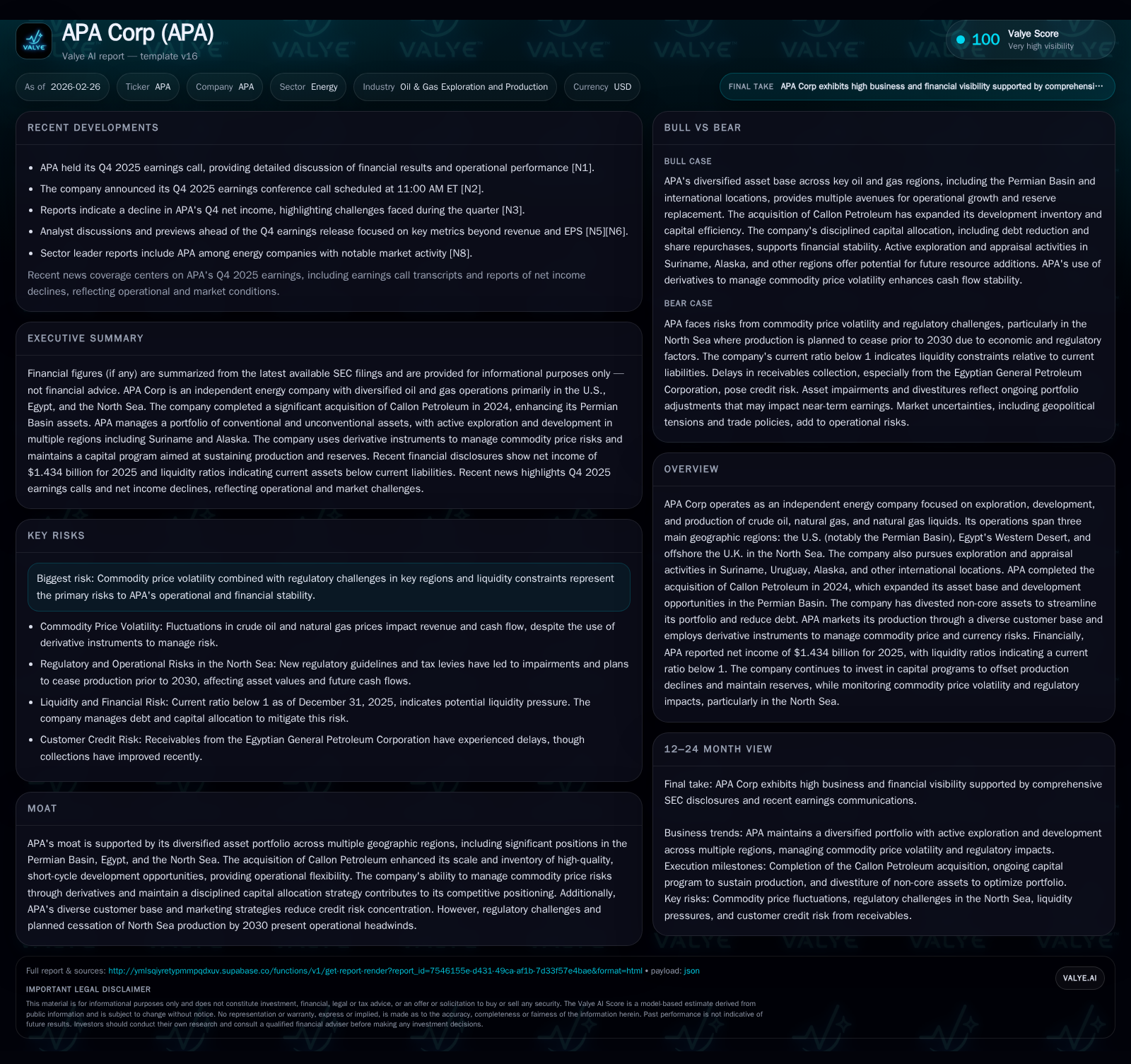

APA Corp Harnesses Permian Expansion and International Assets to Sustain Financial Momentum

Exploring APA’s levered growth from recent acquisitions and diversified operations amid evolving operational and regulatory pressures.

APA Corp’s financial revival in 2025 prominently reflects the strategic integration of Callon Petroleum, which bolstered its core Permian Basin footprint and expanded its short-cycle development inventory. The company’s tripartite geographic presence spanning the U.S., Egypt, and North Sea assets provides both diversification benefits and operational complexity. Navigating commodity price fluctuations alongside regulatory headwinds—particularly the planned North Sea production exit—tests APA’s capital discipline, yet persistent deleveraging efforts and a focus on streamlining position it for stable cash flow generation. Upcoming appraisal results in Alaska and risk-managed drilling programs remain critical milestones in assessing APA’s growth trajectory beyond 2026.

Evolution of APA Corp’s Growth Trajectory

APA Corp’s financial results for fiscal year 2025 underline a significant rebound following a dynamic phase of asset realignment and expansion. Operating income increased sharply by 26.4% year-over-year to $3.087 billion [F1], contrasting with the prior year's $2.442 billion figure despite overall industry cyclicality.

This income uplift closely tracks the April 2024 acquisition of Callon Petroleum Company—a transaction valued at approximately $4.5 billion inclusive of its debt—that markedly augmented APA’s acreage and well inventory within the Permian Basin, the company's primary cash flow engine [S17]. The consolidation allowed realization of scale efficiencies, contributing to improved drilling economics and operational leverage.

Operating cash flow similarly advanced by 25.6% to $4.545 billion in 2025 versus $3.620 billion in 2024 [F1], underpinning liquidity inflows essential for APA’s aggressive deleveraging post-acquisition phase.

Equity has expanded materially over this period—from approximately $528 million at end-2024 to over $6.093 billion at end-2025—supporting a robust return on equity estimated at roughly 23.5% when deploying net income against year-end equity balances [F1]. This equity surge reflects earnings retention combined with manageable share repurchase activity.

Historical performance (annual)

| FY | CFO ($bn) | OpInc ($bn) |

|---|---|---|

| 2025 | 4.5 | 3.1 |

| 2024 | 3.6 | 2.4 |

| 2023 | 3.1 | 3.6 |

| 2022 | 4.9 | 5.6 |

Source: SEC companyfacts cache [F1].

Note: Net income series limited; FY2025 only available figure.

Asset Portfolio Diversity: Regional Breakdown and Strategic Moves

APA operates across a triad of principal geographic regions: the Permian Basin in the U.S., Egypt's Western Desert onshore fields, and offshore U.K.'s North Sea developments [S12]. Beyond these, exploration endeavors extend to Suriname, Uruguay, Alaska, among others.

The Permian Basin constitutes APA's cornerstone with a concentrated position following the Callon acquisition which added approximately 120,000 net acres in Delaware Basin plus roughly 25,000 net acres in Midland Basin [S11]. Total confirmed net acreage is about 406,000 acres in Midland alone plus an estimated additional acreage aggregating approximately 217,000 in Delaware Basin as cited for end-2025 [S19].

Drilling success is noteworthy with reported success rates of 100% for gross development wells drilled during the year: an indicator of precise geological targeting and robust operational execution that enhances the quality of APA's short-cycle inventory [S4]. This infusion of high-quality drilling locations enables effective cost management through tighter well spacing and reduced completion intensity.

Internationally, Egypt contributes around one-third of total production with approximately 176 million barrels equivalent proved reserves post noncontrolling interest adjustments representing a meaningful component of APA’s portfolio diversification strategy [S26]. The North Sea offshore assets, accounting for about seven percent of production volume and reserves proportionally smaller than U.S. or Egypt but still strategically valuable, are on track for planned cessation by year-end 2030 consistent with regulatory frameworks and asset life-cycle considerations .

Alaska represents a nascent but potentially transformative venture where APA reported successful appraisal drilling results in late-2025 including flow testing averaging around 2,700 barrels per day from discovered reservoirs on roughly 163,000 net undeveloped acres on North Slope territory [S4]. Further evaluation is ongoing to quantify reserves impacts.

Recent Financial Performance: Operational Drivers and YoY Dynamics

Reviewing calendar Q4 results disclosed in earnings calls reveals mixed operational effects tempered by fluctuating commodity prices yet overall cost discipline contributed heavily to annual gains despite Q4 net income decline relative to sequential quarters [N1][N9]. Commodity hedging activities employing derivatives such as swaps and options on oil and gas volumes provide some downside protection though none are designated as formal cash flow hedges—highlighting a tactical stance balancing cost against flexibility amid price volatility [S14].

The company's realized prices for hydrocarbons coupled with successful drilling campaigns sustained production volumes effectively offsetting natural decline rates common in maturing fields. Cost improvements notably stemmed from reduced drilling/completion costs enabled by Callon's integration synergy and operational scalability particularly within tight oil zones [S11][S19].

EBITDA margins were maintained within competitive industry ranges albeit slightly compressed quarter-on-quarter due to market mix shifts; margin resilience owes largely to broad-based operational optimization supported by differentiated product marketing strategies emphasizing premium liquid index sales points across regional benchmarks like WTI Midland or West Texas Sour prices adjusted for transport differentials [S21].

2026 Outlook: Production Levels, Capital Program, and Market Considerations

APA projects maintaining its upstream capital expenditure plan at sufficient levels aimed primarily at offsetting natural base declines while selectively advancing high-return development projects predominantly within the Permian assets that provide shorter cycle investment payback profiles compared with international counterparts [N1][S4]. The company continues a measured approach towards new ventures contingent upon commodity price ceilings supporting economic drilling thresholds.

Onshore U.S. activity retains priority with expected mid-to-high single-digit rig counts focusing on Wolfcamp and Bone Spring formations; offshore programs are inherently more capital intensive but represent stable albeit declining revenue streams as North Sea operations approach sunset mandates around decade end [S4].

Notably, scheduled cessation of North Sea production introduces structural headwinds constraining long-term growth potential but releases resources increasingly towards high margin U.S assets fostering an operational pivot aligned with shareholder value maximization intent.

Risks and Constraints: Regulatory Environment and Commodity Price Volatility

The incumbent regulatory framework especially relevant offshore U.K.—mandating phased-out production by no later than end-2030—presents tangible risks involving accelerated asset abandonment costs alongside stranded reserve challenges potentially compressing future reserve replacement ratios absent offset by new discoveries or acquisitions [N7]

Commodity markets remain exposed to global macroeconomic swings including geopolitical tensions influencing OPEC+ decisions impacting supply baselines; these dynamics directly affect realized pricing power despite derivative overlays designed to manage earnings volatility thereby imposing margin pressure uncertainty as noted by recent analyst previews highlighting potential earnings softness in near quarters [N7][N9]. Liquidity risks are contained but susceptible to sharp downturns warrant cautious capital planning.

Capital Allocation Focus: Debt Reduction, Dividends, and Share Repurchases

APA has demonstrated disciplined capital stewardship highlighted by significant debt retirement initiatives utilizing proceeds from divestitures exceeding half a billion dollars from non-core asset sales predominantly in New Mexico during late-2025 aiming to bolster balance sheet resilience post-Callon accession [F1][S11][S23]. Total long-term debt was reduced from nearly $6 billion at end-2024 down to approximately $4.3 billion by fiscal close-off representing meaningful deleveraging progress within twelve months window.

Liquidity metrics show a current ratio around .82 reflecting tight working capital positioning but supported by robust operating cash flows facilitating dividend payments consistent with previous distributions totaling roughly $260–$271 million annually combined with prudent share repurchase activity underway though at moderate pace given capital structure goals and cash flow priorities [F1][S23][S24].

Return on equity stability near mid-twenties percentage confirms efficient capital usage amidst an environment requiring attentive cost management aligned with longer-term value approaches.

What to Watch: Key Milestones and Indicators for Future Performance (Analysis)

Looking ahead beyond immediate reporting cycles several factors will critically shape APA’s evolutionary trajectory:

- Drill rig count evolution specifically within Permian Basin formations evidencing continued high success rates or potential stress owing to input cost inflation or regulatory constraints.

- Alaska appraisal well results stemming from promising discovery test flows achieved in late-2025; confirmation here could substantively expand reserve life extending growth prospects beyond near-term horizons.

- Commodity price movements remain paramount; sustained strength would validate CAPEX deployment plans whereas weakening could force retrenchment despite hedging cushions.

- Progress on debt reduction targets will indicate financial flexibility available for opportunistic reinvestment or enhanced shareholder returns.

- Execution risk related to North Sea shutdown plans including decommissioning costs impacting free cash flows over medium term.

These indicators serve as barometers not only for APA’s internal operational pacing but also broader upstream sector health under shifting energy demand paradigms.

This analysis is based solely on information available through SEC filings ([S#]), Nasdaq transcripts ([N#]), companyfacts datasets ([F1]), and Valye News excerpts as of February 26, 2026. It does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments