machine learning platforms plus ethical considerations around opaque algorithmic decisions affecting policy terms or claim adjudications that may prompt customer or regulator pushback. Continuous enhancements of governance frameworks alongside augmented internal audit controls are described as critical mitigants within AFG’s enterprise risk management discussions ensuring AI adoption augments rather than undermines sustainable profitable growth trajectories.

Evaluating Dividend Safety and Capital Returns Amid Profit Volatility

American Financial’s cash flow profile displays notable strength despite net income softness: operating cash flow surged over 33% year-over-year reaching $1.53 billion in FY2025 indicative of solid underlying business liquidity supporting capital deployment strategies even amid transient earnings pressure from catastrophe losses or investment market volatility noted during earnings commentary sessions [F1], [S24].

Dividend distributions have remained resilient at $606 million paid out in 2025 versus higher levels seen previously ($788 million in 2024), reflecting conservative payout ratio adjustments preserving balance sheet flexibility without sacrificing shareholder return appeal—augmented recently by special dividends declared alongside Q4 earnings beats reaffirming confidence in free cash generation stability amid earnings swings ([N4],[N9]).

Share repurchases resumed cautiously with about $99 million deployed after no buybacks occurred in 2024 signaling disciplined capital stewardship prioritizing reinvestment into business resilience while opportunistically addressing valuation inefficiencies under new repurchase authorization approved through decade-end 2030 cycle per SEC filings outlining long-term capital return framework consistency ([F1],[S24]).

The approximate ROE calculation using net income against shareholder equity at around 17.5% suggests an efficient leverage of equity capital emphasizing AFG’s capacity to generate above-average returns typical of focused specialty insurance operations balancing risk adjusted margins against capital requirements effectively.

Gauging Future Prospects: Sector Dynamics, Acquisition Impact, and Earnings Drivers

Looking forward, growth vectors largely hinge on broadening specialty healthcare insurance offerings following AFG’s full acquisition of Radion Insurance Holdings—an MGA specializing in small and mid-sized business healthcare coverage acquired for $7 million cash increasing product diversification beyond core P&C niches ([S17]). This strategic move positions AFG advantageously within growing healthcare markets distinctly separate from traditional casualty volatility thereby creating cross-selling possibilities leveraging Radion’s expertise alongside existing agent networks.

Analyst initiation observations from Wells Fargo emphasize constructive perspectives reflecting synergy potential alongside robust dividend safety rankings generating positive sentiment amongst institutional investors looking past transient cyclicality amid ongoing macroeconomic uncertainties ([N13],[N9]).

Nevertheless, competitive intensity fueled by well-funded incumbents plus emerging insurtech entrants applying sophisticated technology stacks continues to pressure pricing power necessitating continued underwriting rigor supported by proprietary models refined via AI integration ([N12],[S10]). How well AFG balances innovation velocity against prudent risk appetite will critically influence medium-term operating outcomes.

What to Watch Next: Market Signals, Regulatory Changes, and Competitive Pressures

Heading into subsequent quarters investors should track frequency and impact trends regarding natural catastrophes which materially influence underlying loss ratios reported historically ([N7],[S7]). Key regulatory developments concerning emerging state and federal oversight frameworks on AI implementation protocols could introduce compliance cost variability or operational restrictions impacting efficiency curves ([N12],[S6],[S26]).

Peer insurers’ Q4 earnings announcements collectively confirm cyclicality heightening attention towards expense containment effectiveness plus reinsurance market dynamics shaping cost structures essential for maintaining favorable combined ratios ([N1],[N2],[N3]). Finally monitoring retention rates within independent agency segments alongside any shifts toward direct-to-consumer channels will provide insights into competitive positioning durability for AFG’s traditional distribution model ([S10]).

This analysis is intended for informational purposes only reflecting currently available public financial data and disclosures without expressing an investment recommendation. Market conditions can evolve rapidly; readers should consult professional advisors before making any financial decisions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments