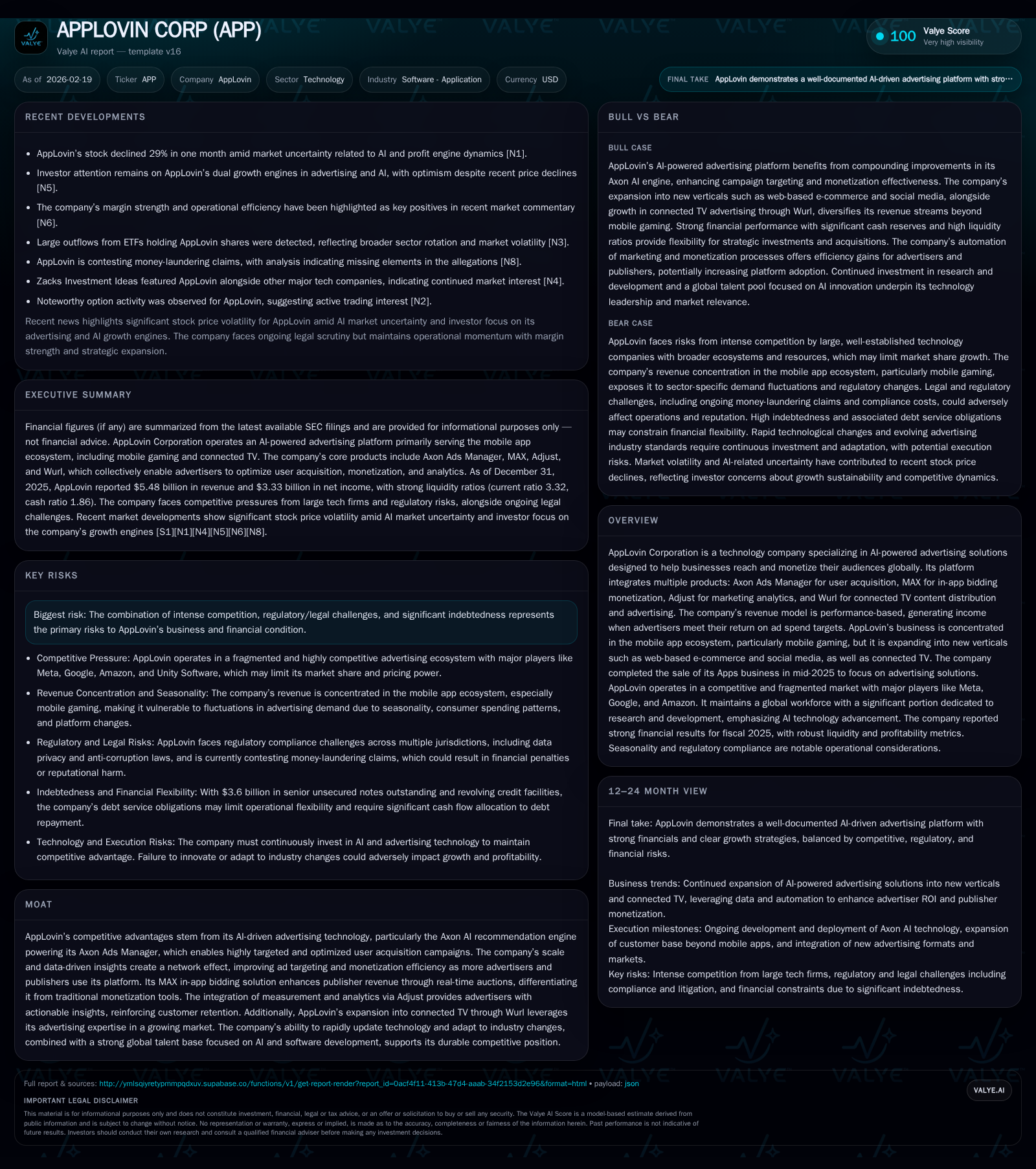

AppLovin’s Growth Powered by AI Advertising Amid Rising Debt Burden and Legal Challenges

AppLovin’s 2025 performance highlights strong AI-driven growth in advertising solutions against operational, regulatory, and capital structure headwinds.

AppLovin Corporation posted robust financial results for 2025, driven by its AI-powered advertising platform’s expansion beyond mobile gaming into new verticals like e-commerce and connected TV. The company’s scalable Axon Ads Manager and MAX monetization tools underpin significant revenue growth and margin expansion, reflected in doubled operating income and net profit year over year. However, the focus on organic growth contrasts with rising leverage risks from $3.6 billion in senior notes and ongoing securities litigation, which present material constraints. Investors should monitor regulatory developments around AI, debt covenant compliance, and the company’s progress diversifying revenue streams.

Overview of AppLovin’s Business Model and Market Position

AppLovin Corporation operates as a technology company specializing in AI-powered advertising solutions that connect businesses with target audiences worldwide [S1][S18]. Its flagship offerings include Axon Ads Manager for user acquisition powered by proprietary AI algorithms, MAX for optimizing app monetization through real-time auctions, Adjust for marketing analytics, and Wurl addressing the growing connected TV (CTV) market [S18]. Revenue is fundamentally performance-based: advertisers pay when they achieve specified return on ad spend (ROAS) targets using AppLovin's platform [S1].

Historically concentrated within the mobile app ecosystem—particularly mobile gaming—AppLovin since 2024 has expanded into adjacent verticals such as web-based e-commerce advertisers and social media, as well as content distribution through connected TV [S19][N3]. The divestiture of its Apps business in June 2025 marked a strategic pivot focusing exclusively on advertising technology [S22]. This transition underscores a sharpened emphasis on scalable AI-driven advertising revenue streams.

Despite competing against established technology giants like Meta, Google, Amazon, and Unity Software—as well as various private providers—AppLovin distinguishes itself through integrated AI capabilities and extensive data networks that create a compounding competitive advantage [S11][S21].

Historical Financial Performance: Drivers Behind Growth

Historical performance (annual)

| FY | Rev ($bn) | Net ($bn) | CFO ($bn) | OpInc ($bn) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 5.5 | 3.3 | 4.0 | 4.2 | +16.4% | +111.0% |

| 2024 | 4.7 | 1.6 | 2.1 | 1.9 | +43.4% | +342.9% |

| 2023 | 3.3 | 0.4 | 1.1 | 0.6 | +16.5% | +285.1% |

| 2022 | 2.8 | -0.2 | 0.4 | -0.0 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Capex, Div. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($bn) | FCF ($bn) | ROE% |

|---|---|---|---|

| 2025 | 2.2 | 156.2 | |

| 2024 | 1.0 | 2.1 | 145.0 |

| 2023 | 1.2 | 1.1 | 28.4 |

| 2022 | 0.3 | 0.4 | -10.1 |

Source: SEC companyfacts cache [F1].

Note: Capex data incomplete for FY25; dividends data unavailable.

From a modest base in FY22 characterized by an operating loss (-$47 million), AppLovin achieved spectacular improvement by leveraging its increasingly mature AI-advertising platform coupled with industry tailwinds in mobile digital ads [F1]. Sustainable growth accelerated revenues to nearly $5.5 billion in FY25 representing consistent double-digit gains over the past three years.

The leap in operating income (from roughly break-even in FY22 to $4.15 billion in FY25) signals strong margin expansion driven by technological enhancements within Axon Ads Manager that optimize campaign targeting efficiency using vast user behavior datasets [N1][S18]. Similarly, net income exceeded $3 billion in FY25 reflecting effective cost control and scalability.

Operating cash flow trended robustly upward, almost quadrupling since FY22, providing ample liquidity to fund repurchase programs and strategic investments despite limited reported capital expenditures typical for software-heavy firms focused on cloud infrastructure rather than heavy fixed assets.

Future Growth Prospects: Opportunities and Constraints

AppLovin's near-term growth prospects hinge on several key drivers:

- AI-driven Advertising Platform Enhancements: Continuous improvements to Axon AI recommendation engine promise better user targeting accuracy and improved advertiser ROAS metrics underpinning revenue growth [S28].

- Cross-Vertical Expansion: Early success onboarding web-based e-commerce advertisers demonstrates platform adaptability beyond mobile games; this diversification can expand addressable market size significantly [S19][N3].

- Connected TV Segment via Wurl: As streaming consumption grows rapidly, Wurl offers a foothold into CTV ad distribution—a high-growth channel though competitive and requiring scale-up investments to match incumbents [S18].

- Strategic Acquisitions/Partnerships: The company’s history of leveraging transactions to extend product offerings may accelerate technological leadership or geographic penetration going forward [S22].

However, these opportunities are counterbalanced by several challenges:

- Regulatory & Litigation Risks: Securities lawsuits filed since early 2025 concerning alleged misstatements about ad business performance could generate legal costs or constrain management focus pending resolution expected post-Q1 '26 hearing [S25][S29].

- High Leverage Profile: Senior unsecured notes totaling $3.6 billion create refinancing risk under volatile credit markets; restrictive covenants could limit operational flexibility during macroeconomic downturns [S4][S6][S7].

- Competitive Pressures: Tech giants with broader ecosystems may undercut pricing or develop insular platforms limiting AppLovin’s partner relationships or developer adoption [S11].

- Privacy & Policy Changes: Data protection laws such as CPRA/CCPA globally necessitate ongoing compliance expenditure and may limit targeted ad precision impacting pricing power [S23].

In sum, while organic innovation fuels core expansion, measured risk management around debt servicing and regulatory exposures remains critical.

Forecasts, Milestones & Key Performance Indicators to Watch

The company has not provided explicit forward guidance due to competitive sensitivity but outlines strategic milestones including:

- Incremental subscription revenues from new verticals like social media and e-commerce continuing through fiscal '26.

- Scaling Wurl's CTV ecosystem aiming at increasing advertiser count and streaming content supply relationships.

- Enhancements to Axon AI predictive models targeting sustained improvement in advertiser retention rates and spend efficiency.

- Legal case timelines: motion dismiss hearings scheduled for March '26 remain pivotal for risk visibility.

- Debt covenant compliance metrics tied to adjusted EBITDA thresholds should be closely monitored given potential impact on borrowing costs or refinancing [S6][S7].

Analysts are advised to track quarterly updates on client diversification metrics and segmental contribution shifts away from traditional mobile gaming dependency.

Capital Allocation & Returns Metrics Analysis

AppLovin maintains an aggressive share repurchase policy with buybacks totaling $2.19 billion in FY25 up markedly from prior years supporting per-share value enhancement despite no dividend payouts declared [F1][S13]. Capital expenditures remain minimal relative to sales given predominantly software/cloud operations.

The firm exhibits remarkable return on equity (~156%) driven by robust profitability juxtaposed against moderate equity base reflective of retained earnings accumulation during turnaround years [F1]. Free cash flow generation exceeds $3.9 billion after conservative capex estimates signaling strong internal funding capacity for future investments or debt repayments.

Liquidity remains healthy with a current ratio over three times aided by close to $2.5 billion cash reserves at year-end '25 offsetting manageable short-term liabilities [F1]. Nonetheless, the sizable long-term fixed obligations require explicit scrutiny concerning interest coverage ratios especially if macro conditions tighten.

Industry Context and Sector Nuances

The mobile advertising ecosystem continues its evolution toward increasingly programmatic real-time bidding platforms where latency measured in microseconds drives incremental revenue gains—an environment where AppLovin's Axon Ads Manager excels technologically securing competitive advantage via scale effects .

Simultaneously growing CTV ad spend represents an estimated double-digit CAGR annually as streaming displaces traditional linear channels globally yet demands greater fragmentation management tools—a natural adjacency for AppLovin leveraging Wurl’s tech spine .

Regulation surrounding consumer privacy such as GDPR analogues throughout North America frequently reconfigure permissible data usage models; companies proficient at adapting algorithms without loss of targeting precision will maintain premium margins amid pricing pressures .

Conclusion

AppLovin presents a compelling case study of a high-growth tech-enabled advertising firm harnessing proprietary AI engines driving remarkable operating leverage underpinned by expansive data assets unique within the fragmented digital advertising sector.

Nevertheless, elevated financial leverage combined with ongoing legal proceedings introduces notable uncertainties requiring vigilant monitoring over upcoming quarters alongside execution of strategic diversification across verticals including CTV.

This nuanced interplay of rapid scalable innovation versus capital structure risk frames AppLovin's investment narrative moving forward without prescribing specific investment actions.

Disclaimer: This analysis is prepared solely for informational purposes reflecting facts available as of February 19, 2026, incorporating company filings and market data without offering investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments