MPLX LP Strengthens Midstream Infrastructure with Contractual Stability and Diversified Assets

The latest quarterly filing reveals MPLX’s stable operations supported by diversified midstream assets and long-term contracts, anchoring steady revenue streams amid energy sector dynamics.

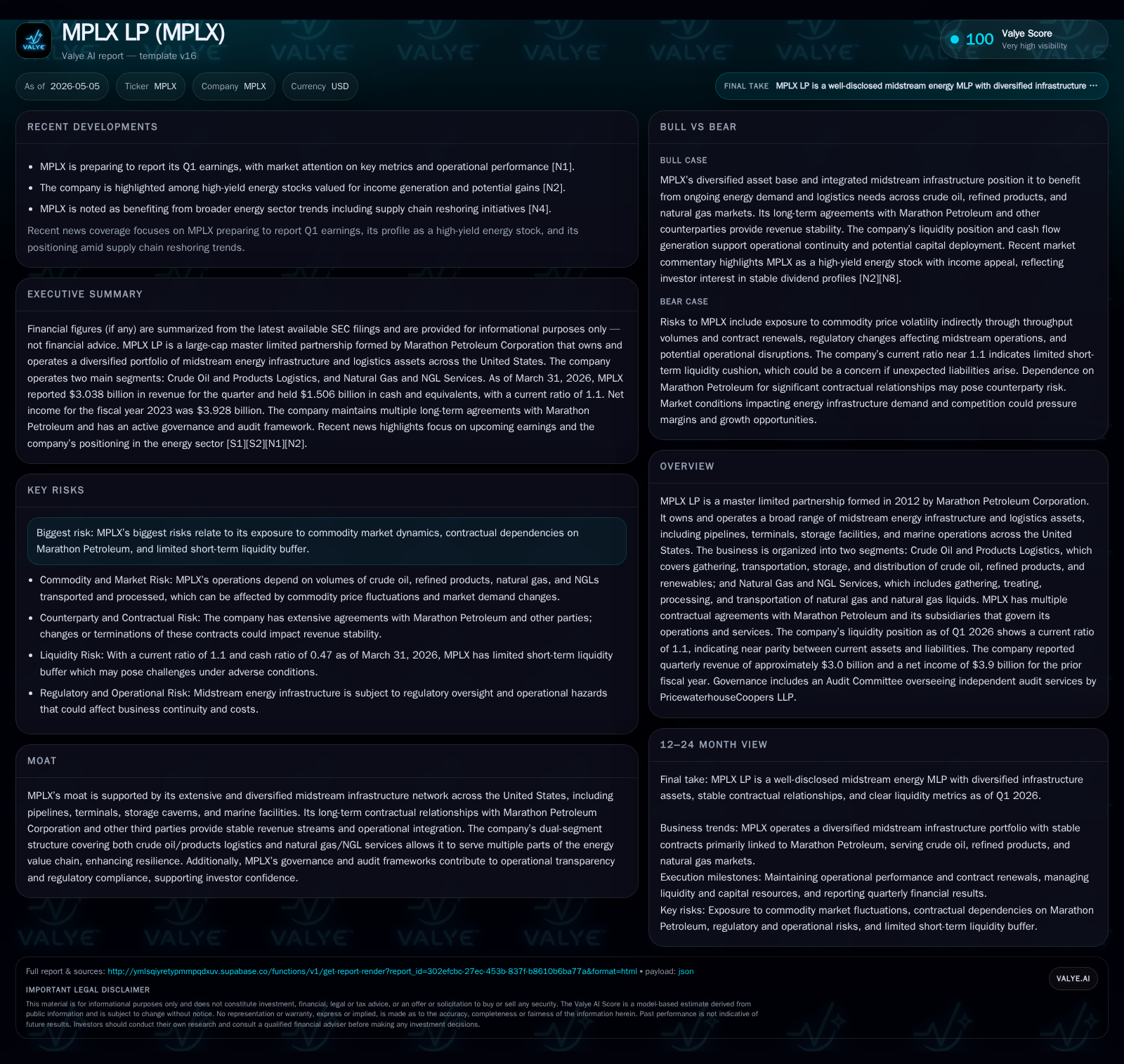

MPLX LP's Q1 2026 filings highlight its continued operational stability underpinned by a diversified U.S. midstream network and enduring contractual ties primarily with Marathon Petroleum Corporation. The company operates through two main segments: Crude Oil and Products Logistics, and Natural Gas and NGL Services, providing it resilience across hydrocarbon value chains. Recent liquidity metrics show a current ratio of 1.1 with substantial cash reserves and debt levels typical for a capital-intensive midstream MLP. Going forward, MPLX faces commodity price exposure risks but benefits from multi-year agreements and strategic infrastructure positioning that support stable cash flows.

Recent Operating Update

MPLX LP’s Q1 2026 SEC filings ([S2], [S3]) provide crucial insights into the company's near-term operating environment. The partnership reported maintaining operational consistency across its midstream assets against a backdrop of evolving energy sector conditions. Notably, MPLX highlighted that as of March 31, 2026, it held $1.5 billion in cash and equivalents alongside $24.4 billion in total debt ([F1]), establishing a current ratio of approximately 1.1—indicating near parity between current assets and liabilities.

In parallel with its quarterly disclosure, MPLX entered into a new $2.5 billion revolving credit agreement expiring in 2031 ([S27]), replacing its prior facility while maintaining no outstanding borrowings under this agreement as of quarter-end. This move preserves liquidity flexibility to support operational needs or growth initiatives without immediate refinancing pressure.

Business Model Overview

Established in 2012 by Marathon Petroleum Corporation (MPC), MPLX functions as a master limited partnership controlling an extensive network of U.S.-based midstream energy infrastructure assets ([S1]). Its business distinguishes itself via two primary segments:

Crude Oil and Products Logistics: This segment encompasses the gathering, transportation, storage, and distribution of crude oil, refined petroleum products (including renewables), along with inland marine operations and terminals. It further includes refining logistics support through storage caverns, rail facilities, docks, loading racks, and ancillary piping infrastructure.

Natural Gas and NGL Services: Covering wellhead-to-market activities such as gathering systems for natural gas, treatment processes to remove impurities or separate liquids, fractionation of natural gas liquids (NGLs), transportation pipelines, and processing plants.

Revenue generation chiefly arises from long-term contractual arrangements primarily with MPC subsidiaries but also includes third-party contracts that provide stable fee-based income independent of direct commodity price exposure ([S20]). These agreements typically specify volume commitments or capacity reservation fees ensuring minimum throughput utilization.

Margins tend to reflect the mix between regulated or contracted fee structures versus commodity-linked revenues; however, the bulk of MPLX’s fee-profile provides resilience during commodity price volatility cycles common to upstream producers.

Industry Structure and Competitive Position

Positioned within the U.S. energy midstream value chain—an infrastructure-intensive sector—MPLX competes among master limited partnerships that own pipeline networks, storage terminals, fractionators, marine facilities, and distribution operations. Key competitive advantages include:

- Diversification across hydrocarbon segments: By operating both crude product logistics and natural gas/NGL services segments, MPLX mitigates dependencies on any single commodity or regional market.

- Extensive Asset Footprint: Its broad operational footprint offers geographical reach across major production basins and refining hubs.

- Contractual Backing from MPC: Long-standing contracts granted by its sponsor provide revenue certainty uncommon among purely merchant midstream operators.

- Integrated Services Offering: Ability to bundle multiple logistic stages from gathering to delivery enhances switching costs for customers reliant on streamlined service delivery.

These factors collectively establish a defensible moat characterized by infrastructure scale combined with embedded commercial relationships fostering customer retention.

Growth Drivers

Several vectors underpin MPLX’s growth prospects:

- Capacity Expansion in Core Basins: Incremental investments targeting increased pipeline throughput capability in prolific crude producing areas serve to capture rising domestic production volumes.

- Renewable Fuel Logistics: Integration of renewable hydrocarbons within product transport allows leveraging existing terminal infrastructure addressing evolving industry fuel mix trends.

- Natural Gas Processing Demand: Continued U.S. natural gas production growth supports higher utilization rates on fractionation plants and treatment facilities.

- Contract Amendments & New Agreements: Ongoing negotiations for contract extensions or new service arrangements with MPC or third parties can enhance revenue visibility over medium terms.

KPIs linked to these drivers include backlog/order book growth for pipeline capacity contracts, utilization rates at processing units, terminal throughput volumes measured in barrels/day or Mcf/day for gases.

Risks and Growth Constraints

While structurally poised for stability, MPLX faces notable risks including:

- Commodity Market Exposure: Although much revenue derives from fees rather than commodity sales directly, underlying production declines or price downturns could reduce overall throughput volumes affecting usage-based fees ([S6], [S7]).

- Dependency on Marathon Petroleum Contracts: A significant share of MPLX’s revenues originates from MPC-related entities; any disruption or unfavorable renegotiation poses operational risk.

- Leverage Levels: With net debt approximating $22.9 billion against $1.5 billion cash ([F1]), financial flexibility hinges upon disciplined capital management amid potential macroeconomic tightening.

- Limited Short-Term Liquidity Cushion: Current ratio near unity suggests working capital is tightly managed; unexpected cash flow interruptions could challenge short-cycle obligations.

- Regulatory Environment: Changes in environmental regulation impacting pipeline operations or permitting delays may hinder asset deployment schedules.

What to Watch Next

Investors monitoring MPLX should focus on several forthcoming milestones:

- Execution progress on announced growth capital projects expanding crude/oil product logistics capabilities or natural gas infrastructure enhancements.

- Updates regarding contract renewals especially those involving Marathon Petroleum entities given their material contribution to revenue streams.

- Quarterly throughput volume metrics signaling demand shifts across both business segments reflecting upstream production trends.

- Regulatory developments or environmental compliance progress impacting capital expenditures or operating licenses.

- Financial updates related to refinancing activity beyond the recent credit facility enlargement or changes in debt covenant compliance.

Financial Snapshot Q1 2026 [F1][S2]

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $1506mm | |

| 2026-03-31 | ||

| Total debt | $24.4bn | |

| 2026-03-31 | ||

| Net debt | $22.9bn | |

| 2026-03-31 | ||

| Current assets | $3.5bn | |

| 2026-03-31 | ||

| Current liabilities | $3.2bn | |

| 2026-03-31 | ||

| Current ratio | 1.1x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value (USD Billion) | Period End |

|---|---|---|

| Cash & Equivalents | 1.51 | |

| 2026-03-31 | ||

| Total Debt | 24.38 | |

| 2026-03-31 | ||

| Current Assets | 3.52 | |

| 2026-03-31 | ||

| Current Liabilities | 3.19 | |

| 2026-03-31 | ||

| Current Ratio | 1.10 | |

| 2026-03-31 | ||

| Net Debt | 22.88 | |

| 2026-03-31 |

This financial profile underscores significant leverage consistent with capital expenditure norms in midstream infrastructure while reflecting sufficient liquidity headroom courtesy of cash reserves plus undrawn credit lines ([S27]).

Conclusion

MPLX LP has fortified its position as a versatile midstream operator coupling an integrated asset base with enduring contractual relationships primarily anchored by Marathon Petroleum Corporation affiliation. The latest quarter affirms operational steadiness amid sector cyclicality. However, shareholders should remain attentive to macrocommodity influences affecting throughput volumes alongside dependency concentration risks stemming from key counterparty exposure.

This analysis is based solely on publicly filed documents as of May 5, 2026. It is prepared for informational purposes without investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments