Versigent's Strategic Course Post-Spin-Off: Operational Shifts and Competitive Standing

Versigent PLC’s inaugural standalone quarterly filing reveals critical restructuring efforts and financial positioning following its April 2026 spin-off from Aptiv.

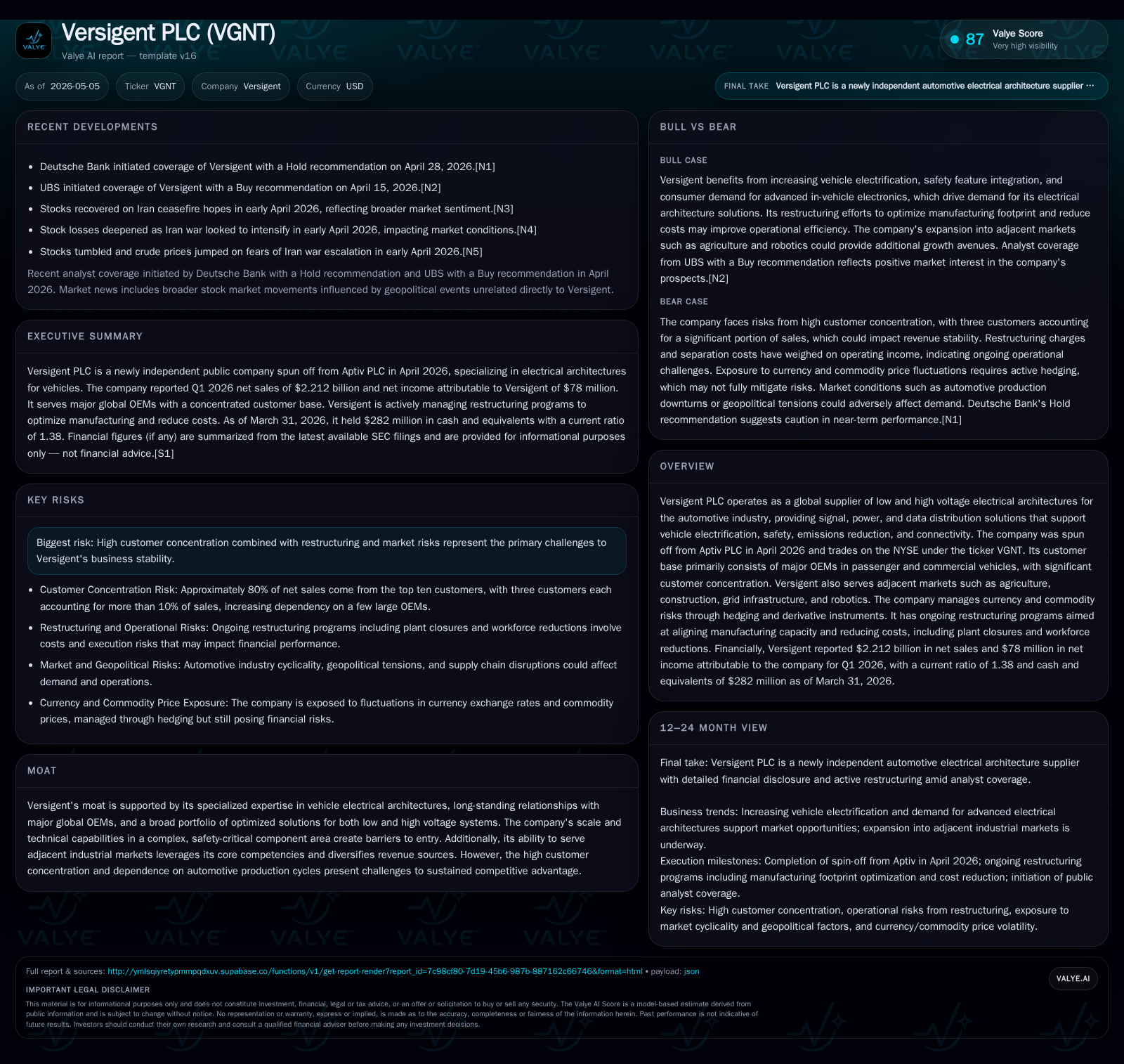

Versigent PLC’s first independent quarterly report since its April 2026 spin-off details elevated restructuring costs aimed at optimizing manufacturing capacity and trimming costs. The company operates as a global supplier of complex low- and high-voltage electrical architectures to major automotive OEMs, with a concentrated customer base and significant exposure to global vehicle electrification trends. Versigent’s competitive moat hinges on its technical expertise, scale, and long-standing OEM relationships, yet its high leverage and customer concentration underscore notable risks. Close monitoring of restructuring outcomes, order intake, and margin trajectories will be key as Versigent establishes standalone operational momentum.

Initial Operating Update Following Spin-Off

Versigent PLC completed its spin-off from Aptiv PLC on April 1, 2026, becoming an independent publicly traded company under the ticker VGNT. The subsequent May 5, 2026 Form 10-Q filing represents Versigent’s first quarterly disclosure as a standalone entity. This filing unpacks early operational realities including revenue recognition nuances and sharp increases in restructuring costs — specifically $26 million incurred in Q1 2026 compared to $18 million a year earlier despite the carve-out nature of the historical financials [S2].

The increased restructuring liability reflects intensified efforts toward realigning the manufacturing footprint through plant closures and workforce reductions aimed at optimizing capacity for evolving industry demands. Versigent applies a conservative allowance approach on revenue recognition, accounting for sales incentives and customer payments as direct revenue reductions at the point of sale [S2]. This reflects necessary prudence given customer negotiations that may impact realized consideration.

Importantly, the company operates as a single segment encompassing both low voltage (LV) and high voltage (HV) electrical architectures [S9]. Its carve-out financial statements incorporate allocations of certain costs from the former Parent Aptiv but caution that these may not fully represent standalone cost structures going forward.

Versigent’s Business Model and Product Value Proposition

Versigent’s fundamental business is supplying complex electrical distribution solutions that include signal, power, and data architectures critical for modern vehicle platforms. These architectures underpin critical functions such as vehicle electrification — supporting electric powertrains — enhanced safety systems like ADAS wiring harnesses, emission controls via optimized power routing, and integrated connectivity enabling infotainment and telematics capabilities, [S28].

Revenue generation flows primarily through contracts with major global original equipment manufacturers (OEMs) producing passenger cars, commercial trucks, vans, buses, and off-highway vehicles. Revenues hinge on volume delivery as automakers ramp or taper production schedules alongside pricing agreed upfront or adjusted via negotiated purchase orders [S2].

Beyond automotive, Versigent leverages its core competencies to penetrate adjacent industrial markets such as agriculture equipment (e.g., tractors with complex wiring harnesses), construction machinery, grid infrastructure components requiring reliable power distribution networks, off-grid power storage systems, and expanding robotics applications, [S28]. This diversification could blunt demand cyclicality tied strictly to passenger vehicle production.

Product quality demands are exacting given safety-critical applications; switching costs remain high due to the engineering complexity and certification hurdles intrinsic to vehicle electrical systems.

Position in the Electrical Distribution Industry and Competitive Dynamics

Versigent's specialized focus on both low- and high-voltage vehicle electrical architectures distinguishes it in a niche requiring deep technical expertise. This expertise stems from its legacy within Aptiv PLC’s Electrical Distribution Systems business. Its long-standing OEM partnerships grant it preferential access to evolving vehicle platform programs globally.

The industry presents high entry barriers: safety-critical compliance requirements, extensive qualification processes specific to each automaker platform, supply chain integration complexity for key raw materials (copper wiring bundles, connectors), plus volatility in commodity inputs necessitating derivative hedging strategies documented by Versigent, [S21].

Versigent faces significant customer concentration risk; three customers accounted for nearly half of it sales in Q1 2026 (18%, 17%, and 13% respectively) while the top ten clients represent approximately 80% of total net sales [S16]. This reliance magnifies exposure to OEM production cycle downturns or program shifts.

Despite this concentration risk, deep collaborative design relationships provide some protective moat by embedding Versigent’s architectures into increasingly software-defined vehicles where synchronized hardware-software integration serves as a switching barrier.

Key Drivers for Future Growth

Structural growth catalysts reside largely in accelerating industry shifts toward electrified vehicles globally—both passenger electric vehicles (EVs) and commercial fleet electrification increase demand for high voltage architectures capable of handling traction power safely and efficiently, [N2].

Further growth is expected from deeper signal data integration across connected vehicle domains—driving need for advanced wiring solutions tailored for bandwidth-intensive sensor arrays (LIDAR/RADAR), infotainment systems—and extending into adjacent industrial sectors adopting electrified machinery designs.

Management's ongoing manufacturing rationalization aims to drive margin expansion by improving capacity utilization and trimming legacy fixed overhead—particularly important during scale-up phases for new EV platforms [S7].

Visibility into order intake post-spin-off remains limited but evolving independent sales channels beyond residual Aptiv-related flows are expected to reveal growth capture ability over coming quarters [N2]. Success will depend on leveraging technical portfolio breadth while addressing evolving customer preferences in rapidly transforming automotive value chains.

Risks, Challenges, and Watchpoints

The primary risk vector is customer concentration: heavy dependency on a handful of OEMs elevates volume volatility risks tied directly to vehicle production cycles impacting revenue predictability [S16]. This risk coexists with competitive pressure from alternative suppliers potentially offering integrated electronic architecture solutions or newer lightweight material technologies.

Restructuring execution uncertainty clouds near-term earnings quality: escalating charges ($26 million Q1 alone) must translate into sustainable cost savings without undue disruption or loss of critical manufacturing know-how [S7], [S16]. Inadequate execution risks margin erosion or impaired supply reliability.

Raw material commodity price fluctuations impose input cost pressures notwithstanding currently employed hedging strategies; failure of these instruments can compress margins unexpectedly, [S21].

Sales incentives recognized as revenue deductions indicate competitive dynamics requiring ongoing micromanagement lest discounting pressure erode topline growth sustainability [S2].

Upcoming Milestones and Monitoring Indicators

Key near-term milestones focus around: tracking restructuring plan progress including reduction in termination benefit liabilities; transparency around standalone order backlog levels; margin improvement trends reflecting operational leverage gains; successful navigation of credit facility covenants; reduction or stabilization in gross leverage ratios; evolution of customer payment/incentive patterns; expanding revenues from adjacent industrial markets beyond traditional automotive base [S2], [S3].

As an emerging standalone company post-spin-off trading independently since April 2026, successive quarterly filings will be critical barometers evidencing Versigent’s ability to convert strategic intents into stable profitable operations.

Latest Financial Snapshot and Capital Structure Highlights

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $282mm | |

| 2026-03-31 | ||

| Total debt | $2.14bn | |

| 2026-03-31 | ||

| Net debt | $1.86bn | |

| 2026-03-31 | ||

| Current assets | $3.15bn | |

| 2026-03-31 | ||

| Current liabilities | $2.28bn | |

| 2026-03-31 | ||

| Current ratio | 1.38x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value (USD millions) |

|---|---|

| Cash & Equivalents | 282 |

| Total Debt | 2141 |

| Net Debt | 1860 |

| Current Assets | 3146 |

| Current Liabilities | 2275 |

| Current Ratio | 1.38 |

| Operating Income (Q1) | 74 |

| Restructuring Expense | 26 |

Versigent reports operating income of $74 million alongside net income of roughly $78 million for Q1 ending March 31, 2026 [F1]. The company maintains liquidity evidenced by cash balances of $282 million versus current liabilities totaling approximately $2.275 billion yielding a current ratio near 1.38x indicative of measured working capital management amid significant current obligations [F1].

Total debt stands at $2.14 billion dominated by a combination of term loans due 2031 ($495 million net) plus senior unsecured notes due in 2031 ($789 million net) and 2034 ($788 million net), plus finance leases at $69 million net after issuance costs settled early in the year post-spin-off capitalizing $23 million in issuance fees related primarily to note offerings completed March 18, 2026 onwards [S6], [S7], [F1]. Letters of credit remain available offering contingent liquidity buffers if deployed under the committed revolving credit facility terms [S2]. Covenants impose leverage ratio ceilings beginning at maximum total leverage under Credit Agreement capped initially at approximately four times EBITDA tightening progressively over the next two years providing cost control impetus amid debt servicing obligations fine-tuned quarterly with floating interest expenses between ABR +0.25% up to margins approaching ~2% contingent on leverage banding metrics established contractually [S6], [S7]. Restructuring outlays significantly contributed approximately $26 million expenses reflecting severance provisions accrued against ongoing manufacturing footprint rationalization plans chiefly focused on Europe Americas operations closing certain plants without incurring additional exit costs recorded separately thus far in liabilities balance sheet reconciliations [S7], [S16]. Cash flow statements chart operating cash inflows moderate at $36 million constrained modestly by increased working capital build largely concentrated in accounts receivable principally owing from outside customers offset partially by payables management strategies with financing activities showing proceeds netting dividend payouts primarily reflecting corporate parent dividends proximal to spin-off completion date aggregate close to $1900 million showing equity structuring effects within cash flows reported primarily as net transfers related post-cutoff timing adjustments consistent with newly separated group financial relations transitioning from Aptiv-centric treasury model toward stand-alone governance frameworks [S17], [F1].

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments