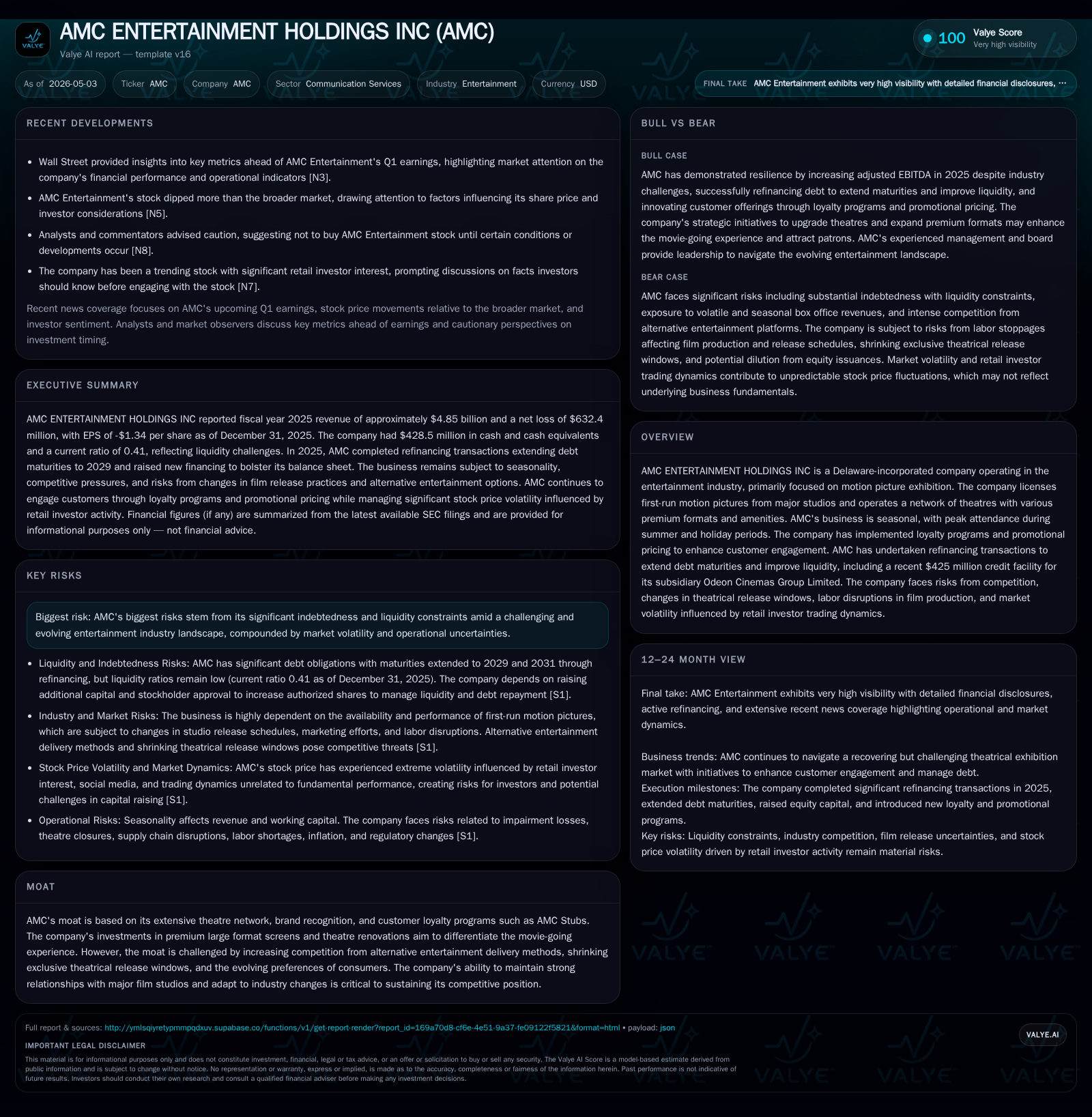

AMC Entertainment Restructures Debt and Battles Industry Headwinds in 2026

AMC's recent refinancing extends debt maturities amid evolving theatrical market dynamics and operational challenges.

AMC Entertainment executed a major refinancing in April 2026, securing $425 million in term loans for its Odeon Cinemas subsidiary with maturity extended to 2031 and quarterly amortization starting mid-2026. This move follows previous debt restructurings aiming to manage a heavy leverage load exceeding $4 billion as of late 2025. AMC's business continues to hinge on premium theatrical exhibition offerings, loyalty initiatives, and navigating the pressures of shrinking exclusive release windows, intensified competition from streaming, and labor disruptions affecting content flow. While growth drivers include upgrading premium large-format screens and customer engagement programs, significant risks remain tethered to liquidity constraints and industry unpredictability.

Recent Operating Update Highlights: Refinancing & Strategic Moves

AMC Entertainment Holdings Inc unveiled a pivotal development in its capital structure with the closing of the Odeon Credit Agreement on April 17, 2026. The agreement arranged $425 million in term loans for Odeon Finco PLC — a direct subsidiary of the Odeon Cinemas Group Limited and an indirect subsidiary of AMC itself — maturing in April 2031 [S3]. The facility bears a fixed interest rate of 10.50% and includes amortization on principal at a rate of 1.00% per annum payable quarterly starting July 15, 2026.

This financing incrementally extends AMC’s debt maturities beyond prior refinancings in 2024 and 2025 which restructured existing senior secured term loans and second lien notes into instruments extending out to 2029 [S2]. These sequential refinancing moves respond directly to managing the company’s elevated leverage position against backdrop of uneven operating cash flows within a pressured theatrical exhibition market.

Further complicating the capital structure status quo is AMC's significant share count dilution over recent years—surpassing half a billion additional common shares issued since early 2020 through multiple mechanisms including at-the-market sales, convertible preferred stock conversions, note exchanges, and equity grants [S2]. This shift reflects ongoing equity capital raises undertaken to bolster liquidity while navigating persistent losses.

Taken together, AMC’s recent refinancing actions underline an urgent imperative to bolster liquidity horizons amidst volatile macroeconomic conditions and evolving sector fundamentals.

AMC’s Business Model: Premium Exhibition and Customer Engagement

At its core, AMC operates as a network-based motion picture exhibitor predominantly licensing first-run releases from major Hollywood studios under timed theatrical distribution agreements [S1]. Revenue derives principally from ticket sales but is increasingly supplemented by concessions and premium format offerings such as IMAX or Prime Large Format (PLF) screens designed to justify higher pricing tiers.

Customer retention strategies revolve heavily around the AMC Stubs loyalty program encompassing tiered memberships that incentivize repeat visits through rewards, discounted concessions, and advance ticket access [S1]. Seasonality plays a discernible role with peak attendance during summer blockbuster months and holiday periods replicating historic patterns albeit tempered by changing consumer entertainment preferences.

Innovation in customer experience—seat upgrades, sight and sound enhancements—and pricing promotions are integral to retaining competitive edge against at-home streaming alternatives which continue fragmenting traditional audience pools [S1]. This hybrid push-pull dynamic challenges AMC to continuously refine value propositions tied closely to physical venue ambiance beyond simple movie viewing.

Industry Structure: Competition, Release Windows, and Consumer Trends

The global theatrical exhibition industry remains highly competitive with multiple chains vying regionally alongside entrenched streaming platforms impacting consumer habits. Increasingly abbreviated exclusive theatrical release windows—driven by studios’ strategic shifts toward rapid digital availability—erode traditional box office revenue share for exhibitors like AMC [S1][S2].

Negotiation power between distributors (major studios) and exhibitors further modifies release timing impacting attendance predictability. The theater operators also grapple with geopolitical regional variances influencing capacity utilization rates across their networks.

Compounding these issues are labor disputes affecting film production schedules encountered over recent years leading to delayed slate rollouts thereby compressing flow of new content—a material risk for chain drive traffic consistency [S1]. Additionally emerging technologies such as AI-generated films pose unpredictable impacts on audience reception though material effects remain speculative.

Drivers of Growth: Premium Formats, Loyalty Programs, and Market Recovery

AMC’s approach to growth focuses on expanding penetration of premium large-format screens which command higher ticket prices relative to standard presentations—a critical lever in improving revenue per patron while aligning with consumer demand for differentiated experiences [S1][N3].

Augmentation of loyalty membership uptake via the AMC Stubs program supports recurring revenue streams as frequent visitors disproportionately drive concession sales margin enhancements.

Post-pandemic recoveries internationally especially within Europe (Odeon Cinemas Group being key operator) offer incremental upside potential as local markets normalize foot traffic alongside new blockbuster releases deferred by prior production strikes.

Macroeconomic factors influence discretionary spending patterns; thus economic stability enhances consumer willingness to engage in nonessential spending such as movie attendance providing structural rather than purely cyclical tailwinds for growth.

Risks and Constraints: Leverage, Industry Volatility, and Content Supply

AMC carries substantial net debt approximating $3.6 billion after cash offsets as of December 31, 2025 [F1], coupled with a notably weak current ratio around 0.41 indicating tight near-term liquidity coverage [F1]. The newly established Odeon Term Loans’ high fixed interest rate at 10.5% further stresses cash flow burden particularly with scheduled quarterly amortizations starting mid-2026 [S3].

Fiscal flexibility remains constrained despite refinancing efforts given covenant restrictions limiting operational maneuverability detailed in recent SEC filings [S2]. Concurrently market volatility influenced by retail investor trading dynamics injects uncertainty into AMC’s equity valuation trajectory complicating future capital raises.

Operational risks persist including further labor stoppages disrupting film supply chains negatively impacting release cadence essential for sustained box office inflows [S1][S2]. Competitive pressures from expanding streaming ecosystems accelerate audience fragmentation exacerbating subscriber churn versus theater visitation frequency.

Ongoing dilution from equity issuances aimed at alleviating leverage tension also dilutes shareholder voting power undermining return prospects.

Key Near-term Catalysts and Monitoring Points

Key performance indicators to observe closely include periodic operating revenue progression across domestic U.S. theatres coinciding with anticipated normalization post-content strike impacts reported over prior years [N3][S3].

Management statements concerning realization of projected synergies from strategic initiatives such as premium format rollouts or loyalty program expansions will illuminate execution effectiveness.

Scheduled stair-step repayments under the new Odeon credit facility beginning July 15, 2026 warrant monitoring for effects on liquidity versus operating cash generation balance [S3].

Evaluating Odeon Cinemas Group operational results within European markets provides insight into international diversification resilience amid shifting consumer trends.

Finally, updates on studio release calendars reflecting any continued labor issues or shifts in windowing policies will materially impact cycle visibility given their influence over box office volumes.

Financial Snapshot: Leverage Profile and Liquidity Position

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $429mm | |

| 2025-12-31 | ||

| Total debt | $4.0bn | |

| 2025-12-31 | ||

| Net debt | $3.6bn | |

| 2025-12-31 | ||

| Current assets | $731mm | |

| 2025-12-31 | ||

| Current liabilities | $1772mm | |

| 2025-12-31 | ||

| Current ratio | 0.41x | |

| 2025-12-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value (USD) |

|---|---|

| Revenue | $4.85 billion [F1] |

| Net Income | -$632.4 million [F1] |

| Cash & Equivalents | $428.5 million [F1] |

| Total Debt | $4.02 billion [F1] |

| Net Debt Approximate | $3.60 billion [F1] |

| Current Ratio | 0.41 [F1] |

The company’s current ratio well below unity reinforces short-term working capital tightness necessitating continued prudent management of cash flows amidst volatile operating conditions [F1]. These financial metrics underscore the strategic imperative behind repeated refinancing transactions aimed at lengthening maturities while attempting modest deleveraging through selective equity raises as previously indicated [S2][S3].

This analysis synthesizes public regulatory disclosures without constituting investment advice or explicit forecasts. Observers should consider inherent sector cyclicality compounded by micro-structural shifts when evaluating AMC Entertainment Holdings Inc's operating context going forward.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments