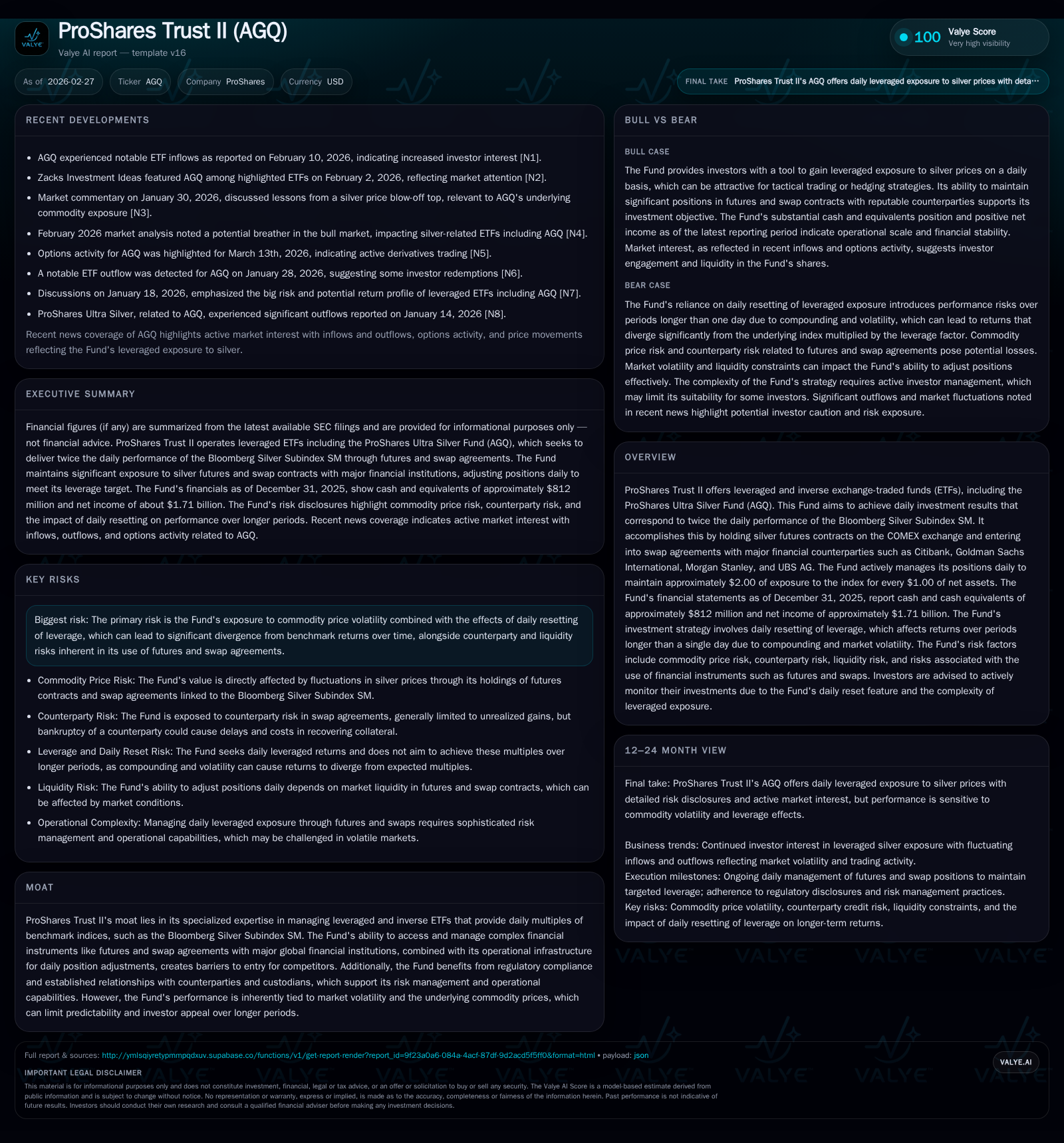

ProShares Trust II Defies Volatility with Ultra Silver Fund’s Surge in 2025

ProShares Trust II reversed prior years’ losses through leveraged silver ETF strategy, signaling operational resilience amidst complex derivatives and market volatility.

After consecutive years of substantial net losses, ProShares Trust II posted a dramatic net income turnaround to $1.71 billion in 2025. This shift is tightly linked to the performance of its ProShares Ultra Silver Fund (AGQ), which employs daily reset leveraging strategies involving COMEX silver futures and swap agreements with major financial counterparties. While operating cash flow turned negative in 2025, aggressive capital allocation via buybacks continued robustly, underpinning an approximate 30% return on equity. The fund’s future growth remains subject to volatile commodity prices, leverage effects over extended periods, and regulatory scrutiny on complex ETF products.

Exceptional Financial Reversal: A Look at Historical Performance

ProShares Trust II's financial performance over the past four years charts a trajectory from significant losses to a spectacular profit surge in fiscal year 2025. After enduring a net loss of approximately $2.48 billion in 2023 followed by a smaller loss of $39.4 million in 2024, the firm recorded an impressive net income of roughly $1.71 billion by the close of 2025 [F1]. This swing represents a staggering change exceeding +4,400% year-over-year.

Operating cash flow (CFO) presents a contrasting pattern. While positive at over $770 million in 2022 and again turning positive at about $209 million in 2024, CFO fell sharply to -$246 million by end-2025 [F1]. This divergence between profitability and cash flow underscores the complex realities tied to managing daily reset leverage positions within commodity futures and swaps portfolios.

Shareholders' equity experienced strong value appreciation from around $3.03 billion at end-2024 to approximately $5.72 billion by end-2025, more than doubling amid expanding fund AUM and elevated mark-to-market valuations [F1]. Concurrently, ProShares Trust II intensified its shareholder returns through share repurchases totaling nearly $13 billion in 2025—its highest annual level since at least 2022—reflecting confidence in capital management amid turbulent underlying asset volatility [F1].

Historical performance (annual)

| FY | Net ($bn) | CFO ($mm) | Net YoY |

|---|---|---|---|

| 2025 | 1.7 | -246 | +4448.1% |

| 2024 | -0.0 | 209 | +98.4% |

| 2023 | -2.5 | -1540 | -2690.7% |

| 2022 | 0.1 | 770 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($bn) | ROE% |

|---|---|---|

| 2025 | 13.0 | 29.9 |

| 2024 | 8.8 | -1.3 |

| 2023 | 9.2 | -75.6 |

| 2022 | 12.7 | 2.5 |

Source: SEC companyfacts cache [F1].

Note: All figures sourced from company filings [F1]. YoY % change reflects net income improvements across FY periods.

Mastering Leverage: ProShares Trust II's Investment Mechanics

At the heart of the turnaround is ProShares Ultra Silver Fund (ticker AGQ), which strives to deliver twice the daily investment result of the Bloomberg Silver Subindex SM through sophisticated leverage techniques [S1]. The Fund primarily achieves this via holding long positions in COMEX silver futures contracts alongside entering into total return swap agreements with prominent banking entities including Citibank, Goldman Sachs International, Morgan Stanley International PLC, and UBS AG [S1].

This approach entails maintaining approximately two dollars of index exposure for every dollar of net assets—a framework known as "daily reset leverage." The Fund dynamically adjusts these positions every trading day to ensure constant two-times exposure despite fluctuations in underlying silver prices or contract expirations [S1]. While this confers heightened sensitivity—and potential for amplified returns—it also induces intra- and inter-day volatility and creates complex path-dependency effects that complicate performance over multi-day or longer horizons.

Additionally, counterparty risk linked to swap agreements is carefully managed through collateralization practices held by third-party custodians; however residual risks remain if any counterparty defaults or declares bankruptcy, potentially delaying collateral recovery [S1][S7]. Such operational sophistication forms a moat as few competitors possess both access and expertise to coordinate futures contracts combined with multi-bank swap facilities while navigating regulatory monitoring.

Q4 2025 and Recent Market Activity: The Pulse of Investor Flows

Silver market volatility fueled marked investor interest fluctuations around AGQ during late 2025 into early 2026 [N11][N10]. The ETF reached new highs within its trading value early January but then underwent intermittent sizable outflows noted across January and February as per multiple market alerts reporting redemption surges [N10][N8][N1]. This ebb-and-flow reflects the sensitivity of leveraged commodity-linked ETFs to spot price swings.

Enhancing tradability for investors, AGQ options contracts started trading on April 10th, providing new tools for hedging or speculative strategies aligned with silver movements [N2]. These derivative offerings facilitate more nuanced risk positioning yet may also intensify trading complexity.

Investors actively utilized put and call options particularly around March expiration dates as evidenced by open interest data indicating substantial options volumes—further underscoring AGQ’s role as a focal point for leveraged silver exposure within public markets [N7][N9].

Constraints and Risks Shaping Future Growth Trajectory

Critical risks revolve around intrinsic properties of leveraged ETFs based on commodities like silver combined with regulatory environment uncertainties affecting complex securities.

Daily reset leverage inherently produces path dependency such that returns measured over periods longer than one day can deviate significantly from two times the underlying benchmark return due to compounding effects during volatile periods [S1]. This limits predictability for investors holding positions long-term.

Counterparty credit risk remains salient despite collateral safeguards since catastrophic counterparty failures might disrupt timely settlement of exposures within both futures custody accounts and swap balances [S7][S24]. Liquidity risk also exists if systemic episode-induced shocks impair market functioning.

Regulatory scrutiny has intensified post-2022 with FINRA soliciting comment on possible restrictions or prohibitions around retail access to "complex products"—potentially encompassing funds like AGQ due to their leverage structure [S4][S23]. While uncertain at this stage, any enactment could constrain demand or require alteration in product marketing/distribution.

Moreover, external factors such as trade disputes or macroeconomic shifts impacting USD exchange rates or global commodity supply chains introduce additional layers of uncertainty given silver pricing dependence on broader metal demand fundamentals [S5][S23].

Capital Allocation Strategy: Buybacks, Cash Flow, and Return on Equity

Despite operating cash flow being negative in fiscal year 2025 (-$246 million), ProShares Trust II conducted substantial share repurchases amounting to approximately $13 billion—the peak among recent years—indicating an assertive capital return focus during periods coinciding with substantial profitability spikes [F1][S12]. This aggressive buyback activity notably exceeds typical industry norms for leveraged ETF issuers where liquidity management usually counsels caution.

Return on equity (ROE), capturing net income relative to shareholders’ equity at about a near-30% rate given reported figures ($1.71 billion net income over ~$5.72 billion equity), reflects high profitability efficiency but must be interpreted alongside inherent volatility risks associated with underlying assets [F1].

Such capital deployment dynamics suggest strategic intent to enhance shareholder value through scaling back share count during favorable market phases while managing liquidity buffers necessary for derivative margin calls and resetting obligations under futures/swap instruments [S12][S7]. Dividend payments are not material components per filings; emphasis remains on buybacks coupled with maintaining adequate cash equivalents exceeding $800 million historically for operational flexibility [F1][S10].

What Investors Should Watch: Market Dynamics and Regulatory Developments

Looking forward, key inflection points include:

- Continued high volatility in silver prices driven by macroeconomic cycles, demand-supply imbalances, geopolitical tensions affecting precious metals demand;

- Monitoring regulatory developments stemming from FINRA proposals regarding retail accessibility rules for leveraged/inverse ETFs classed as 'complex products,' which could reshape market structures affecting ProShares' offerings;

- Evolving investor participation patterns reflected through options market activity enhancing liquidity but potentially increasing short-term speculative pressures;

- Counterparty health metrics amid tightening credit conditions broadly impacting swap agreements conducted with large global financial institutions;

- Changes in methodology or pricing within benchmark indices like Bloomberg Silver Subindex SM influencing calculation bases for Fund exposure.

Absent explicit guidance disclosed by management or regulatory bodies beyond risk disclosures at present, these thematic elements constitute pivotal areas whereby material impacts could emerge requiring attentive analysis by stakeholders [N2][S4].

Disclaimer: This analysis summarizes publicly available information relating to ProShares Trust II leveraging detailed SEC filings [F1], news reports [N#], and official statements without offering investment recommendations or forecasts beyond stated facts.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments