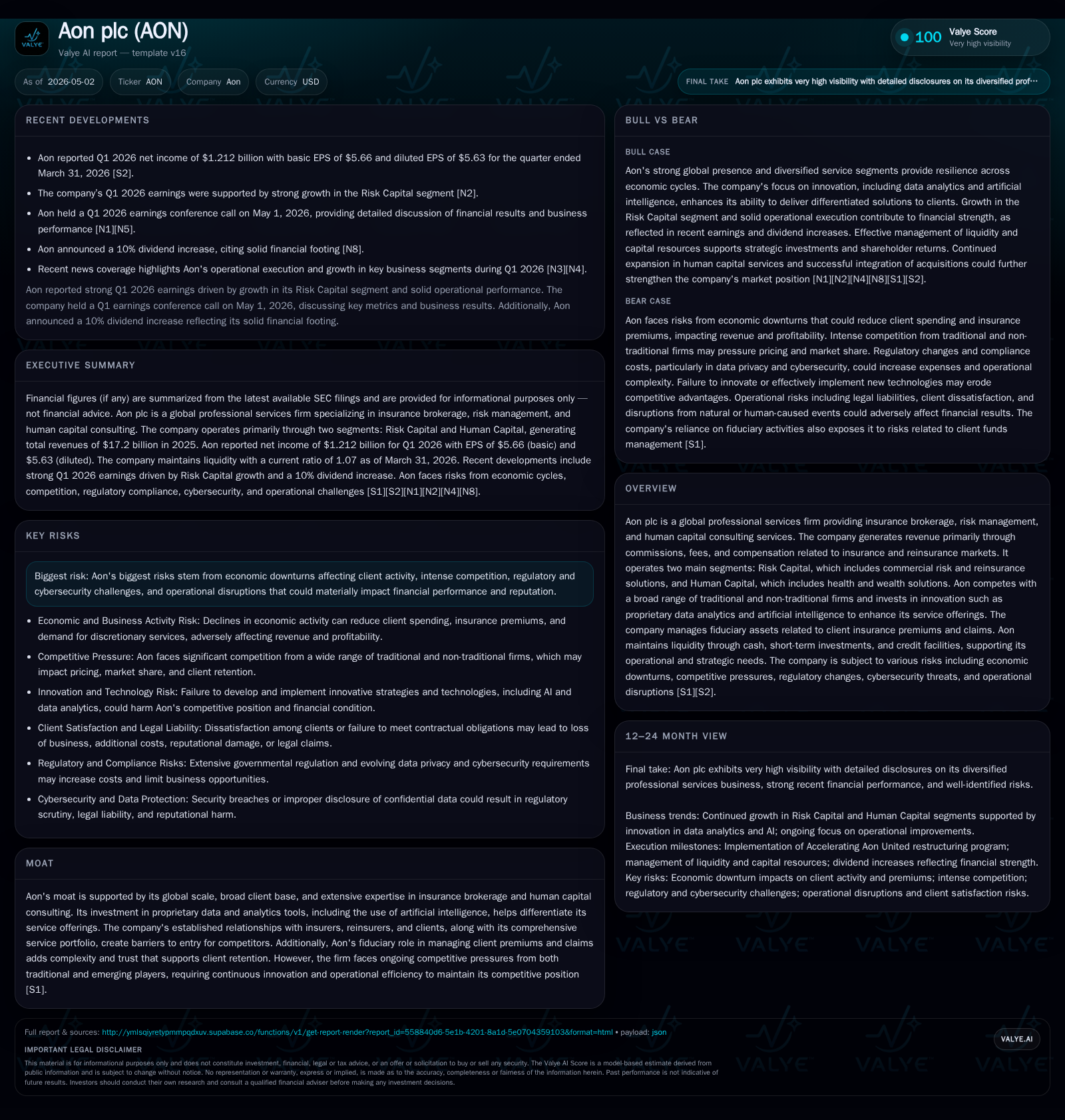

Aon’s Q1 Surge Highlights Risk Capital Momentum and Innovation Edge

Aon's latest quarterly report reveals robust growth in its Risk Capital segment, driven by innovation and strong client demand.

In its Q1 2026 filing, Aon plc reported solid revenue gains led by the Risk Capital business, reflecting continued momentum in commercial risk and reinsurance solutions. The company's investments in proprietary analytics and AI are enhancing its competitive moat amid a challenging industry landscape. While Human Capital consulting remains strategic, near-term pressure exists from wealth solutions. Regulatory risks and economic cyclicality persist, but Aon's diversified portfolio and global scale provide durable growth avenues. Upcoming milestones include contract renewals and technology deployments that will clarify sustained operational progress.

Key Takeaways from the Q1 2026 Operating Update

Aon's latest quarterly filing dated May 1, 2026 [S2] underscores a notable acceleration within its Risk Capital segment. Fueled by increased brokerage commission income from commercial risk solutions and reinsurance placements, revenue growth outpaced estimates as detailed in concurrent earnings analyses [N2], [N4]. This momentum reflects strong client demand for tailored risk mitigation amid persistent global uncertainties.

Operationally, the company highlighted enhancements through proprietary AI-powered analytics that sharpen risk pricing accuracy and improve client advisory capabilities — an initiative aligning with management’s stated strategy to differentiate through innovation [S2]. While Human Capital consulting services maintained stable contributions, some softness emerged within wealth solutions consistent with macroeconomic headwinds affecting discretionary advisory services [N8]. The filing notes ongoing cost disciplines even as certain elevated expenses linked to integration of recent acquisitions—most notably the NFP transaction—are being absorbed as part of long-term synergy realization.

The overall operating environment remains complex but Aon's robust execution in diversifying its revenue streams combined with heightened technology-driven insights supports a cautiously optimistic near-term outlook.

How Aon’s Business Model Drives Diversified Revenue Streams

Aon's revenue derives primarily from two complementary segments: Risk Capital and Human Capital [S1].

Risk Capital generates fees and commissions largely via brokering commercial insurance contracts and structuring reinsurance solutions. This segment benefits from clients’ increasing needs for sophisticated coverage against evolving risks such as cyber threats or climate-related exposures. The company acts as an intermediary between insurers, reinsurers, and clients while managing fiduciary assets representing premiums collected on clients' behalf.

Human Capital focuses on health and wealth consulting encompassing employee benefits administration, retirement plan advisory, and related actuarial services. Fee-based consulting here often builds stickiness due to complex regulatory requirements and trust built over long-standing client relationships.

Crucially, Aon integrates proprietary data analytics embedded with machine learning models that enhance risk assessment precision across both segments. This technological edge enables better client-specific solution customization while amplifying pricing power — a key competitive differentiator in this fragmented industry landscape.

Customer retention is supported by bundled offerings that entwine risk underwriting support with complementary human capital advisory, creating switching costs for clients wary of disrupting integrated service delivery. Furthermore, fiduciary responsibilities in managing premium flows foster trust essential for renewal stability.

Competitive Positioning and Industry Dynamics in Insurance Brokerage and Consulting

Within insurance brokerage and consulting networks, Aon competes with well-entrenched incumbents such as Marsh McLennan and Willis Towers Watson alongside nimble emerging entrants leveraging digital platforms [S1], [N14].

The barriers to entry are elevated due to:

- Extensive regulatory oversight imposing compliance hurdles;

- Trust-intensive fiduciary roles that require high service reliability;

- Proprietary data infrastructure supporting nuanced risk pricing.

Aon’s sizable global footprint confers scale advantages allowing cross-selling opportunities across geographies while spreading fixed IT infrastructure costs over a broad base.

Pressure points arise from evolving insurtech models promising enhanced customer engagement via technology which could erode traditional broker commissions if not countered effectively. Hence continuous investment in advanced analytical tools that integrate AI capabilities under the 'Accelerating Aon United' operational program is critical to maintain relevance [S2], [S1].

Additionally, regulatory complexity—ranging from data privacy laws affecting client information handling to evolving standards on insurance product disclosures—requires vigilant adaptation lest profitability suffers due to compliance costs or litigation exposure.

Growth Drivers: Technology Investment, Market Expansion, and Services Innovation

Aon's trajectory leans heavily on technological augmentation of its service offerings. Investments in AI-driven underwriting models empower more granular evaluation of emerging risks like cybersecurity exposures or niche verticals such as data-center property insurance—a fast-growing specialty line addressed explicitly in recent market commentary [N14].

Geographically, expansion into underserved markets coupled with strategic acquisitions (e.g., the recent NFP deal) broadens product access while enhancing net new business bookings.

Innovation also permeates Human Capital solutions through digitized employee benefit platforms enabling better engagement metrics and predictive health analytics supporting wellness programs — incremental drivers of customer retention amid dynamic workforce trends.

The rapid development of bundled risk-human capital packages presents cross-selling opportunities reinforcing stickier client relationships that sustain organic growth.

KPIs closely watched include organic revenue growth percentages within each segment backed by strong backlog visibility from contract renewals alongside margin improvement reflecting scale efficiencies from operational improvement initiatives.

Risks and Constraints: Economic Cyclicality, Competition, and Regulatory Challenges

Aon discloses multiple risks inherent to its operational model [S1], [S2], [S3]:

- Economic Sensitivity: Volatility influences clients’ decisions to purchase or renew insurance coverages especially in commercial lines which correlates strongly with business activity levels.

- Competitive Pressures: Both incumbent brokers aggressively defend share while digital disruptors introduce alternative distribution channels which may compress broker commission margins over time.

- Regulatory & Compliance Challenges: Increasing regulation heightens expense burdens; potential adverse outcomes from E&O claims pose reputational hazards.

- Cybersecurity Threats: As a repository of sensitive client data including premium management flows held fiduciarily, any breach could result in material financial loss or client attrition.

- Operational Execution: Realizing synergies from acquisitions like NFP largely depends on successful integration execution; failure could impair anticipated cost savings or revenue synergies.

Mitigation efforts revolve around sustained investment in innovation to differentiate products plus comprehensive compliance frameworks paired with crisis management protocols addressing cybersecurity resilience.

Upcoming Catalysts and What Investors Should Monitor

The roadmap ahead calls for tracking several milestones:

- Quarterly earnings updates will provide indications whether Risk Capital momentum sustains beyond initial quarters post-integration stages [N1], [S2].

- Contract renewal cycles particularly within reinsurance brokerage where multi-year deals predominate will reveal booking rates reflective of underlying demand dynamics.

- Progress reports on 'Accelerating Aon United' program focusing on digital transformation outcomes including operating margin improvements serve as execution barometers.

- Advances in rollout of specialty insurance products such as expanded data-center coverage could open higher-margin niches underpinning differentiated growth pathways [N14].

- Regulatory developments including tax reforms or changes impacting fiduciary liabilities represent external factors to monitor given their potential impact on margins or legal exposure.

Overall evidence points toward gradual strengthening validated by clear KPIs linked to technology adoption rates paired with market penetration metrics defining share gains versus competitors.

Latest Financial Snapshot: Liquidity, Leverage, and Profitability

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $1178mm | |

| 2026-03-31 | ||

| Total debt | $15.4bn | |

| 2025-12-31 | ||

| Net debt | $14.2bn | |

| 2025-12-31 | ||

| Current assets | $26.2bn | |

| 2026-03-31 | ||

| Current liabilities | $24.5bn | |

| 2026-03-31 | ||

| Current ratio | 1.07x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

Liquidity remains robust aided by over $1 billion cash reserves supplemented by committed credit facilities totaling $2 billion unused as of year-end [F1], supported by compliance with all debt covenants reported at last annual filing [S7]. The net debt position reflects leveraged acquisitions but is balanced by strong operating cash flows underpinning capital return programs including dividends declared at $0.745 per share quarterly [S4], [S6]. Margins have room for expansion contingent upon integration efficiencies realized through operational improvement initiatives noted previously.

This analysis is based exclusively on disclosed SEC filings and publicly available information as of May 2026. It does not constitute investment advice or endorsement.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments