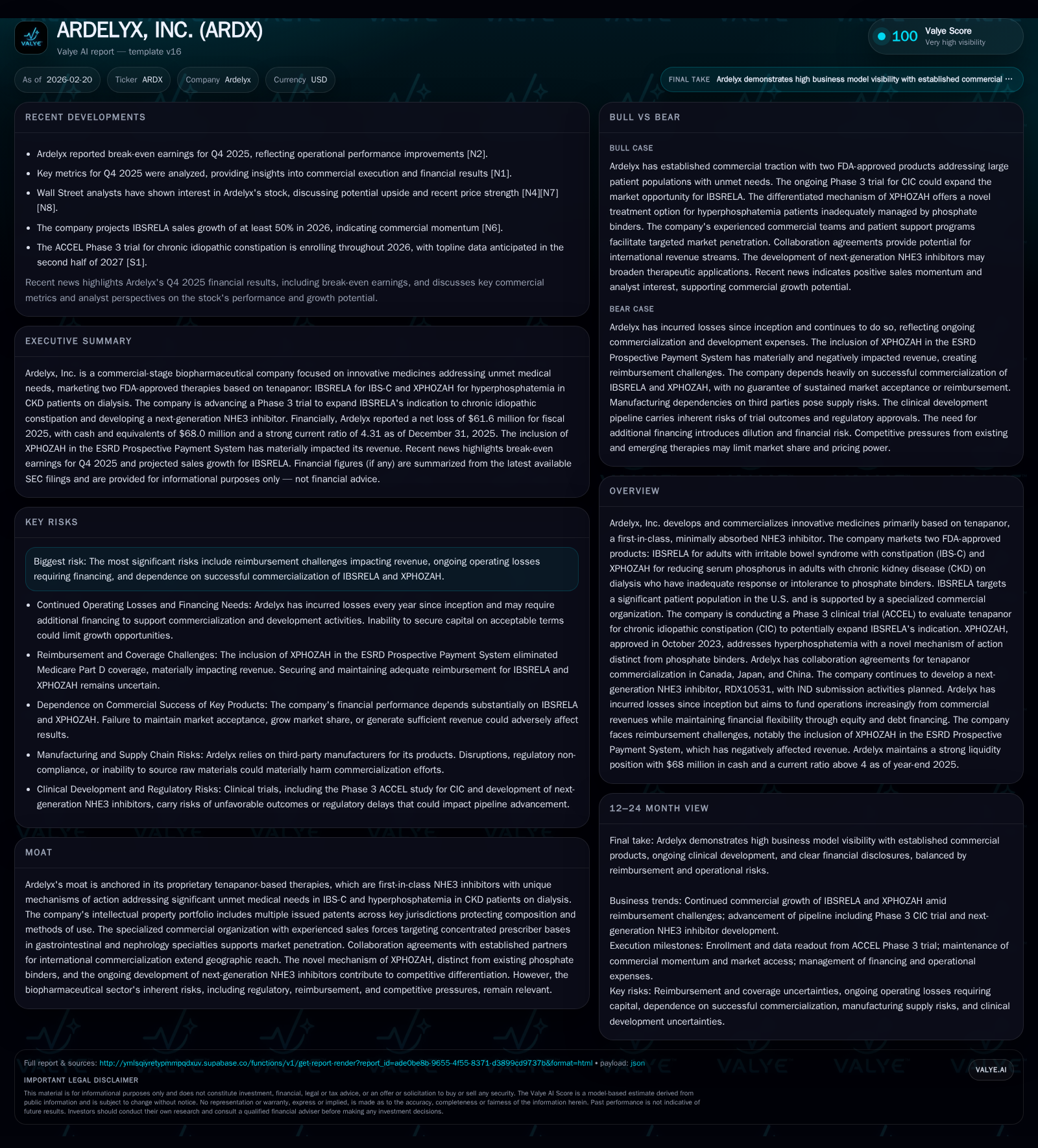

Ardelyx Advances NHE3 Inhibitors Amid Financial and Market Challenges

Focused commercialization of tenapanor-based therapies drives growth potential despite reimbursement and capital hurdles.

Ardelyx, Inc. centers its platform on tenapanor, a minimally absorbed sodium/hydrogen exchanger 3 (NHE3) inhibitor targeting IBS-C and hyperphosphatemia in CKD dialysis patients. Despite pipeline expansion efforts via the pivotal ACCEL Phase 3 trial for chronic idiopathic constipation (CIC), Ardelyx faces commercial challenges driven by Medicare reimbursement changes, notably XPHOZAH’s inclusion in the ESRD prospective payment system (PPS), which materially impacted revenue growth in 2025. The company continues to report operating losses, carries significant indebtedness with restrictive covenants, and depends on expanded coverage and market adoption to improve financial health. Key milestones include clinical data readouts and sales trajectory monitoring.

A Decade of Building a Novel Therapeutic Platform

Ardelyx’s foundation rests on tenapanor, a first-in-class, minimally absorbed sodium/hydrogen exchanger isoform 3 (NHE3) inhibitor localized on the apical surface of intestinal epithelial cells. This mechanism modulates sodium absorption influencing gut fluid dynamics without systemic exposure.

Two products derived from tenapanor have FDA approval: IBSRELA®, for adults with irritable bowel syndrome with constipation (IBS-C), and XPHOZAH®, to reduce serum phosphorus in adults with chronic kidney disease (CKD) on dialysis intolerant or inadequately responsive to phosphate binders. These therapies target sizeable U.S. populations—approximately 13 million adults affected by IBS-C symptoms inadequately controlled by existing treatments—and CKD dialysis patients facing hyperphosphatemia-related complications.

The company’s patent portfolio supports exclusivity across key jurisdictions. Commercial efforts deploy specialized sales teams targeting gastroenterology for IBSRELA and nephrology for XPHOZAH, supplemented by international licensing partnerships expanding reach beyond the U.S. [S1][S23][N7].

Revenue Trajectory and Recent Performance Drivers

Ardelyx’s revenue history reflects critical payer coverage inflections rather than purely volume-driven dynamics. Historical peak revenues reached approximately $301 million by FY2019 but fell precipitously thereafter due primarily to Medicare reimbursement policy shifts impacting XPHOZAH.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -62 | -42 | -41 | 1492000 | -57.4% |

| 2024 | -39 | -45 | -28 | 1011000 | +40.8% |

| 2023 | -66 | -90 | -63 | 344000 | +1.7% |

| 2022 | -67 | -70 | -64 | 55000 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Div, Buybacks. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -44 | -36.9 |

| 2024 | -46 | -22.6 |

| 2023 | -90 | -39.6 |

| 2022 | -70 | -68.3 |

Source: SEC companyfacts cache [F1].

Note: Post-2019 revenues collapsed mainly due to Medicare Part D exclusion of XPHOZAH following ESRD PPS inclusion effective January 2025; exact figures post-2019 not fully disclosed [F1].

The Medicare Part D exclusion removed standalone coverage for XPHOZAH as it became reimbursed within the ESRD PPS bundle starting January 1, 2025. This change materially constrained payor willingness to cover prescriptions separately.

Despite targeted sales initiatives supporting IBSRELA uptake, overall top-line momentum weakened substantially through FY2025 [F1][N1][S1][S2].

Market Access Challenges Impacting Growth Dynamics

Key challenges include:

- XPHOZAH's ESRD PPS inclusion removing Medicare Part D coverage from January 2025 onward.

- Variable commercial payor coverage requiring costly individual negotiations.

- Medicare Part D exclusion ripple effects adversely affecting patient affordability despite clinical needs.

These factors generate pricing pressure and acceptance uncertainty amid entrenched phosphate binder use despite efficacy gaps.

Healthcare reform legislation further complicates reimbursement outlooks with increased compliance costs related to pricing transparency rules [S1][S6][S7][N8].

Clinical Pipeline Expansion: ACCEL Phase 3 Trial and Beyond

The ACCEL Phase 3 trial aims to expand tenapanor indications into chronic idiopathic constipation (CIC), potentially broadening the addressable patient population significantly beyond IBS-C (~13 million adults). Positive results would enhance the IBSRELA franchise growth prospects [N8].

Ardelyx also pursues next-generation NHE3 inhibitors to sustain innovation leadership within this niche .

Financial Health: Capital Structure, Cash Flow, and Funding Needs

As of December 31, 2025:

- Cash and short-term investments totaled approximately $265 million.

- $200 million drawn under a $300 million loan facility subject to covenants restricting business changes or additional debt without lender consent.

- Operating cash flow remains negative at approximately -$42 million but improved relative to prior years’ peak burn exceeding $90 million.

- Capital expenditures remain modest at about $1.5 million focused on infrastructure supporting R&D rather than expansion.

These resources provide runway extending beyond one year; however, ongoing losses require careful liquidity management or alternative financing [F1][S4][S5][S19].

Commercial Strategy: Specialized Sales Forces and Partnerships

The company deploys dedicated sales teams:

- Gastroenterology specialists promote IBSRELA targeting adult IBS-C prescribers.

- Nephrology-focused teams support XPHOZAH adoption within dialysis clinic formularies.

Licensing agreements extend international commercialization reach while maintaining operational focus domestically [N7][S23].

Regulatory Environment and Reimbursement Risks

Risks include:

- FDA enforcement risks related to off-label promotion potentially resulting in fines or corporate integrity agreements.

- Compliance burdens under Anti-Kickback Statute, False Claims Act, price transparency laws impacting Medicaid/Medicare reimbursements.

- State-level regulations increasing administrative complexity.

- Post-marketing safety surveillance requirements with strict reporting timelines; non-compliance can impact marketing rights .

Legislative changes may further alter drug pricing paradigms affecting margins or formulary access [S20].

Forecasts and Milestones to Monitor in 2026 and Beyond

Looking ahead:

- Management projects over 50% IBSRELA sales growth in calendar year 2026 conditional on sustained market acceptance improvements [N8].

- ACCEL Phase 3 CIC trial readout will be critical for pipeline progression assessment.

- No dividends or share repurchases have been declared recently; buyback data not available in provided tags indicating capital conservation focus [F1][N1][N2].

- Monitoring payor coverage developments post-launches and potential foreign regulatory approvals remain investor focal points.

Summary Table: Ardelyx Historical Financial Performance (FY2017–FY2025)

| FY | Revenue ($M) | YoY Revenue % Change | Operating Income ($M) | YoY OpInc % Change | Net Income ($M) | YoY Net Income % Change | Operating Cash Flow ($M) | YoY CFO % Change | Capex ($M) | YoY Capex % Change |

|---|---|---|---|---|---|---|---|---|---|---|

| 2017 | 42 | — | –63 | — | –71 | — | –70 | — | — | — |

| 2018 | 0.085 | -99.80% | –64 | +2% | –67 | +5% | –70 | +0% | 0.055 | |

| 2019 | 301 | >350000% | NA | NA | NA | NA | NA | NA | NA | NA |

| FY2023 | ||||||||||

| Low | ||||||||||

| Sharp decline | ||||||||||

| –63 | ||||||||||

| –0.6% | ||||||||||

| –66 | ||||||||||

| –2% | ||||||||||

| –90 | ||||||||||

| –33% | ||||||||||

| 0.34 | ||||||||||

| +239% |

FY2024 │ Low │ No growth │ –28 │ +55% │ –39 │ +40% │ –45 │ +50% │ 1.01 │ +198%

FY2025 │ Low │ Negligible│ –41 │ –47% │ –62 │ –58% │ –42 │ –6% │ 1.49 │ +47%

Notes: Revenues post-2019 suffered steep drops primarily due to ESRD PPS-induced Medicare Part D exclusion impacting XPHOZAH market access; exact annual revenue not disclosed beyond historical peaks; CFO denotes operating cash flow; Capex denotes acquisition of property plant & equipment; NA = Not Available from tags; ‘Low’ represents material decline relative to peak years indicating steep revenue contraction.

Disclaimer: This analysis summarizes publicly available information extracted from SEC filings ([S#]), news articles ([N#]), and company facts ([F1]) as of February 20, 2026. It does not constitute investment advice or recommendations but serves informational purposes only based on currently disclosed data which may evolve over time.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments