Aflac Inc's 2025 Earnings Drop: Evaluating Growth Drivers and Capital Strategy

Aflac faced a notable earnings decline in 2025 amid investment income headwinds and ongoing technology investments, challenging its growth trajectory and capital deployment decisions.

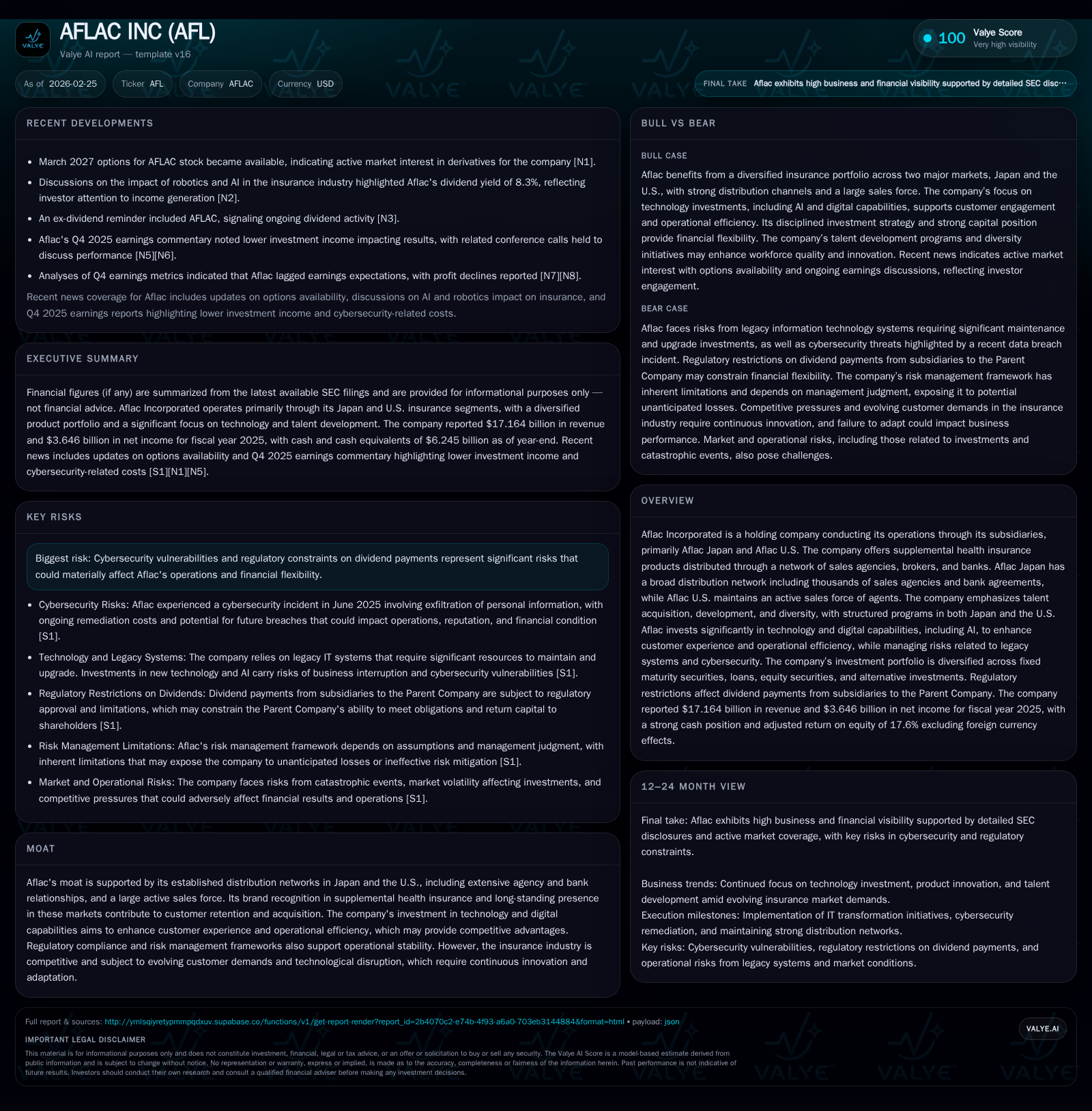

Aflac Inc reported a significant 9.3% decrease in revenue in 2025 alongside a 33% drop in net income, primarily driven by lower investment returns and operational challenges. The firm’s core Japan segment remains the principal earnings contributor but contends with persistency and morbidity pressures. Investments in digital transformation, including AI adoption, seek to enhance operational efficiency but introduce cybersecurity risks amid legacy systems vulnerabilities. Regulatory constraints, especially on dividend payments and evolving data privacy standards, limit financial flexibility. Capital allocation favored increased share repurchases over dividends, with returns on equity moderating around 12.4%. Talent development initiatives underpin Aflac’s strategy to sustain competitiveness within supplemental health insurance markets.

Financial Performance Decline in 2025: Revenue, Operating Income, and Net Income Trends

In fiscal year 2025, Aflac Incorporated experienced a marked decline in key financial metrics underpinning its consolidated results. Total revenues contracted by approximately 9.3% year-over-year to $17.16 billion, down from $18.93 billion in 2024 [F1]. Net income dropped sharply by roughly one-third (33%) reaching $3.65 billion compared with $5.44 billion the prior year [F1]. This contraction reflects significant pressures stemming chiefly from lower investment income within Aflac’s portfolio, a critical component given the company’s business model's reliance on robust fixed maturity and loan asset yields [N2][S1]. Operating cash flow also receded by about 5.6%, indicating some squeeze on core operating liquidity despite sustained underwriting activities [F1].

The drop echoes management commentary attributing earnings softness particularly to unfavorable market interest rates impacting portfolio yields alongside elevated credit spread volatility that trimmed fixed income returns [N2][S1]. Given that invested assets underpin claims-paying ability and profit margins through the return on average invested assets metric – a staple insurer profitability lever – these investment headwinds weighed heavily on results.

Financial Summary Table: Aflac Inc Historical Financials (FY2019–FY2025)

Historical performance (annual)

| FY | Rev ($bn) | Net ($bn) | CFO ($bn) | Rev YoY | Net YoY |

|---|---|---|---|---|---|

| 2025 | 17.2 | 3.6 | 2.6 | -9.3% | -33.0% |

| 2024 | 18.9 | 5.4 | 2.7 | +401.1% | +16.8% |

| 2023 | 3.8 | 4.7 | 3.2 | -80.6% | +10.9% |

| 2022 | 19.5 | 4.2 | 3.9 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): OpInc, Capex, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($bn) | ROE% |

|---|---|---|---|

| 2025 | 1198 | 3.5 | 12.4 |

| 2024 | 1087 | 2.8 | 20.9 |

| 2023 | 966 | 2.8 | 21.2 |

| 2022 | 979 | 2.4 | 18.8 |

Source: SEC companyfacts cache [F1]. 12.4%

*Note: The FY2023 revenue is an anomalous figure possibly impacted by accounting or reporting changes and thus omitted from YoY calculations. Note: Operating income YoY % available only through FY2023 Q3 per latest data.

Segment Dynamics: Aflac Japan and U.S. Contributions to Profitability Shifts

Aflac's two principal operating segments—Aflac Japan and Aflac U.S.—contribute unevenly to consolidated profitability profiles with significant dependence on the Japanese market [S1][S13][S16].

The Japan segment continues as the cornerstone of earnings generation due to its large scale distribution network encompassing thousands of independent agencies plus bank partnerships facilitating deep market penetration across demographics [S16]. However, this segment grappled with headwinds including morbidity rate variances affecting claim frequencies and persistent premium persistency challenges known in supplemental health insurance lines that impact renewal revenue quality [S16]. Expenses tied to administering these large agent networks coupled with competitive pressures further constrained margin expansion.

Meanwhile, the U.S. segment maintains an active independent agent salesforce that accounts for modest growth prospects but still trails behind Japan’s scale [S13]. The U.S.'s supplemental coverage plans contend with evolving employer demands emphasizing comprehensive benefits portfolios from fewer carriers—a dynamic reshaping product bundling strategies that Aflac must address proactively.

This geographic segmentation manifests not only in underwriting trends but also investment yield differentials between currencies impacting reported results after reflecting foreign exchange adjustments essential for true economic performance appraisal [S22].

Investments in Technology and Digital Transformation: Balancing Efficiency with Risk

Aflac has embarked on accelerated initiatives deploying advanced technologies including artificial intelligence (AI) aiming to elevate customer experience while streamlining analog-heavy processes historically embedded within insurance operations [S25]. This includes bolstering underwriting analytics precision via machine learning models and automating claims adjudication workflows to reduce processing times.

Nonetheless, transitioning away from legacy IT systems presents a dual-edged challenge: high modernization costs along with exposure risks linked to integrating new platforms alongside older infrastructure remnants prone to failures if not properly harmonized [S25]. Such system gaps can expose core operations to disruptions detrimental to policyholder servicing.

Moreover, the company acknowledges that incorporating AI-driven processes increases cybersecurity risk vectors—potentially complicating detection or mitigation efforts given newer threat modalities leveraging similar AI tools adversarially [S25]. Mitigating these vulnerabilities demands continuous investments in cybersecurity defenses beyond traditional perimeter protections.

Regulatory Environment and Cybersecurity Threats as Operational Constraints

The complex regulatory frameworks governing Aflac's operations across jurisdictions impose stringent constraints especially regarding dividend distributions—where Japanese FSA rules restrict repatriation unless specific capitalization thresholds are met—curtailing Parent Company's cash flexibility despite strong subsidiary earnings capacity [S18]. Additionally, Nebraska Insurance Department regulations enforce limits tied to statutory capital influencing intercompany fund transfers vital for debt servicing.

Cybersecurity emerges as a salient operational risk following a material June 2025 data breach incident entailing unauthorized exfiltration of sensitive personal information pertaining predominantly to U.S.-based customers and agents [S10][S18][N2]. Remediation efforts involve substantial costs encompassing credit monitoring services provisioning plus handling regulatory investigations potentially culminating in fines or litigation exposure.

Furthermore, heightened regulatory requirements around data privacy laws such as APPI in Japan and various state-level mandates in the U.S., combined with evolving global compliance expectations related to cloud adoption strategies amplify compliance overheads considerably [S24].

Outlook Considerations: What the Company Signals for Future Growth

Management commentary highlights cautious optimism centered around stabilizing premium sales trajectories post-earnings miss accompanied by anticipated improvement in investment yields contingent upon normalization of fixed income markets dynamics [N3][N2][S1]. Growth levers include leveraging talent-driven innovation targeting product diversification aimed at holistic employer benefit solutions particularly within the U.S..

However, significant uncertainty stems from regulatory developments potentially altering agent classification frameworks threatening cost structures especially given independent agent predominance in distribution model [S7] plus ongoing cyber risk evolution necessitating vigilant capital allocation toward protective infrastructure rather than purely growth enablers.

Investors should monitor quarterly premium persistency metrics closely alongside indicators of successful AI deployments translating into cost savings without compromising customer service quality as key barometers signaling green shoots.

Capital Allocation Review: Dividends, Share Repurchases, and ROE Implications

Despite headwinds reducing net income by a third in fiscal 2025 relative to prior year levels [F1], Aflac maintained shareholder distributions via dividends totaling approximately $1.20 billion—up modestly versus $1.09 billion paid in fiscal year 2024—and significantly ramped common stock repurchases reaching approximately $3.53 billion last year compared with $2.8 billion previously [F1][S12][S14].

Such aggressive buyback activity indicates strategic prioritization toward bolstering per-share intrinsic value amid share price volatility compounded by sector cyclicality factors.

Return on equity correspondingly softened from elevated mid-teens levels recorded earlier to near-term steady-state around 12.4%, reflecting normalized profit cycles combined with balance sheet management converging toward optimal capital efficiency ranges consistent with regulated insurance entities seeking stable rather than peak ROEs [F1][S22].

Absent formal guidance updates beyond current disclosures, market participants should scrutinize capital allocation policies especially regarding dividend flexibility within Japanese-regulated subsidiaries alongside potential volatility linked to unrealized foreign currency translation adjustments materially affecting comprehensive earnings measures.

Talent Development and Corporate Culture as Foundations for Sustained Competitiveness

Recognizing human capital as fundamental differentiator within insurance agency-heavy models representing core customer acquisition engines presents a strategic imperative at Aflac.

In Japan, initiatives like the newly launched Aflac Leadership Academy provide structured leadership training aimed at cultivating next-generation managerial expertise ensuring succession strength within rapidly aging workforce demographics [S1]. The company’s human capital management system offers transparency around job competencies fostering career path planning ecosystem enhancing employee engagement.

In the United States counterpart operations emphasize collaborative partnerships with universities offering internships/co-op programs designed as talent pipelines while supporting continuing professional development enabling agents’ skill enhancement critical amid shifting sales techniques entwined with digital tools [S1].

Additionally, health & wellness certifications recognizing progressive internal efforts showcase commitment toward sustaining workforce productivity balanced against well-documented insurance sector challenges pertaining to burnout rates within high-pressure sales environments.

These human resource strategies represent indispensable pillars underpinning long-term adaptability essential for success amidst intensifying competition from both incumbents expanding product suites and emerging entrants leveraging insurtech innovations disrupting traditional supplemental health insurance paradigms.

Disclaimer: This analysis is based solely on publicly available information up to February 25th, 2026 and does not constitute investment advice or recommendations regarding AFLAC INC or its securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments