ONE Gas Surges with Strategic Growth and Capital Discipline in 2025

A review of ONE Gas’s robust 2025 performance driven by infrastructure investment, strengthened liquidity measures, and balanced capital deployment.

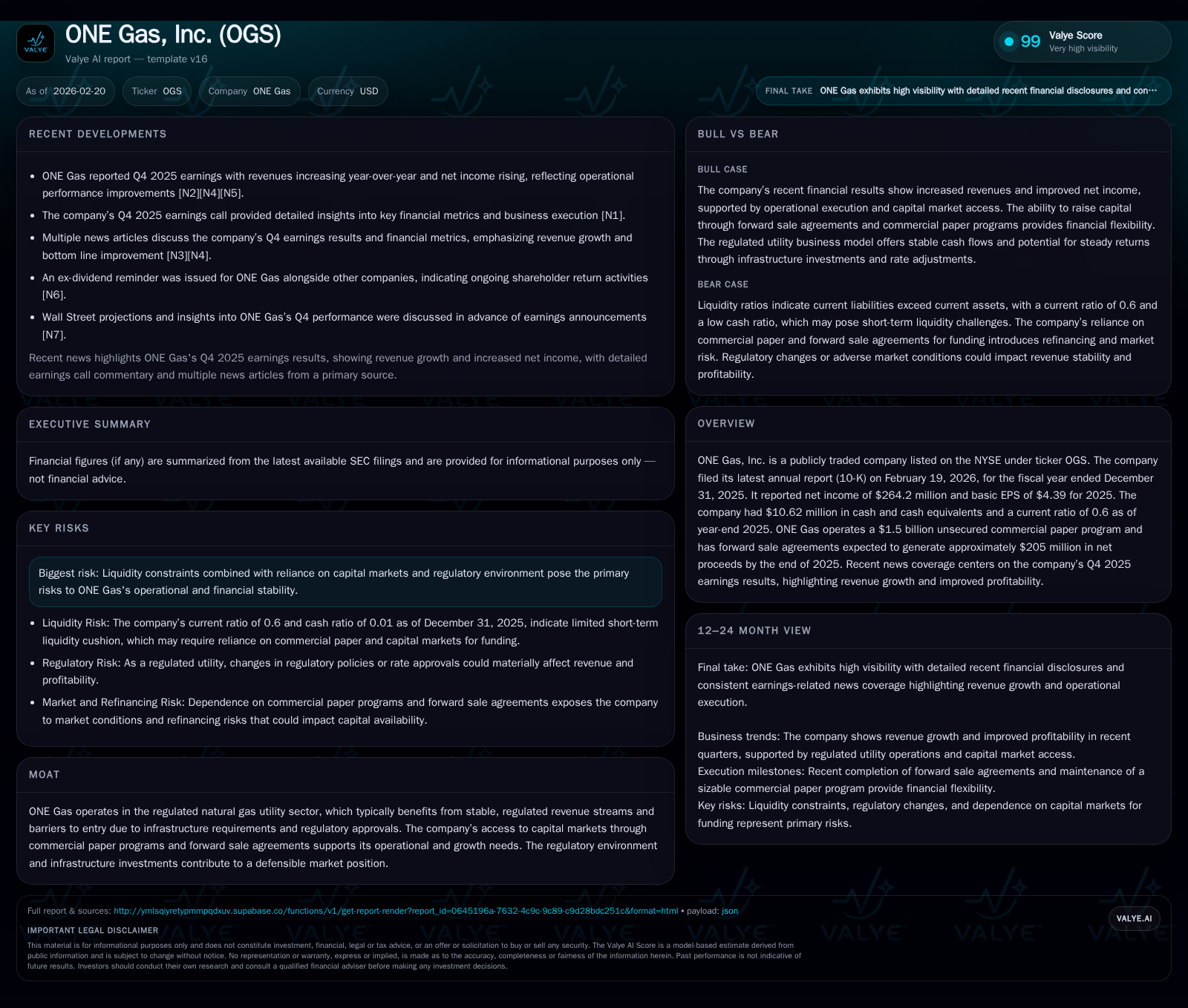

In 2025, ONE Gas delivered notable financial growth highlighted by a 42.5% increase in revenue and a 14.6% uplift in operating income, underscoring effective leverage of its regulated natural gas utility business model. The company's strategic $1.5 billion commercial paper program expansion and $205 million forward sale agreements enhanced liquidity despite a conservative current ratio of 0.6. Capital allocation maintained a focus on sustainable dividends amid substantial infrastructure capex totaling approximately $707 million. Regulatory frameworks and evolving tariff proceedings remain crucial factors shaping its near-term operational and financial landscape.

2025 Results Highlight Accelerated Growth Trajectory

ONE Gas posted an impressive acceleration in financial metrics for fiscal year 2025, underscoring the strength of its regulated natural gas utility operations within its service territories. Revenue leapt by approximately 42.5% year-over-year to USD 2.58 billion—an outsized increase indicative of favorable tariff adjustments and growing demand [F1]. Operating income reached USD 457 million, up nearly 14.6%, signaling effective cost management alongside volume appreciation [F1]. Net income climbed by close to 18.6% to USD 264 million, reinforcing improved bottom-line profitability [F1]. Moreover, operating cash flow rose more than 57% year-over-year to USD 579 million, suggesting amplified utility consumption patterns or efficient working capital management [F1].

This constellation of growth metrics reflects not only robust regulated revenue streams but also an operational model capable of absorbing infrastructure investments without diluting margins.

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 264 | 579 | 457 | |||

| 2023 | 223 | 368 | 399 | +0.5% | ||

| 2022 | 2.6 | 222 | 1571 | 350 | +42.5% | +7.4% |

| 2021 | 1.8 | 206 | -1536 | 310 | +18.2% |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Capex, Buybacks. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | FCF ($bn) | ROE% |

|---|---|---|---|

| 2025 | 161 | -0.1 | 7.7 |

| 2023 | 149 | -0.3 | 7.2 |

| 2022 | 134 | 1.0 | 8.6 |

| 2021 | 124 | -2.0 | 8.8 |

Source: SEC companyfacts cache [F1].

Note: Revenue YoY % data for FY2025 unavailable; FY figures for FY2024 missing from available dataset.

Evolving Drivers Behind Revenue and Operating Income Gains

The backbone of ONE Gas’s revenue jump lies partly in base rate cases approved across its principal subsidiaries: Oklahoma Natural Gas, Kansas Gas Service, and Texas Gas Service [S1][N1]. These regulatory tariff proceedings have granted upward rate adjustments calibrated to fund infrastructure modernization while maintaining authorized returns on rate base assets.

Capital expenditures approaching USD 707 million—nearly flat versus prior year—primarily fund pipeline integrity projects ensuring compliance with federal safety regulations as well as expansion initiatives to meet incremental customer demand [S1][S5][N1]. Notably, demand-side management programs encourage efficiency among consumers yet simultaneously necessitate ongoing maintenance capex to balance supply reliability.

Sector-specific vernacular comes into play here: ONE Gas is actively increasing its rate base through investments that strengthen both system integrity and capacity ahead of forecasted consumption growth — effectively locking in future regulated earnings streams based on infrastructure footprint expansion.

Capital Structure Strengthened: Commercial Paper Program and Liquidity

A pivotal development in late-2025 was the expansion of the company's unsecured commercial paper program limit to USD 1.5 billion from USD 1.35 billion [S7][S8]. This move directly addresses operational liquidity needs amid seasonally volatile working capital demands inherent in utilities.

However, the balance sheet snapshot reveals a conservative current ratio hovering around 0.6 due to elevated current liabilities over current assets as of December-end [F1]. This mismatch implies reliance on short-duration debt rollovers supported by ready access to liquid capital markets rather than cash reserves alone.

Complementing this strategy are forward sale agreements poised to deliver approximately USD 205 million net proceeds by year-end [S15][S16], boosting near-term liquidity without immediate dilution or long-term indebtedness increase.

While typical within utility financial structures given regulatory lag effects and gradual cost recovery via tariff mechanisms, this liquidity positioning requires prudent balance to avoid funding stress during adverse credit market conditions.

Capital Allocation Focus: Dividends, Buybacks, and Investment Priorities

Capital allocation decisions in FY2025 emphasize sustaining shareholder distributions while accommodating heavy capex commitments characteristic of the sector's infrastructural imperatives [F1][S9][S10]. Dividends paid amounted to USD 160.7 million—a growth trajectory consistent with previous years reflecting steady payout ratios aligned with regulated earnings profiles.

Despite modest return on equity approximating a typical utility norm near 7.7%, buyback activity remains dormant in recent periods [F1], indicative either of capital conservation preferences amidst regulatory uncertainties or prioritization toward reinvestment rather than share repurchases.

Such discipline aligns with ONE Gas's operational mandate balancing investor expectations against ongoing infrastructure funding requirements needed to preserve system integrity and support future demand escalation.

Regulatory Environment Impacting Growth Prospects

As a natural monopoly operating under state utility commissions’ jurisdiction, ONE Gas faces systematic exposures spanning tariff review schedules, environmental compliance mandates, and legislative policy shifts [S4][S6]. Regulatory lag—whereby expenditures precede recovery through rates—remains relevant, underpinning both revenue timing visibility and earnings forecasting difficulty.

Moreover, mandated upgrades addressing pipeline integrity directly influence capex trajectories but yield durability benefits securing long-term asset reliability under jurisdictional scrutiny [S1]. Successfully navigating these proceedings supports continued rate base accretion fundamental to long-term revenue advancement.

Key Risks: Liquidity Constraints and Market Dependencies

Liquidity management emerges as the leading risk vector with dependency on commercial paper issuances exposing ONE Gas to market sentiment fluctuations that could tighten funding availability unexpectedly [S4][S6][F1]. The modest cash buffer juxtaposed with sizeable current liabilities ratchets pressure on rolling short-term commitments smoothly.

Coupled with regulatory uncertainty surrounding timing and magnitude of rate cases—which can delay incremental cost recoveries—this risk profile necessitates vigilant treasury oversight alongside robust capital market engagement strategies.

Path Forward: Monitoring Operational Milestones and Financial Metrics

Looking ahead, observers should track upcoming rate case filings across the three main local distribution operations alongside execution progress on large-scale pipeline projects such as the $120-$160 million joint initiative targeting southeast Oklahoma’s Hugo Plant supply needs slated for completion in Q3 of 2028 [S17].

Additionally, monitoring quarterly updates on operating cash flow stability will provide insight into potential margin compression or expansion linked to commodity pricing pass-throughs or consumption changes [N13][N5]. While explicit quantitative guidance remains absent from latest disclosures, management commentary signals confidence in balanced growth underpinned by disciplined capital deployment.

Leadership continuity is evidenced by key executive promotions effective March ’26 designed to bolster operational execution capabilities without disruptive turnover risk [S19]. This facet complements ongoing strategic efforts focused on expanding infrastructure footprint while navigating evolving regulatory landscapes.

Disclaimer: This analysis relies solely on publicly available information from SEC filings and credible news sources as cited; it does not constitute investment advice or solicitation.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments