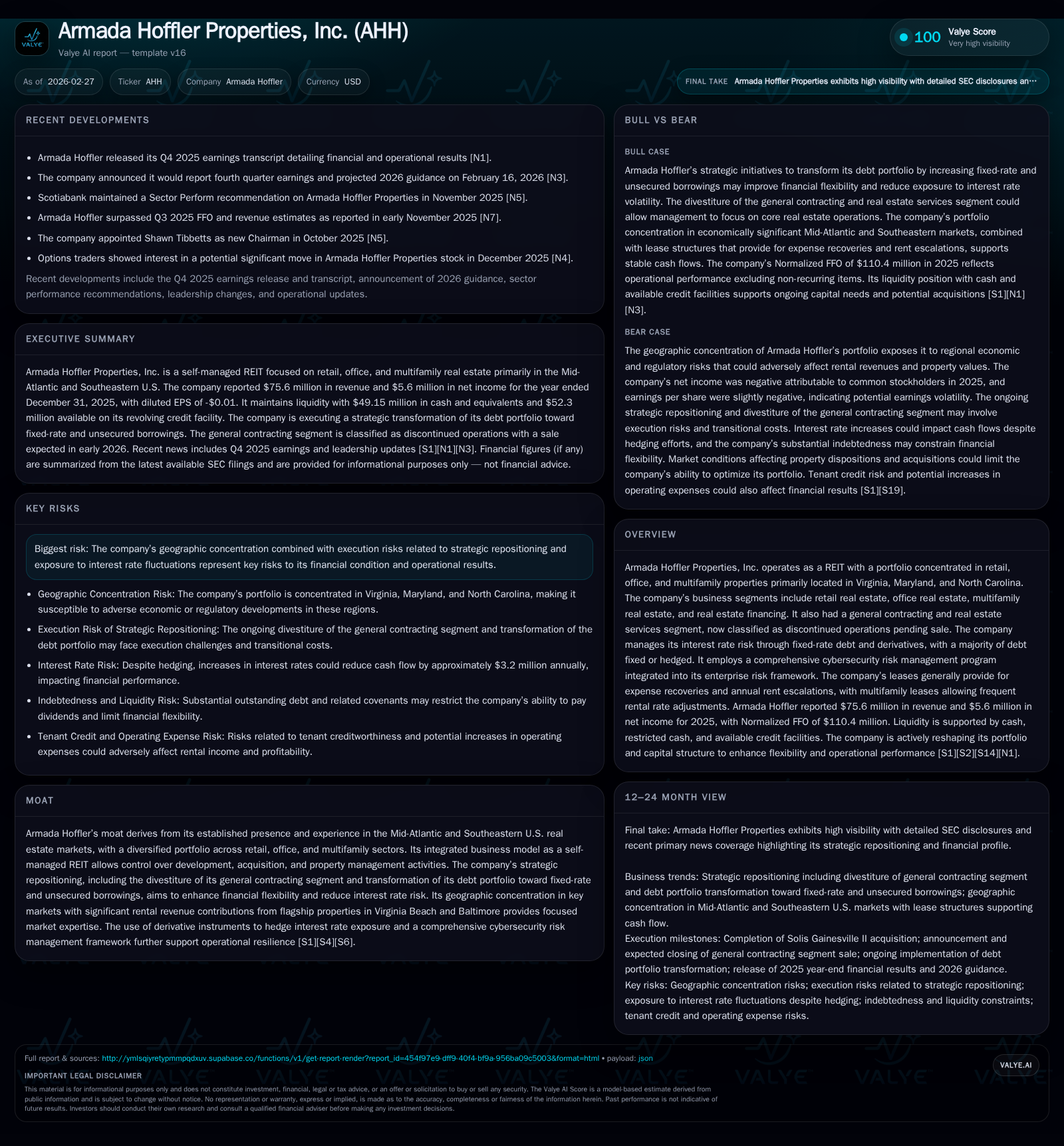

Armada Hoffler Properties Shrinks Revenue Amid Strategic Shifts and Market Focus

The company’s revenue plummeted sharply in 2025 due to segment divestiture and portfolio concentration, while proactive debt restructuring and leasing strategies shape its near-term outlook.

Armada Hoffler Properties experienced an extraordinary 89% drop in revenue in fiscal 2025, primarily driven by the classification of its general contracting segment as discontinued operations and divestiture activities. Despite this sharp shrinkage, the REIT maintained a positive operating cash flow, reflecting resilient core property operations. Strategic repositioning efforts focused on reducing interest rate exposure via increased fixed-rate and unsecured debt, alongside a consolidated geographic focus in Mid-Atlantic markets, aim to stabilize financial flexibility. However, concentrated market risks, execution uncertainties tied to the ongoing transformation, and reliance on external capital pose material constraints on growth prospects and dividend sustainability.

Historical Financial Performance: Revenue Collapse and Margin Impact

Armada Hoffler Properties faced a striking contraction in revenue for fiscal year 2025, landing at approximately $75.6 million compared to $708.5 million a year prior—a nearly 89.3% decline based on SEC-filed figures [F1]. This precipitous drop primarily reflects the reclassification of the general contracting and real estate services business as discontinued operations pending sale, leading to a substantial reduction in reported continuing operations revenue as highlighted during the Q4 earnings call transcript [N1] and detailed in the annual report discussion [S1].

Despite extreme revenue compression, operating income stayed positive at about $23.5 million for 2025 but fell by approximately 78% from $106.5 million in 2024 [F1]. Net income suffered an even sharper fall of roughly 84%, down to $5.6 million from $35.6 million previously, evidencing margin pressure beyond pure top-line softness caused by segment divestiture effects [F1]. This translates into an approximate return on equity around 0.9%, highlighting minimal generation of net profits on shareholder equity given the transition phase.

Operating cash flow (CFO) remained resilient with prior years showing solid cash flows upward of $112 million for 2024 and consistent levels near or above $90 million annually before that [F1]. While specific CFO for 2025 is not yet available, continued operational activity outside discontinued segments supports reasonable cash generation relative to earnings trends.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 76 | 6 | 23 | -89.3% | -84.3% | |

| 2024 | 708 | 36 | 112 | 107 | +6.2% | +330.1% |

| 2023 | 667 | 8 | 93 | 74 | +46.9% | -88.9% |

| 2022 | 454 | 75 | 117 | 117 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | ROE% |

|---|---|---|---|

| 2025 | 75 | 0 | 0.9 |

| 2024 | 84 | 0 | 5.3 |

| 2023 | 80 | 13 | 1.4 |

| 2022 | 73 | 11.5 |

Source: SEC companyfacts cache [F1].

The table illustrates Armada Hoffler's drastic decline in reported continuing revenues driven largely by divested operations reclassification.

Strategic Repositioning: Divestitures and Debt Transformation

Armada Hoffler's strategic repositioning centers on refocusing its operations exclusively on core real estate assets by shedding ancillary businesses such as the general contracting segment now treated as discontinued operations pending sale as described in both the latest annual report [S1] and Q4 transcripts [N1]. This streamlining effort aims to sharpen operational focus but significantly diminished total revenue reported under continuing lines.

Simultaneously, the company has actively transformed its debt structure seeking enhanced financial flexibility and reduced interest rate risk amid volatile credit markets—a priority emphasized repeatedly in regulatory filings [S1], with specific measures including:

- Issuance of $115 million fixed-rate private placement notes in mid-2025 bearing coupons ranging from approximately mid-5% to just above 6%, providing long-dated unsecured funding sources with predictable interest costs rather than floating rate exposure typical of prior borrowings [S7], [S9], [S13].

- Increasing proportion of fixed-rate debt from approximately $680 million at end-2025 versus variable-rate debt near $847 million; variable-rate exposure is hedged effectively via derivative instruments reducing sensitivity to SOFR shifts [S9], [S14], [S16].

- Growing unsecured borrowings now representing over 61% of total indebtedness versus ~56% previous year reflecting deliberate deleveraging of secured loans backed by property collateral to avoid encumbrances limiting capital deployment agility.

Management notes execution risks inherent during transition which could impact liquidity if market conditions deteriorate or refinancing options become constrained unexpectedly [S1].

Operating Segments: Retail, Office, Multifamily Dynamics in Core Markets

Armada Hoffler's operating portfolio remains geographically concentrated within three adjacent states: Virginia, Maryland, and North Carolina — key Mid-Atlantic/Southeastern hubs offering a mix of retail shopping centers, office buildings, and multifamily residential properties per their corporate disclosures [S1]. Such geographic concentration enhances local market expertise but exposes the REIT to regional economic cycles or regulatory shocks disproportionately compared with more diversified peers.

Leasing arrangements across retail and office assets generally include provisions for tenant expense recoveries contributing incremental revenues tied to operational costs like property taxes or maintenance escalating annually alongside base rent hikes embedded per contract terms noted in SEC narratives [S1]. Meanwhile multifamily leasing exhibits greater flexibility featuring shorter-term leases permitting periodic rent resets responsive to prevailing market conditions—a sectoral nuance beneficial for nimble rent optimization as demand fluctuates.

This leasing roll dynamic stabilizes cash flows even during market softness but also introduces vulnerability where multifamily segments could see rapid downturns if local affordability weakens or economic disruptions depress tenancy rates.

Interest Rate Hedging and Risk Management Frameworks

Armada Hoffler integrates a comprehensive interest rate risk mitigation strategy involving fixed-rate borrowings complemented by derivative hedge instruments designed specifically around SOFR-linked variable debt exposures outlined extensively in filings [S1], protecting against sudden benchmark rate spikes that would otherwise inflate financing costs materially.

By balancing roughly one-fifth fixed-interest funding plus effective swaps neutralizing large portions of floating liabilities' volatility exposure as documented through their credit facility disclosures ([S14]), Armada Hoffler exhibits prudent treasury management reflective of rising uncertainty in credit markets currently.

Furthermore, cybersecurity is incorporated within its enterprise risk framework emphasizing continuous monitoring protocols to avert operational disruptions caused by potential cyber threats — a relevant modern safeguard increasingly expected across institutional asset managers but explicitly reaffirmed here per company statements ([S1]).

Capital Structure Evolution: Debt Profile and Liquidity Position

As of December-end 2025, Armada Hoffler maintains total principal borrowings around $1.53 billion split between fixed-rate debt ($679.6 million) and variable-rate borrowings ($847 million) with scheduled principal repayments extending through the next several years highlighted below from filings ([S9]):

- Significant maturities loom especially across next three years including approximately $420 million due in calendar year-2026.

- Revolving credit facility capacity totaled about $655 million following accordion expansions providing upcoming liquidity headroom totaling approximately $52 million currently unutilized as per quarterly discussions ([S5],[S16]).

- All loan covenants remain satisfied across credit agreements encompassing leverage thresholds below maximum permitted caps (60%) ensuring ability under current terms to maintain distributions within limits imposed by debt agreements ([S8],[S9],[S17]).

This evolving liability mix targets a balance favoring unsecured senior notes atop stabilized cash flows yet continues maintaining some secured property loans factoring into risk diversification strategies discussed internally ([S16]).

Cash Generation and Capital Allocation: Dividends vs Buybacks

Dividend policy reflects traditional REIT distribution mandates requiring high payout ratios often near taxable income margins combined with investor expectations aligned on yield priorities ([S4]). Armada Hoffler declared dividends aggregating roughly $75 million during fiscal year ended December 31 2025 despite trailing net profits significantly reduced from previous years ([F1],[S4]). This represents a defensive capital allocation approach aiming to preserve shareholder income streams amid corporate earnings pressure.

Conversely Armada Hoffler ceased share repurchase activity during FY25 although maintaining a buyback authorization with nearly $37 million capacity remaining unused—likely reflective of conservatism amid constrained liquidity and emphasis on strengthening balance sheet relative flexibility ([S4]). Prior buybacks executed modestly (~$12.6m) before this pause illustrate selective opportunistic use rather than regular capital return policy implied historically ([F1]).

Looking Ahead: Growth Constraints and Opportunities in Key Regions

Forward momentum faces clear headwinds from geographic concentration rendering the firm vulnerable if economic or regulatory environments destabilize within Virginia-Maryland-North Carolina corridors ([N2],[S1]). Credit market dislocations present additional challenges potentially limiting acquisition financing or capital expenditures necessary for redevelopment initiatives shaping long-term value creation.

Leasing renewal dynamics remain critical indicators where successful lease retention coupled with annual rent escalations built into contracts underpin stable fundamental revenues amidst volatile broader demand cycles ([S1]). Multifamily rental flexibility offers some cushioning yet also carries downside risks during softened tenant demand phases through short-term lease expirations.

Absent explicit disclosed development pipelines or new acquisitions from current materials available ([N2]), growth must rely heavily on organic portfolio yield improvements balanced against potential property dispositions aimed at further refining asset base focus.

What Investors Should Monitor: Leases, Financing Access, Execution Risks

Stakeholders should track several performance touchpoints influencing Armada Hoffler's trajectory:

- Leasing roll success rates particularly within office and multifamily properties determining achievable rental rates amid ongoing market shifts.

- Continued access to capital markets facilitated by maintenance of favorable credit ratings ensuring competitive borrowing costs while managing covenant compliance closely ([S6],[S10],[S19]).

- Progress against strategic plan milestones around divestiture completions coupled with timely execution minimizing transitional disruptions warned about explicitly as material risks ([S1]).

- Effectiveness of interest rate hedging sustaining cost containment as benchmark rates remain volatile impacting debt servicing burdens.

- Portfolio occupancy thresholds especially unencumbered assets monitored pursuant contractual loan agreements acting as liquidity safeguards ([S9],[S17]).

Maintaining vigilance on these parameters offers pragmatic insight into how well Armada Hoffler manages internal transformation against external headwinds without presuming outcomes beyond disclosed facts.

This analysis is based solely on information available through February 27th 2026 as presented in SEC filings and public transcripts without speculative forecasts or investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments