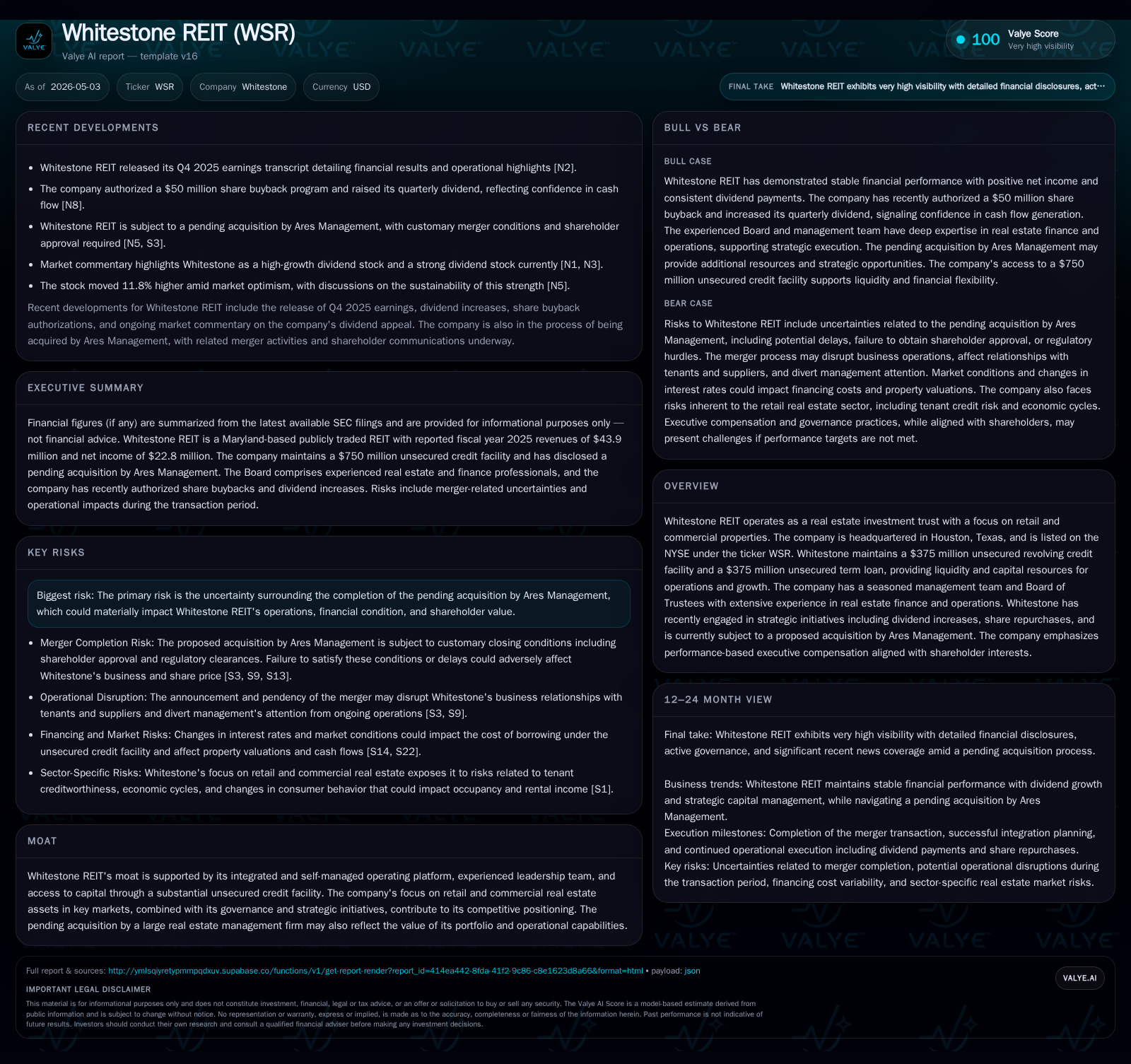

Whitestone REIT’s Strategic Transition Anchored by Pending Ares Acquisition and Capital Flexibility

Whitestone REIT advances toward a $19/share acquisition by Ares Management amid robust liquidity and active capital management.

Whitestone REIT’s latest disclosures underscore a transformative pivot with a definitive merger agreement to be acquired by Ares Real Estate Management. This deal crystallizes at a $19 per share cash consideration, pending shareholder approval, and represents a significant liquidity event. Operationally, Whitestone maintains strong liquidity via a substantial unsecured revolving credit facility and term loan that underpins ongoing portfolio management and growth initiatives, including dividend enhancements and share repurchases. The company’s integrated self-management approach combined with experienced leadership fortifies its competitive position within retail and commercial property markets. However, the pending acquisition introduces execution risk and near-term operational uncertainties.

Recent Operating Update: Definitive Merger Agreement Signals Strategic Inflection

Whitestone REIT’s most consequential development is the April 8, 2026 announcement of a definitive merger agreement under which it will be acquired by investment vehicles affiliated with Ares Real Estate Management ("Ares Funds") at a fixed cash price of $19.00 per share [S3], [S7], [S18]. This transaction is structured as a merger involving both the REIT common shares and Operating Partnership units, with conversion into cash consideration. The completion remains subject to customary closing conditions such as shareholder approval, regulatory clearance, and absence of material adverse changes to Whitestone’s business.

The update filing also notes that Parent has secured committed financing blending equity contributions from Ares affiliates with third-party debt facilities adequate to fund the transaction closing [S3], ensuring financial backing to consummate the acquisition. Whitestone’s Board unanimously recommends shareholder approval of the deal anticipating strategic value crystallization [S18].

This development materially shifts Whitestone’s near-to-medium-term strategic context by positioning it for privatization post-transaction, cessation of public equity trading, and deregulatory relief under exchange listing rules [S11]. The company deferred its annual meeting while this process unfolds, reflecting prioritization of shareholder votes on the transaction.

Business Model: Integrated Self-Managed Retail-Centric REIT Offering

Whitestone REIT operates primarily as an owner and manager of retail and commercial real estate assets concentrated in key U.S. markets [S1]. Its business model centers on acquiring, managing, leasing, maintaining, and selectively developing properties focused predominantly on shopping centers anchored by essential services such as grocery stores or daily needs retailers — a segment designed to deliver stable occupancy through resilient tenant demand.

A distinctive strength lies in Whitestone’s integrated self-management platform where in-house teams handle leasing, operations, capital improvements, tenant relations, and asset management functions rather than outsourcing these activities [S1]. This model purportedly gives greater operational control, cost discipline, flexibility in capital deployment decisions, and enhanced responsiveness to tenant needs.

Revenue is principally generated from lease rentals paid by tenants which are subject to contractual obligations often containing base rent plus percent rent structures tied to sales performance. Revenue levels are driven by occupancy rates across properties, rental rate escalations embedded within leases (indexed frequently to inflation or market resets), lease renewals or new tenant acquisitions, as well as lease term durations that support recurring income predictability.

Margins can vary depending on property type mix (retail vs commercial), geographic location premium, tenant credit quality affecting collections risks, and operating expense efficiency leveraged by management control. Additionally, Whitestone generates fees associated with its Operating Partnership units owned by investors but does not heavily rely on fee-based revenue streams compared to some externally managed REITs.

Industry Structure and Competitive Position

Whitestone competes within the broader sector of publicly traded equity real estate investment trusts specializing in retail property domains amid evolving macroeconomic dynamics impacting brick-and-mortar retail footprint demand.

Unlike many larger retail-focused REITs that concentrate heavily on malls or lifestyle centers vulnerable to e-commerce substitution risks, Whitestone's portfolio tilts towards neighborhood centers anchored by grocery or essential service providers offering more defensive cash flow durability [S1]. This focus highlights resilience features within an industry facing sector-wide challenges related to tenant bankruptcies or downsizing.

The company leverages its self-managed platform for nimble portfolio responses to leasing challenges while competing against peers who outsource property management but may benefit from scale advantages provided by larger asset bases.

Capital access is another competitive edge: Whitestone maintains an unsecured credit facility totalling $750 million split evenly between revolving credit ($375 million) and a term loan ($375 million), with maturity horizons extending through late-decade periods [S12], [F1]. Interest rates are anchored around Term SOFR plus a margin correlated with leverage profile offering efficient cost of capital options for opportunistic acquisitions or portfolio enhancements.

Growth Drivers

Key growth enablers for Whitestone have historically included:

- Portfolio Optimization: Acquisition of strategic retail/commercial properties in high-demand catchment areas balanced with selective asset dispositions allowed portfolio turnover enhancing yield profiles.

- Leasing Activity: Maintaining high occupancy rates through active leasing efforts bolstered by long-term tenant relationships generates stable recurring income streams.

- Rental Rate Escalations: Embedded lease escalations linked either contractually or indexed to inflation provide organic rent growth critical amid cost pressures.

- Capital Recycling: Deploying capital efficiently through redevelopment or renovations increases asset value driving net operating income improvements.

- Dividend Policy Refinement: Shift from monthly dividends to quarterly payouts with recent hikes improves shareholder cash flow stability attracting yield-sensitive investors [S20].

- Share Repurchase Program: Newly authorized $50 million buyback initiative supports per-share earnings metrics enhancing shareholder returns [S20].

Potential growth trajectory pre-acquisition had these levers contributing incrementally; going forward, realization depends largely on integration strategy under Ares’ stewardship which may accelerate portfolio repositioning or capital deployment.

Risks and Watchpoints

While Whitestone exhibits operational strengths, several watchpoints warrant attention:

- Merger Execution Risk: Completion is conditioned on customary regulatory approvals including antitrust clearances potentially impacted by market conditions or legal challenges; failure would introduce material uncertainty [S6], [S13].

- Shareholder Approval Uncertainty: Although Board recommendation is positive, any adverse shareholder vote or emergence of higher-value competing offers could disrupt plans introducing volatility [S29].

- Business Disruption: Announcement effects often induce distraction among management/tenants/suppliers potentially dampening leasing velocity or renewal negotiations during pendency periods [S4], typical in M&A settings.

- REIT Status Preservation: Continuity of tax-qualified REIT status is critical; possible structural changes post-merger could affect tax considerations altering investor returns [S13].

- Leverage Profile Sensitivity: Despite ample financing sources currently, leverage remains near $650 million net debt level; shifts in interest rates or leasing profiles could stress coverage ratios especially if operating disruptions occur pre-close [F1], [S12].

- Retail Property Market Pressures: Structural shifts from e-commerce growth continue posing long-term tenant base survivability issues impacting income durability.

What To Watch Next

Investors and industry participants should monitor several milestones:

- Special Shareholder Meeting Outcome: Expected to be scheduled post-merger proxy filings; vote results will determine deal viability timeline [S8], [S11].

- Regulatory Filings & Approvals: Updates regarding Hart-Scott-Rodino Act filings or other jurisdictional clearances influence closure timing.

- Post-Merger Operational Plans: Any guidance or disclosures from Ares about strategic direction will signal future portfolio focus areas or capital allocation shifts.

- Dividend Declarations During Pendency: Ongoing dividend policy adherence offers clues on financial discipline maintained during transition phase.

- Lease Renewal Rates & Occupancy Trends: Quarterly supplemental operational disclosures through recently reported periods will indicate whether core portfolio fundamentals sustain amid merger-related uncertainty.[N1]

Financial Profile Highlights as Contextual Support

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $5mm | |

| 2025-12-31 | ||

| Total debt | $649mm | |

| 2025-12-31 | ||

| Net debt | $644mm | |

| 2025-12-31 |

Source: SEC companyfacts cache [F1].

Below is a snapshot derived from latest annual filings highlighting key metrics:

| Metric | Value (USD) | Period End |

|---|---|---|

| Revenue | 43.92 million | |

| 2025-12-31 | ||

| Net Income | 22.84 million | |

| 2025-12-31 | ||

| Cash & Equivalents | 4.89 million | |

| 2025-12-31 | ||

| Total Debt | 649.35 million | |

| 2025-12-31 | ||

| Approximate Net Debt | 644.46 million | |

| 2025-12-31 |

Liquidity stems from the revolving credit facility ($375M) coupled with an equal-sized term loan providing extended tenor funding at competitive interest rates (~Term SOFR + ~135bps) hedged via interest rate swaps minimizing volatility risks [F1], [S12]. Net income reflects stable operational profitability anchored in lease revenues less operating expenses before interest/capital activity.

Conclusion

Whitestone REIT's current narrative is dominated by its definitive merger agreement with Ares Management funds framing a strategic inflection point accompanied by robust financing arrangements safeguarding firm execution capability. The company’s differentiated model emphasizing integrated self-management over retail-focused assets demonstrates resilience amid broader sector headwinds but faces execution risk linked explicitly to acquisition closure dynamics. Stakeholders should keenly track upcoming shareholder meetings, regulatory developments, and interim operational results that will illuminate the trajectory toward deal consummation or alternative pathways.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments