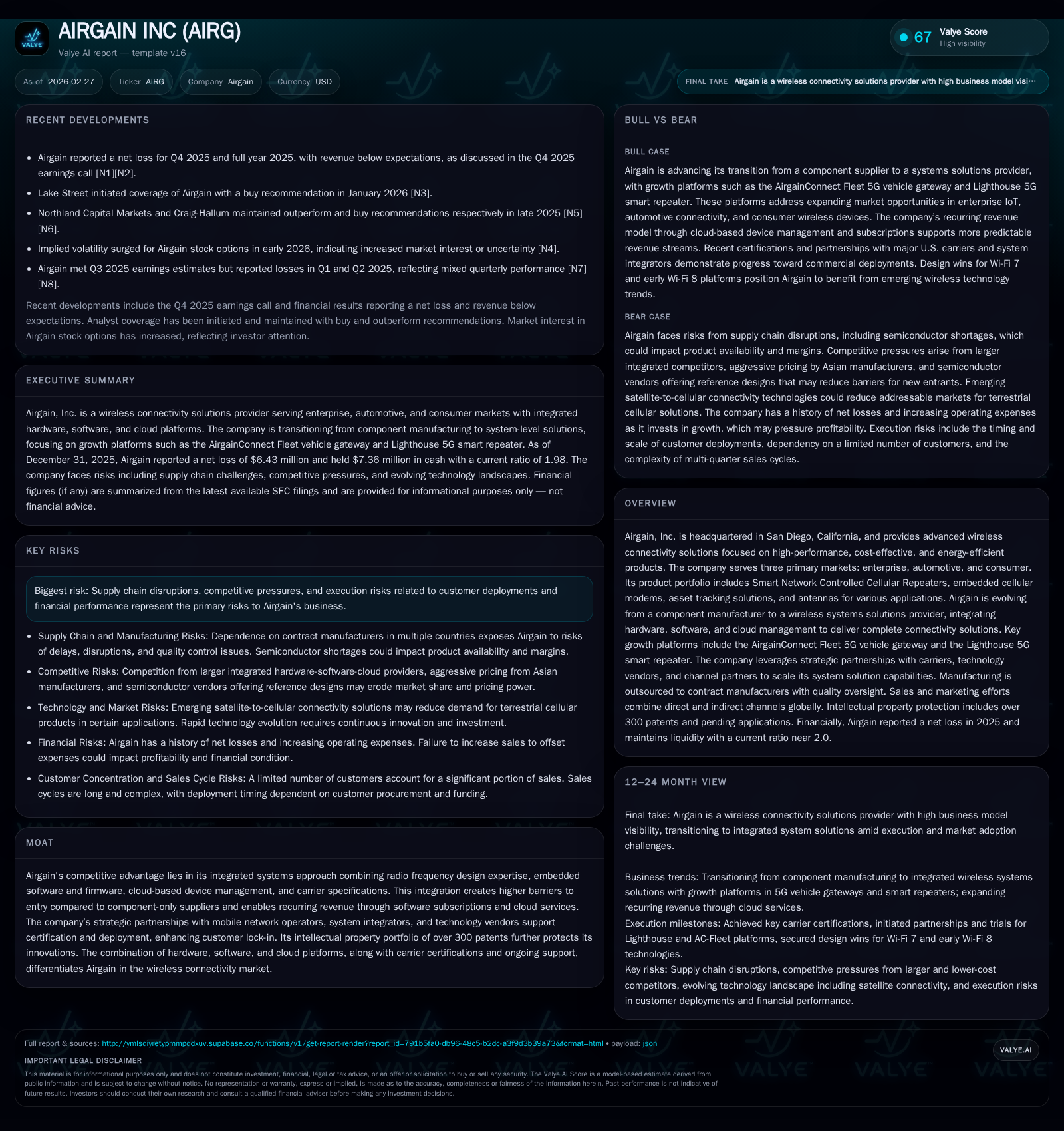

Airgain’s Transition to Integrated Connectivity Solutions Challenges Profitability

Airgain's strategic evolution from RF hardware supplier to integrated wireless systems provider introduces operational complexity that weighs on margin expansion and profitability.

Airgain, historically rooted in high-performance radio frequency components, is pursuing a transformational strategy by embedding software and cloud management into its connectivity offerings. This shift supports entry into higher-value markets such as 5G smart repeaters and automotive vehicle gateways but has led to sustained operating losses and negative cash flow amid rising execution risks. While revenue grew slightly in fiscal 2025, the incremental system integration complexity tempers near-term financial returns. Key upcoming milestones include broader carrier certifications for core platforms and deeper market penetration in automotive telematics. Observers should watch quarterly revenues, customer deployments, and channel partner expansions as indicators of Airgain's ability to scale its integrated solutions effectively.

From RF Components to Integrated Connectivity: Airgain’s Business Evolution

Airgain’s legacy as a manufacturer of high-performance radio frequency components has underpinned its reputation within telecommunications OEMs and network operators. Headquartered in San Diego, the company historically excelled in designing antennas for consumer access points, external modems, and IoT devices. Over recent years, however, Airgain has embarked on a deliberate pivot towards offering comprehensive wireless connectivity solutions that marry hardware with embedded software, firmware, and cloud-based device management platforms [S1][S4][S6].

The cornerstone of this transformation is exemplified by their Smart Network Controlled Cellular Repeaters (Smart NCRs), notably the Lighthouse platform—a high-power 5G smart repeater designed to extend mobile coverage cost-effectively without the infrastructure costs of small cells or Distributed Antenna Systems (DAS). Complementing this is the AirgainConnect Fleet—the second-generation low-profile roof-mounted 5G vehicle gateway targeting the increasingly connected automotive fleet sector.

This integration elevates Airgain beyond component supply towards a systems provider role that requires synchronization with carrier specifications including carrier aggregation, TDD synchronization, echo cancellation, firmware-over-the-air updates (FOTA), and remote monitoring via cloud platforms such as AirgainConnect Cloud. The move promises sticky revenue streams through subscription-based software services alongside hardware sales [S4][S6].

Historical Financial Performance and Underlying Growth Drivers

Examining fiscal year data between 2017 through 2025 reveals modest top-line expansion alongside chronic profitability challenges (see Table below). Revenue increased modestly by roughly +1.4% in FY2025 relative to FY2024 reaching $12.8 million USD [F1]. This slow growth masks underlying shifts wherein higher-value system integrations are expanding even as volume-driven component sales plateau.

Operating income remains negative but improved marginally from -$8.93 million in FY2024 to -$8.48 million in FY2025, indicating some operational leverage albeit insufficient for sustained profitability. Net losses also narrowed substantially—down about 26% year-over-year—with net income improving from -$8.69 million to -$6.43 million [F1].

Cash flow metrics highlight ongoing investment burdens; operating cash flow remained negative at approximately -$1.11 million in FY2025 although it improved significantly versus the prior year figure of -$3.53 million. Capital expenditures trimmed slightly to $166k reflecting conservative investment aligned with outsourcing models rather than heavy internal manufacturing infrastructure spend [F1]. The firm holds a strong current ratio near two times (~1.98), suggesting healthy short-term liquidity buffers despite accumulated deficits approaching $94 million USD at year end 2025 [F1][S1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -6 | -1 | -8 | 166000 | +26.0% |

| 2024 | -9 | -4 | -9 | 178000 | +30.1% |

| 2023 | -12 | -3 | -12 | 346000 | -43.5% |

| 2022 | -9 | 4 | -9 | 763000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -1 | -22.7 |

| 2024 | -4 | -28.1 |

| 2023 | -4 | -39.6 |

| 2022 | 4 | -21.7 |

Source: SEC companyfacts cache [F1].

*Approximately derived for illustration purposes only from available data; see narrative for exact figures.

Emerging Growth Platforms and Market Opportunities in 5G and IoT

With global mobile networks ramping up advanced 5G deployments—transitioning towards the nascent RedCap standards—and Wi-Fi evolving rapidly into Wi-Fi 7 adoption cycles particularly among MSOs and enterprises [S21], Airgain's product pipeline aligns strategically with these trends.

The Lighthouse platform secured pivotal FCC certification in September 2025 clearing regulatory hurdles for U.S.-based cellular repeaters deployment—a critical gatekeeper status that enables marketing to tier-one mobile network operators (MNOs) [N1][S4].

Simultaneously engaging MNOs alongside system integrators via structured enablement programs—covering installation training and technical certification—facilitates smoother rollouts across enterprise venues such as campuses or stadiums where private LTE/5G networks are expanding coverage needs economically.

In automotive applications — specifically fleet electrification and real-time telematics — AirgainConnect Fleet meets growing demands for remote diagnostics and route optimization leveraging low-latency simultaneous multi-band connectivity paired with embedded GNSS functions [S21].

Such embedded products benefit from stringent carrier-grade features like automatic gain control and echo cancellation essential in high-noise vehicular environments.

Continued partnerships with key ODMs accelerate time-to-market while AI-driven enhancements promise ongoing performance optimizations via firmware-over-the-air updates supporting adaptive beamforming — features that carriers increasingly require for certification scalability [S12][N3].

Operational Risks and Execution Challenges in Scaling System Solutions

The shift from components towards integrated wireless systems inherently escalates operational complexity—introducing risks linked to product development timelines extending due to tight coordination across hardware-software-cloud strata.

Airgain outsources manufacturing predominantly across Vietnam, China, Taiwan, Mexico,and the U.S., cultivating long-term relationships with contract manufacturers (CMs) who also procure critical semiconductor components from limited suppliers subject to global scarcity pressures [S15][S17]. This reliance exposes Airgain to potential supply chain disruptions amplified by geopolitical tensions surrounding trade policies affecting China-U.S.-Mexico relations [S10].

Strategic alliances aim to offset such risks; however failure or delay on partner performance affects time-to-market critically given aggressive competition from Asian manufacturers offering cost-competitive but less certified alternatives eroding addressable market share [S18][S24].

Furthermore extensive IP enforcement efforts struggle against counterfeit products entering markets leading to reputational damage risks despite an IP portfolio exceeding three hundred patents that provide defensive walls enabling premium pricing strategies [S16][S23].

Execution risk also emerges when aligning complex product certifications with diverse carrier requirements globally requiring sustained channel enablement efforts through training programs designed for system integrator familiarity enabling consistent quality deployments at scale [S4][N2].

Capital Structure, Liquidity, and Returns: A Focus on ROE and Cash Flow Dynamics

Airgain maintains a solid liquidity stance evidenced by current assets nearly double current liabilities (~$25.76M vs $12.98M) yielding a ~1.98 current ratio that affords operational flexibility despite persistent earnings deficits accelerating accumulated losses over $93 million USD through FY2025 [F1][S5].

Yet continued operating losses reflect difficulty translating system integration investments into positive returns; net income deterioration tempers potential ROE trajectories which stands near negative 22.7% given net loss versus shareholder equity [$6.43M loss / $28.29M equity] for calendar year ended December 31st 2025 [F1].

Negative free cash flow approximates $1.28 million driven by marginally negative operating cash flows offset slightly by subdued capital expenditure ($166K) aligned with outsourcing manufacturing rather than fixed asset intensity means capital commitments remain low but recurring operational burn sustains liquidity pressure absent profitable scale-up or external financing events historically not evidenced post-2019 buyback cessation trends reflecting conservative capital deployment philosophies amid transformation uncertainty [F1][S5].

No declared dividend payments or recent share repurchases indicate capital allocation priorities favor reinvestment into R&D projects targeting emerging wireless technologies including AI-powered antenna tuning improvements underpinning future competitive differentiation initiatives across enterprise and automotive segments [S12][F1].

What to Watch: Future Milestones and Sector-Specific Trends Affecting Airgain

In the absence of formal forward guidance highlighted by management disclosures during Q4 FY2025 earnings calls ([N1]), stakeholders should monitor several key indicators:

- Progression of new customer deployments for Lighthouse repeaters especially post-U.S. FCC certification which unlocks expanded addressable markets alongside validation by tier-one operators.

- Expansion of carrier certifications not only domestically but internationally aiming at standardization essential for broader commercial acceptance.

- Adoption rates for AirgainConnect Fleet within automotive OEM programs as electrification trends heighten demand for connected vehicle data solutions.

- Strategic broadening of channel partner networks coupled with system integrator enablement effectiveness impacting deployment rhythm.

- Market responses relative to emerging satellite-to-cellular hybrid connectivity solutions where Airgain’s multi-band antennas could secure advantage if successfully integrated into hybrid architectures.

- Quarterly revenue stability or inflection as measured against recent volatility which would signal material market traction or persistent execution lapses respectively.

- Competitive dynamics including price pressures stemming from Asian integrated competitors lacking traditional certifications but benefiting from lower cost structures necessitating continuous innovation cycles.

These variables collectively determine Airgain’s trajectory towards sustainable profitability balancing its pioneering technology integration ambitions against tight operational constraints.[N3][N2][S1]

Disclaimer: This analysis is intended solely for informational purposes based on publicly filed documents and recent news transcripts without providing investment advice or recommendations of any kind.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments