Fossil Group’s Financial Turnaround and Strategic Reset Post-2025 Restructuring

Following a comprehensive debt restructuring in late 2025, Fossil Group aims to stabilize its financials and reposition its legacy watch and accessories brand amid competitive pressures and operational challenges.

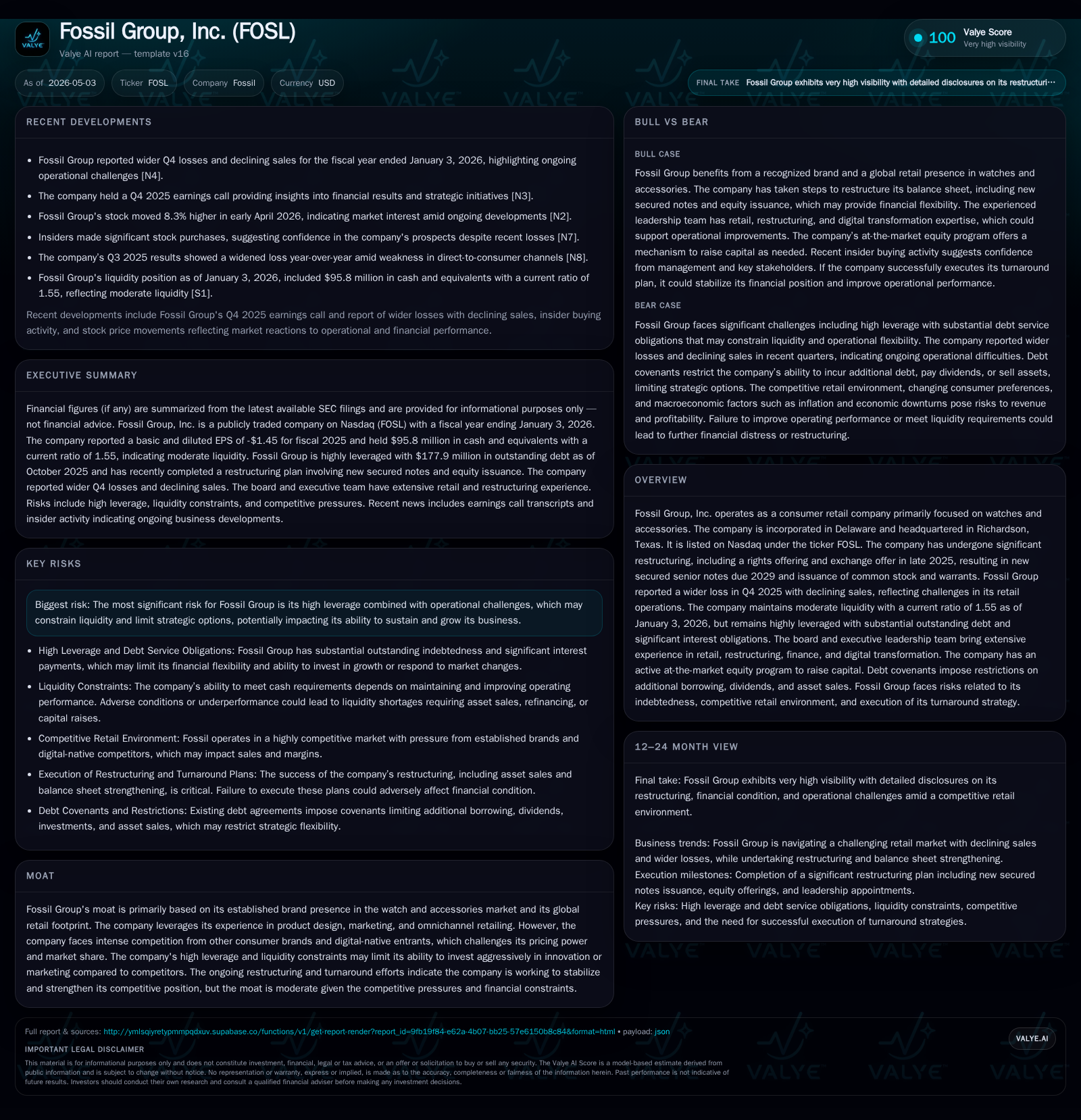

Fossil Group's latest 10-Q for Q3 2025 reveals widening losses alongside declining sales, underscoring ongoing pressures within its retail operations. The company's November 2025 capital restructuring replaced maturing notes with new senior secured debt due in 2029, supplemented by equity issuance and warrants, which helped ease imminent liquidity pressures. Despite this, Fossil remains highly leveraged with substantial net debt, constraining investment flexibility. Operationally, the company depends on its established brand presence and licensing portfolio but faces intensifying competition from digital-native entrants. Recent leadership changes hint at strategic recalibration as the company seeks growth from innovation and omnichannel expansion while navigating risks from high leverage and market volatility.

Latest Operating Update: Key Takeaways from Q3 2025 and April 2026 Events

Fossil Group’s most recent quarterly disclosure on November 13, 2025 ([S2]) highlights intensified challenges with wider operating losses accompanied by declining sales within its retail segment. This reflects persistent headwinds in consumer spending patterns for traditional watchmakers as well as inventory adjustments impacting revenue volume. Despite these operational strains, the company addresses near-term solvency concerns through a comprehensive financial restructuring finalized in November 2025 ([S25],[S26]), which included a rights offering combined with an exchange offer to refinance its maturing senior notes.

The restructuring replaced $150 million of old notes due in 2026 with approximately $153 million in new senior secured notes due in 2029. Incremental new money financing raised was $32.5 million via issuance of higher-yielding first-out first-lien notes bearing a coupon of 9.50%, along with common stock issuance and warrants. This provided critical capital infusion while extending debt maturities materially beyond the near term.

From a liquidity standpoint, Fossil entered fiscal year end January 3, 2026 with roughly $95.8 million in cash and equivalents and current assets totaling about $467.8 million against current liabilities near $301.8 million—yielding a current ratio of approximately 1.55 ([F1]). While this suggests moderate liquidity cushioning, net debt remains robust at about $109.3 million ([F1]), signifying continued pressure on cash flow allocation.

Further signaling an evolving strategic posture is the resignation announcement of the Chief Commercial Officer in April 2026 ([S3]), indicating potential shifts in leadership priorities or commercial focus amidst ongoing turnaround efforts.

Fossil’s Business Model: Revenue Streams, Product Quality, and Customer Appeal

Fossil Group’s core business generates revenue principally from designing, marketing, and selling watches and accessories globally ([S1]). Its multi-brand portfolio encompasses proprietary lines as well as licensed brands where Fossil acts as manufacturer or marketer under licensing agreements. These licenses contribute supplementary income streams but rely heavily on brand strength.

The company’s revenue mechanics hinge on wholesale orders from retail partners—including department stores plus specialty retailers—and increasingly direct-to-consumer channels such as branded e-commerce platforms. Sales volumes are sensitive to cyclical consumer discretionary spending trends but also influenced by product lifecycle dynamics where innovation drives fashion relevance.

Product quality centers on mid-tier watch craftsmanship blending traditional analog designs with smartwatches integrating modern technology, attempting to bridge legacy appeal to younger demographics. However, maintaining sufficient gross margins remains challenging due to competitive pricing pressure that compresses average selling prices amid shifting product mix toward more value-oriented SKUs.

Competitive Environment: Market Positioning Within Watches and Accessories

Within the watches and accessories industry, Fossil occupies a middle ground spanning classic heritage brands against newer digital-native entrants aggressively targeting tech-savvy consumers ([S1]). This bifurcation complicates pricing power; legacy firms like Fossil contend with eroding market share against disruptors benefiting from direct online channels and contemporary branding.

Operationally, supply chain robustness has been an area of focus with the appointment of a Chief Supply Chain Officer in mid-2025 ([S1]) to oversee sourcing, manufacturing efficiency, inventory turnover, and logistics—a critical lever given tariff uncertainties and input cost inflation impacting product availability and margin structure.

At the industry level, factors such as geopolitical tariff risks affect component costs variably across sourcing geographies; moreover, excess capacity in certain product segments caps pricing upward flexibility. Brand switching costs are moderate; consumers increasingly treat watches as interchangeable fashion accessories rather than long-term heirlooms.

Growth Drivers: Innovation, Licensing, and Omnichannel Optimization

Fossil’s path to growth focuses on three intertwined levers: accelerating product innovation particularly integrating connected technologies; expanding high-value licensing arrangements; and maximizing omnichannel retail capabilities incorporating both physical store presence optimization and digital commerce enhancements ([S1],[S2],[S3]).

Recent restructuring efforts underscore a commitment to operational efficiencies freeing resources for targeted marketing investments aimed at revitalizing key brands. Initiatives encompass refreshed smartwatch offerings that combine style with emerging functionalities seeking parity with tech competitors.

Licensing renewal cadence serves as a tangible growth barometer; success here sustains royalty streams while fueling brand diversification without direct capital allocation. Concurrently e-commerce penetration improvements aim at capturing channel shift trends accelerated by pandemic behaviors.

KPIs such as online traffic growth rates, license extension outcomes beyond contract expiration dates (noted in March-April filings), and same-store sales stabilization will function as milestones to validate traction against these strategic priorities.

Risk Factors: High Leverage, Operational Challenges, and Competitive Headwinds

Foremost among Fossil's risks is the persistent elevated leverage profile—with total debt around $205 million offset partially by cash balances—leading to substantial fixed interest costs limiting free cash flow available for reinvestment or unexpected shocks ([F1],[S2]). This restricts ability to pivot swiftly should product demand deteriorate further or if economic downturns reduce discretionary budgets.

Operationally, declining retail traffic coupled with intensifying competition from digitally native brands imposes margin erosion risk through relentless price competition targeting mid-market consumers ([S2]). Supply chain disruptions or cost inflation stemming from international tariffs could exacerbate procurement expenses undermining profitability.

Without continued improvement in top-line sales momentum aligned to cost structure optimization the company’s turnaround ambitions face tangible downside risk.

Leadership Changes and Strategic Direction Post-April 2026

The April 24, 2026 departure of Joe Martin as Chief Commercial Officer ([S3]) signifies an inflection point reflecting potential shifts in commercial strategy execution or internal realignment amid challenging market conditions. Given that commercial leadership is pivotal for brand revitalization efforts including client relationship management across wholesale distributors and license partners, this transition carries operational significance.

This change underlines management’s resolve to recalibrate frontline execution capabilities potentially embedding fresh perspectives aligned with the ongoing restructuring objectives aiming at stabilizing revenues while containing costs.

What Investors Should Monitor: Milestones, Guidance, and Execution Signals

Attention should center on quarterly updates addressing:

- Revenue trajectory stabilization or reversal of prior declines,

- Margin improvements driven by mix shift or cost efficiencies,

- Progress on license renewals/extensions indicating sustained brand relevance,

- E-commerce growth rate acceleration as omnichannel strategies mature,

- Refinancing activities or changes to debt covenants affecting capital structure flexibility,

- Leadership succession announcements especially within commercial functions signaling strategic consistency. Monitoring cash flow adequacy versus interest obligations will also be key given solvency considerations inherent in current net leverage balance.[S2][S3]

Contemporary Financial Snapshot: Liquidity, Debt Structure, and Capital Flexibility

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $96mm | |

| 2026-01-03 | ||

| Total debt | $205mm | |

| 2026-01-03 | ||

| Net debt | $109mm | |

| 2026-01-03 | ||

| Current assets | $468mm | |

| 2026-01-03 | ||

| Current liabilities | $302mm | |

| 2026-01-03 | ||

| Current ratio | 1.55x | |

| 2026-01-03 |

Source: SEC companyfacts cache [F1].

| Metric | Value (USD) |

|---|---|

| Cash & Equivalents | $95.8 million |

| Total Debt | $205.1 million |

| Net Debt | $109.3 million |

| Current Assets | $467.8 million |

| Current Liabilities | $301.8 million |

| Current Ratio | 1.55 |

As of the fiscal year ended January 3, 2026 per [F1], Fossil’s liquidity metrics reflect cautious stability post-restructuring but remain pressured by high total indebtedness which commands significant interest expense burden emphasized in MD&A commentary ([S2]).

The newly issued senior secured notes bear interest rates ranging between approximately 7.5% (second-out notes) to 9.5% (first-out notes), imposing meaningful fixed financial obligations that must be serviced quarterly starting March 2026 ([S27],[S28],[S29]). Covenants restricting dividends or asset disposals constrain flexibility further requiring steady operating performance just to maintain compliance.

Disclaimer: This analysis is based solely on publicly available information cited herein without access to nonpublic data or forecasts held by Fossil Group management or affiliates. It does not constitute investment advice but aims to provide informed context on operational footing post recent restructuring developments.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments