Atlantica Inc’s Search for Sustainable Operations Amid Financial Constraints

Atlantica Inc remains a shell company facing severe liquidity challenges as it seeks a viable business combination to drive future growth.

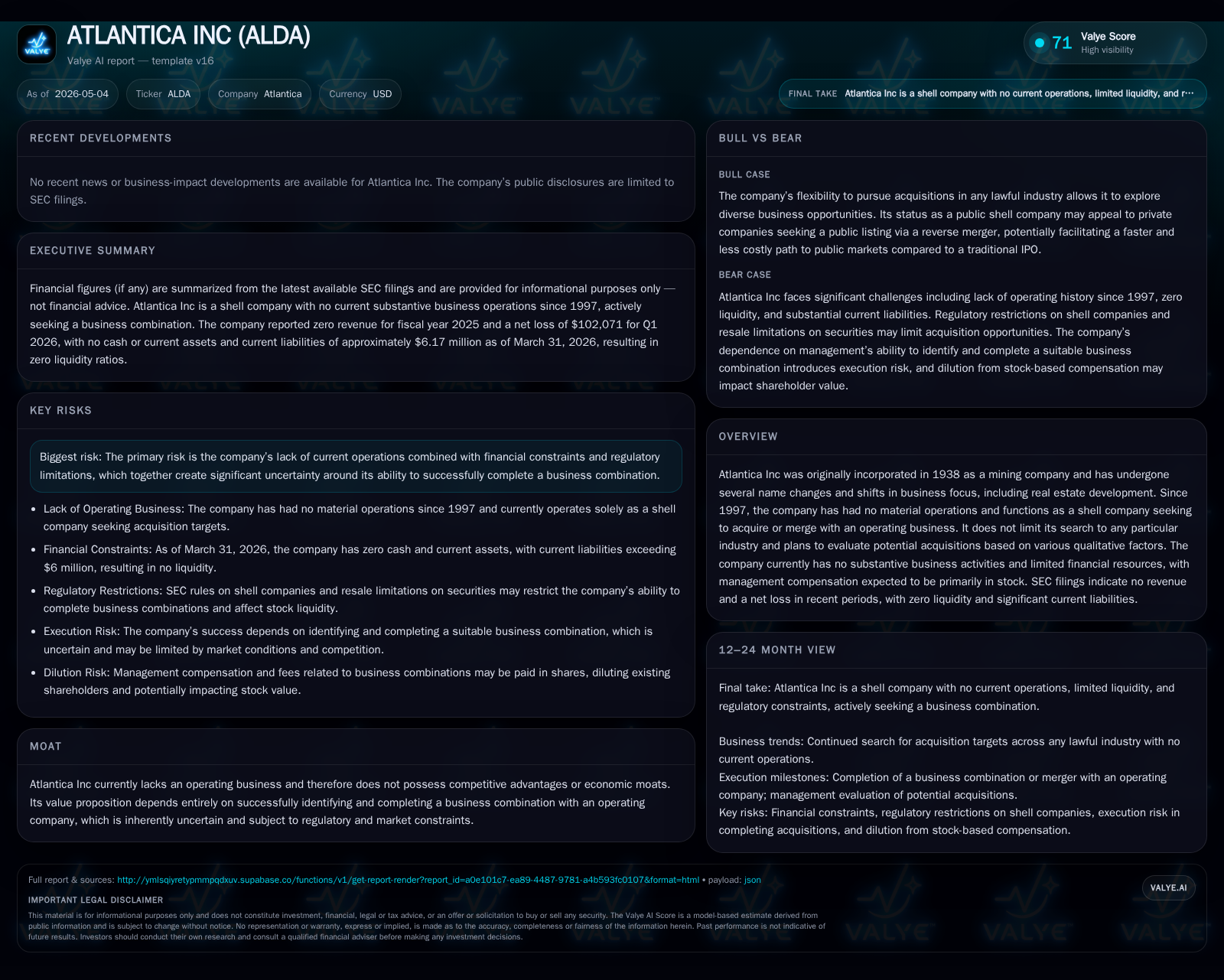

As of the first quarter of 2026, Atlantica Inc continues to operate without revenue or active business operations, maintaining a status as a publicly traded shell company. The latest quarterly filing underscores acute financial constraints including zero current assets against multi-million dollar liabilities, which presents a critical barrier to executing its acquisition-driven business strategy. Historically rooted in mining and real estate, the company now depends entirely on identifying and closing an operating business combination to realize value. This analysis explores the implications of its financial standing, structural risks, and strategic outlook given these constraints.

Latest Quarterly Filing Highlights and Operational Status

The most recent quarterly filing dated May 4, 2026 (covering the period ended March 31, 2026) reconfirms Atlantica Inc’s status as a non-operating entity with no reported revenues or active business operations [S2]. The company reported zero current assets juxtaposed against approximately $6.17 million in current liabilities, yielding a current ratio of zero—a stark indicator of liquidity risk and near-term solvency concerns [F1]. This financial snapshot signals that Atlantica lacks the working capital needed to meet its immediate obligations without outside financing.

This absence of an operating business means that the company’s expenses predominantly relate to administrative overhead rather than any core commercial activity [S2]. The filing notably omits any discussion of impending acquisitions or transaction progress, highlighting continued operational inertia.

Corporate Evolution: From Mining Origins to Present Shell Company

Founded in 1938 under Utah law as Red Hills Mining Company, Atlantica Inc originally operated within mining sectors before undergoing several rebrandings and shifts in focus over ensuing decades [S1]. By 1971, it transitioned into real estate development but ceased significant operations by 1990. Efforts in subsequent years focused mainly on restructuring capital and management changes rather than substantive commercial activity.

Since at least the late 1990s, Atlantica has functioned effectively as a shell company—publicly listed yet devoid of operating subsidiaries or revenue-generating ventures [S1]. This historic context illustrates why no competitive positioning or moats currently exist: Atlantica holds no proprietary technology, brand equity, or customer relationships within any industry sector.

Business Model Analysis: No Current Operations, Acquisition-Driven Strategy

Atlantica’s business model revolves exclusively around identifying and completing a "business combination" or acquisition that would constitute the foundation for future operations [S1][S2]. Without ongoing revenues or products/services to market, the company relies on management efforts to source potential targets across any industry sectors.

Given severe cash flow constraints highlighted in Q1 2026 filings, management compensation plans are anticipated to be fulfilled primarily via stock issuances rather than cash payments [S1]. This approach implies shareholder dilution risk which could complicate efforts to raise capital or incentivize executive talent without clear acquisition success.

Administrative costs continue despite inactivity, creating operating losses and financially burdening the company absent a transactional event. The absence of identified acquisition candidates within disclosures contributes further uncertainty around timing and strategic direction.

Sector and Competitive Position: Lack of Moat, Reliance on Successful Acquisition

In its current state, Atlantica holds no economic moat nor competitive advantages typically associated with operating businesses such as proprietary assets or scale economies. Its valuation is entirely contingent upon executing a successful acquisition that can generate sustainable cash flow.

From an industry perspective, this places Atlantica outside conventional competitive frameworks; analysis shifts from comparing product lines or market share toward assessing management’s capability and market conditions enabling deal completion. The risk profile is elevated due to inherent execution uncertainties common among shell entities attempting transformative mergers.

Growth Opportunities and Strategic Considerations

Growth prospects are entirely dependent on consummating one or several business combinations that can quickly establish operating scale. Management holds latitude to pursue companies in varied sectors; however, limited available resources restrict bidding power and negotiation leverage [S1].

Potential target evaluation criteria are likely qualitative rather than quantitative given current disclosure—factors such as sector attractiveness, synergy potential, manageable capital requirements, and rapid operational ramp-up are probable priorities.

Despite flexible sector options theoretically expanding opportunity sets, practical growth is inhibited by scarce liquidity leading to possible prolonged timelines before value creation becomes feasible.

Risks and Distinct Constraints Stemming from Financial and Regulatory Issues

Atlantica faces distinct risks rooted chiefly in its precarious balance sheet. Zero current assets against over $6 million in short-term liabilities creates acute insolvency risk absent external financing [F1][S2]. This scenario creates pressure on management both to secure capital swiftly and complete an accretive acquisition.

Regulatory scrutiny commonly intensifies for shell companies attempting mergers post-2000s reforms designed to protect public investors. These factors can delay deal approvals or introduce compliance costs.

Shareholder dilution resulting from expected stock-based executive compensation amidst recapitalization efforts poses additional governance concerns by potentially eroding existing equity stakes [S1]. Together, these constraints significantly temper the feasibility and timing of successful transformation initiatives.

Upcoming Catalysts and Key Milestones to Monitor

Currently there are no public disclosures regarding imminent merger agreements or financings with timeline targets [S2]. Therefore, future catalysts will likely emerge through subsequent SEC filings that might reveal:

- Letters of intent or definitive agreements for acquisitions,

- Capital raising activities easing liquidity constraints,

- Changes in senior management aiming at repositioning,

- Any updates reflecting changes in business strategy or operational progress.

Absent such material developments, monitoring quarterly reports remains essential for early signals of strategic momentum reversal.

Current Financial Snapshot: Liquidity and Balance Sheet Realities

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Current assets | 0 USD | |

| 2025-12-31 | ||

| Current liabilities | $6mm | |

| 2026-03-31 | ||

| Current ratio | 0x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value (USD) |

|---|---|

| Cash & Equivalents | 0 |

| Current Assets | 0 |

| Current Liabilities | 6,174,191 |

| Current Ratio | 0 |

This table encapsulates Atlantica’s fragile financial footing at the close of Q1 2026: no liquid assets exist to service pressing liabilities totaling over $6 million [F1][S2].

Disclaimer: This analysis is based solely on public SEC filings and authoritative data sources up to May 2026. It does not constitute investment advice. Given Atlantica Inc’s status as a non-operating shell with material financial constraints, any prospective developments carry high uncertainty requiring careful scrutiny by stakeholders.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments