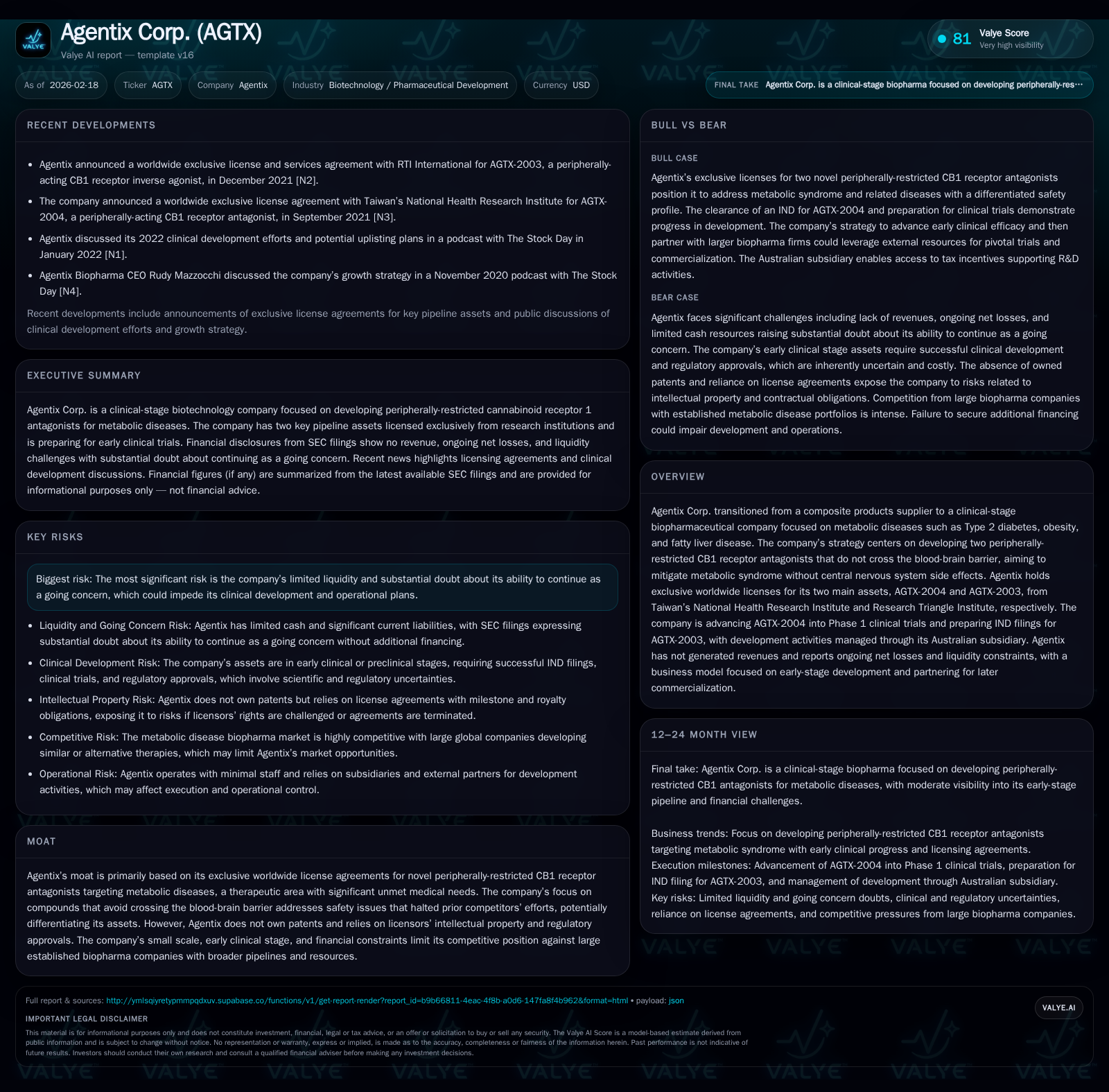

Agentix Corp.'s Transition to Clinical-Stage Biopharma Faces Critical Funding and Development Milestones

Agentix is advancing novel peripheral CB1 receptor antagonists for metabolic diseases while grappling with significant liquidity constraints.

Agentix Corp. has shifted from composite products manufacturing to clinical-stage biopharmaceutical development, focusing on peripherally-restricted CB1 receptor antagonists for conditions such as Type 2 diabetes and obesity. Despite exclusive worldwide licenses for promising compounds AGTX-2004 and AGTX-2003, the company remains pre-revenue, operating at net losses with fragile liquidity. Progress includes IND clearance and upcoming Phase 1 trials, yet ongoing cash flow deficits and high debt levels raise substantial doubt about its going concern status. Future growth hinges on successful clinical milestones and capital raises amid stiff competition and regulatory complexities in the biopharma space.

Company Evolution and Strategic Shift

Agentix Corp., originally engaged in composite product supply predominantly for oil and gas sectors, made a fundamental pivot beginning in mid-2020 when it acquired GSL Healthcare, Inc. This deal marked its entry into clinical-stage biopharmaceutical development focused on metabolic diseases like Type 2 diabetes mellitus (T2DM), obesity, and fatty liver disease [S1][S28]. This transition reflects a strategic repositioning toward innovative therapies aimed at addressing sizeable unmet medical needs within the metabolic syndrome domain.

The company’s central scientific thesis revolves around the cannabinoid receptor type 1 (CB1) as a therapeutic target. Unlike prior players including Pfizer and Merck whose candidates failed due to central nervous system-related toxicities caused by blood-brain barrier penetration, Agentix leverages compounds engineered to be peripherally restricted, minimizing CNS exposure [S18]. This approach holds promise for maintaining efficacy against key metabolic pathways like lipogenesis and insulin sensitivity without psychiatric side effects.

Pipeline Overview: AGTX-2004 and AGTX-2003

Agentix holds exclusive worldwide license rights for two core assets:

AGTX-2004 (DBPR211): Licensed from Taiwan's National Health Research Institute (NHRI) under a March 2021 agreement, this peripherally acting CB1 antagonist has completed preclinical efficacy and safety animal studies demonstrating favorable toxicology profiles without blood-brain barrier crossing [S8][S10][S18]. The company received FDA clearance of an Investigational New Drug (IND) application enabling planned Phase 1 dose-escalation safety trials, managed through its Australian subsidiary [S18].

AGTX-2003: Licensed from the Research Triangle Institute (RTI) in March 2020, this CB1 inverse agonist also exhibits peripheral restriction with preclinical evidence supporting efficacy in obesity and non-alcoholic fatty liver disease (NAFLD) models [S8][S18]. Current efforts emphasize completing enabling animal studies required before an IND filing.

Both programs operate under milestone-based license agreements requiring upfront fees, multiple development phase payments upon advancement (Phases I–III), regulatory approvals across jurisdictions (FDA, EMA, PMDA), plus royalties on sales [S8][S10]. These obligations signify substantial future financial commitments contingent on clinical success.

Historical Financial Performance

Agentix remains pre-revenue since pivoting into biotech—with no sales recorded from FY2020 through FY2023 [F1]. The transition phase is marked by sustained operational losses primarily due to R&D expenditures and administrative costs supporting early-stage clinical development:

Historical performance (annual)

| FY | Rev | Net ($mm) | CFO ($) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | -1 | -125078 | -1 | +3.1% | ||

| 2024 | -1 | -110429 | -1 | +57.4% | ||

| 2023 | 0 | -1 | -88541 | -1 | +40.0% | |

| 2022 | 0 | -2 | -1623 | -2 | -100.0% |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Capex, Div, Buybacks, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 18.3 |

| 2024 | 22.9 |

| 2023 | 61.1 |

| 2022 | 212.7 |

Source: SEC companyfacts cache [F1].

*Some expense details not fully available from filings.

Operating losses have improved approximately 31% year-over-year between FY2024 and FY2025 reflecting some operating leverage despite ongoing cash burn consistent with early-stage clinical development [F1][S16]. Professional fees increased alongside R&D consulting costs while general administrative expenses decreased notably due to lower royalty fee expenses compared to prior periods [S16].

Operating cash flow remains negative at roughly $125K annually underscoring persistent cash burn.

Balance Sheet and Liquidity Constraints

Current financial positioning reveals severe liquidity challenges threatening operational continuity:

- Cash & equivalents stood at approximately $4.5K as of March 31, 2025 worsening slightly to about $6.4K by December 31, 2025 based on latest interim reports [F1][S11][S2].

- Current liabilities exceeded $3.5 million at December 31, 2025 with related party payables forming the largest segment [F1][S26].

- Stockholders’ equity remains deeply negative at $(3.10) million as of FY2025 end indicating cumulative accumulated deficits since inception [F1][S26].

The company relies on mezzanine secured notes totaling up to $700K from Gray’s Peak Private Credit LLC bearing punitive interest rates starting at 7.5% monthly escalating if unpaid beyond specified periods [S6][S14]. These debt obligations exacerbate financial strain amid absent revenue streams.

Management discloses "substantial doubt" about ability to continue as a going concern absent timely capital infusion via equity or additional debt financing—both bearing risks of dilution or onerous terms [S11][S17]. No dividends or share repurchases have been made historically given cash constraints [S21].

Market Opportunity and Competitive Landscape Analysis

The global biopharmaceutical market targeting metabolic disorders remains robust driven by rising prevalence of diabetes and obesity worldwide along with increased acceptance of novel therapies [S12]. However, the sector is intensely competitive:

Industry incumbents include pharmaceutical heavyweights such as Novo Nordisk specializing in diabetes treatments; Sanofi and Eli Lilly developing complementary agents; Takeda advancing licenses for peripheral CB1 antibodies; plus smaller specialized companies like Inversago Pharma working on similar targets for rare disorders [S12][S18].

Agentix faces competitive risk compounded by lack of proprietary patent ownership—relying exclusively on licensed intellectual property—and regulatory scrutiny given historical failures of CB1 antagonists crossing the blood-brain barrier [S12][S18]. Regulatory oversight spans multi-phase clinical trials plus manufacturing compliance under GMP standards enforced by FDA and international agencies including EMA/PMDA [S10][S13].

Growth Prospects and Key Milestones Ahead

Critical near-term catalysts include:

- Completion of Phase 1 safety studies for AGTX-2004 currently planned which will inform feasibility for subsequent clinical phases.

- IND submissions for AGTX-2003 following completion of enabling animal studies executed by its Australian subsidiary.

- Fulfillment of licensing milestone payments tied to regulatory clearances which impose cash outflows but may unlock further financing opportunities.

- Securing sufficient additional funding—equity or debt—to sustain operations beyond initial clinical stages.

Absent these milestones or timely capital raises progress could stall given limited runway amid costly clinical trial requirements common among early-stage biotechs.

Capital Allocation and Returns Metrics

Agentix has not declared or paid dividends historically nor indicated plans for share buybacks due to ongoing cash limitations [S21]. Free cash flow remains negative driven primarily by operating expenses typical of R&D-focused entities without commercial revenues yet realized [F1].

Return metrics such as ROE are not meaningfully calculable given persistent negative stockholders’ equity; the firm reported an approximate ROE of +18% based on net income divided by negative equity figure but this is not indicative of profitable returns due to accounting deficit context [F1].

Risks Overview Highlighted in SEC Filings

Key risks outlined include:

- Liquidity Risk: Cash reserves are critically low necessitating urgent fundraising; failure risks business failure imminently.

- Clinical Development Risk: High attrition inherent in drug development; failure would materially impair asset values.

- Regulatory Risk: Complex multi-jurisdictional approvals involving costly compliance.

- Intellectual Property Dependency: Entirely reliant on licensed IP rather than owned patents introducing vulnerability.

- Competition: Larger pharma competitors possess deeper resources potentially outpacing Agentix’s assets.

- Operational Constraints: No full-time employees; reliance on contractors/directors limits operational agility.

- Financial Leverage: Debt bears punitive interest compounding financial burden absent revenues [S15][F1].

Conclusion: Balancing Innovation Ambition Against Commercial Realities

Agentix Corp’s strategic repositioning toward peripheral CB1 receptor blockade addresses a scientifically validated target implicated in widespread metabolic illnesses—a field marked by prior failures due to CNS toxicity concerns.

With two licensed assets progressing toward critical first-in-human trials but constrained by austere capital conditions featuring narrow runway and heavy debt burdens, Agentix faces pivotal execution challenges where securing non-dilutive financing or partnerships will be critical for survival amid intense competition.

Monitoring upcoming IND filings progressions especially Phase 1 trial commencements alongside announcements regarding financing activities will be essential indicators of viability moving forward.

Disclaimer: This analysis is based solely on available SEC filings and public data as of February 18, 2026. It does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments