Mativ Holdings Confronts Profitability Challenges Despite Stable Revenues and Strategic Portfolio Shift

The company’s restructuring and divestiture reshape its segment dynamics amid ongoing operating losses.

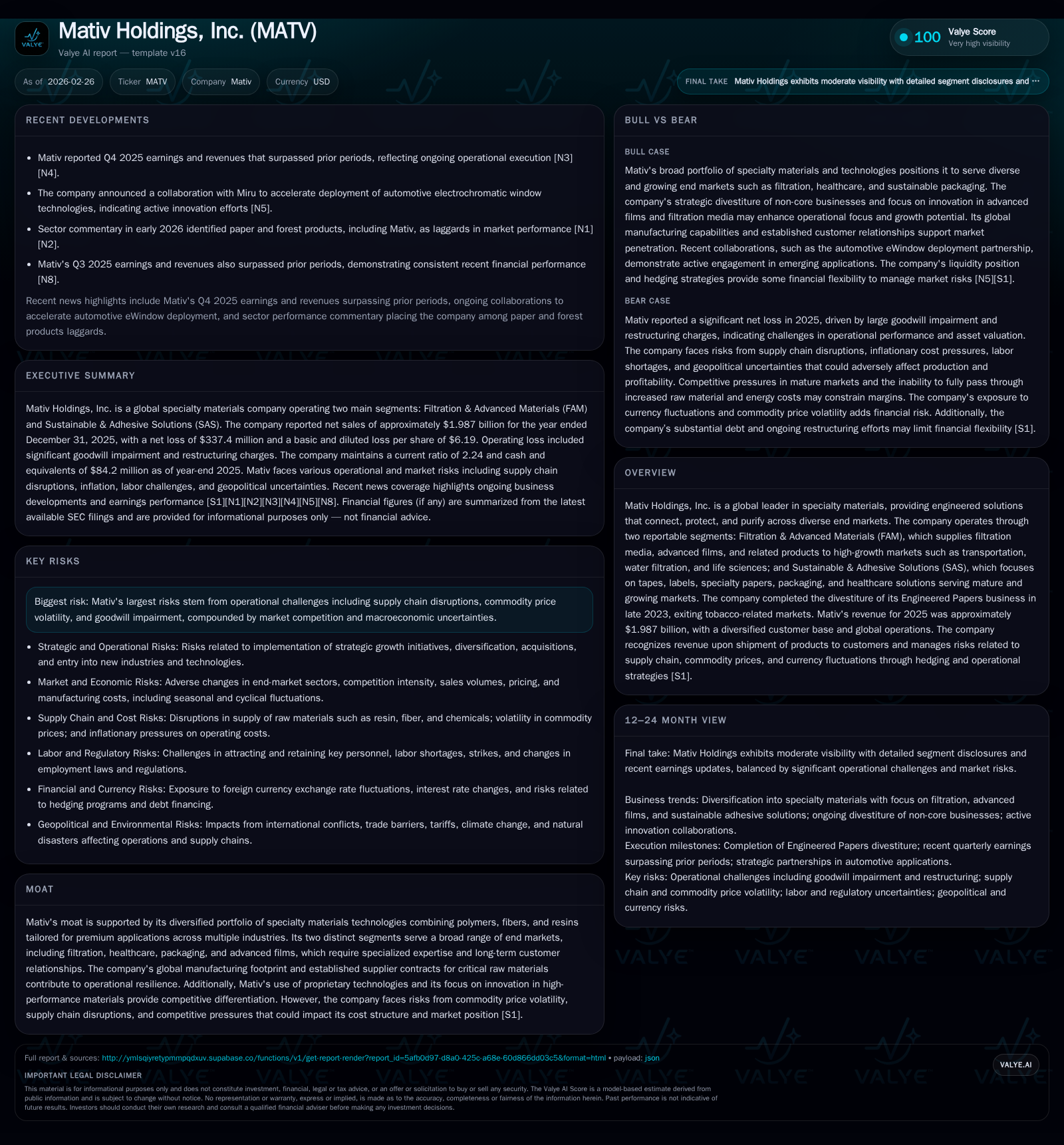

Mativ Holdings, Inc. reported nearly flat revenue in 2025 at just under $2 billion but incurred a substantial operating loss of $384 million, driven largely by goodwill impairments and restructuring charges. The divestiture of its Engineered Papers business completed in late 2023 signals a strategic refocus away from tobacco-related markets toward higher-growth specialty materials segments. While cash flow from operations improved by over 40%, challenges remain as the Filtration & Advanced Materials segment suffered operating losses, offset partially by gains in Sustainable & Adhesive Solutions. Debt remains significant with covenant compliance intact, and capital allocation favors dividends with no recent share repurchases.

Company Overview and Segmentation

Mativ Holdings, Inc. operates as a global supplier of specialty materials engineered for critical applications spanning filtration, advanced films, tapes, labels, packaging, and healthcare solutions. It is organized into two reporting segments: Filtration & Advanced Materials (FAM) and Sustainable & Adhesive Solutions (SAS). The FAM segment targets higher-growth markets such as transportation filtration media, water purification, industrial processes, life sciences, alongside niche areas like advanced wound care films and electrochromatic window technologies [S1][N5][S12]. SAS serves predominantly mature or stable growth end-markets including construction tapes, commercial labels, specialty papers for packaging and print collateral, as well as medical device fixation products.

A pivotal corporate redesign occurred following Mativ's divestiture of its Engineered Papers business late in 2023. This move effectively exited tobacco-related markets previously under SAS’ umbrella and narrowed Mativ’s focus on specialty material technologies with better growth prospects and margin stability [N2][S18].

Historical Financial Performance

Revenues for fiscal year (FY) 2025 totaled approximately $1.987 billion, remarkably steady compared with $1.981 billion reported for FY 2024 — denoting almost flat top-line growth amid challenging market conditions in certain segments [F1]. However, profitability metrics worsened substantially:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -337 | 134 | -384 | 40 | -592.8% |

| 2024 | -49 | 95 | 6 | 55 | +84.3% |

| 2023 | -309 | 107 | -414 | 66 | -4589.4% |

| 2022 | -7 | 202 | 51 | 57 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 22 | 94 | |

| 2024 | 22 | 40 | |

| 2023 | 55 | 11 | 41 |

| 2022 | 72 | 7 | 145 |

Source: SEC companyfacts cache [F1].

The operating loss ballooned from a slight positive $6 million in FY24 to a substantial negative $384 million in FY25 — more than a six-thousand percent decrease year-over-year — driven principally by significant goodwill impairment charges totaling roughly $412 million recorded against the FAM segment during this period [F1][S23]. This one-time non-cash event reflects market recalibrations following sustained share price declines and segment valuation reviews.

Net income followed suit with an expanded loss of $337 million in FY25 vs. an already negative $49 million in FY24.

Despite these earnings headwinds, Mativ generated positive cash flows from operations totaling $134 million in FY25 — up over 40% year-over-year — indicating underlying operational cash generation resilience amid restructuring efforts [F1][S20]. Capital expenditures were curtailed to $40 million from $55 million previously as part of management's capital discipline program.

Dividend disbursements remained consistent at about $22 million annually through this period; however recent years have seen a dramatic reduction compared to pre-impairment payouts implying cautious preservation of capital amid earnings volatility [F1][S25].

Segment-Level Dynamics

Filtration & Advanced Materials (FAM)

The FAM segment encountered significant challenges culminating in an operating loss nearing $360 million for FY25 compared to a positive operating profit near $70 million the prior year. The amplitude of this swing directly corresponds to the goodwill impairment allocated entirely within FAM alongside elevated restructuring costs associated with facility rationalizations and production footprint realignments post-divestiture [S12][S23].

This division serves high-technology filtration media spanning automotive engine air filters, water treatment membranes, life science consumables such as sterile-grade filters for biotech manufacture as well as advanced films utilized in vehicle glazing and emerging smart glass applications leveraging electrochromic innovations [N5][S18]. Though top-line sales held steady (~$768 million), profitability pressure stemmed from competitive raw material cost inflation (not fully passable owing to market dynamics), currency translation effects particularly Euro weakness versus USD, and supply chain disruptions impacting production cadence.

Sustainable & Adhesive Solutions (SAS)

Conversely, SAS maintained stable revenue around $1.22 billion while improving operating profits significantly from approximately $45 million (FY24) to close to $86 million (FY25). This reflects effective cost containment initiatives alongside benefits realized from having streamlined product lines post-Engineered Papers exit focusing on higher-margin specialty tapes, label substrates used broadly across construction DIY markets plus medical device adhesives integral for consumer wellness sectors [S18].

The balanced geographic diversification also supports resilience; approximately half of revenues derive domestically within the U.S., while Europe accounts for just over one-quarter; Asia Pacific and Other foreign locales complete the footprint ensuring coverage across major industrial bases [S18].

Growth Prospects and Constraints

Future growth catalysts lie primarily within innovation-driven expansion across specialized filtration media serving increasingly stringent environmental regulations (e.g., automotive emissions standards), water purification technologies amid global scarcity concerns, life sciences consumables post-pandemic growth phases; plus expanding adoption of advanced films within automotive eWindow applications and security glass markets accelerated by Mativ’s recent collaboration announcements targeting these segments [N5][S1].

Nonetheless, growth is tempered by various operational risks: volatile commodity prices notably resin and fiber inputs; disruptions within international supply chains exacerbated by geopolitical tensions; inflationary pressures on labor and overhead costs; plus intense competition compressing pricing power especially within mature SAS product lines [S9][S13][N3]. Additionally noteworthy is exposure to macroeconomic uncertainties impacting discretionary spending particularly construction-related demand where significant SAS components are sold.

Forecasts and Milestones to Monitor

While explicit forward guidance is absent from available disclosures through FY25 filings or earnings calls, key performance indicators to watch include:

- Recovery trajectory for FAM segment profitability after goodwill impairment resets,

- Execution progress on manufacturing footprint optimization reducing fixed cost burdens,

- Raw material cost pass-through capabilities amidst fluctuating energy prices,

- Penetration gains within automotive eWindow deployments stemming from technology partnerships,

- Effects of further portfolio rationalization or potential bolt-on acquisitions targeting innovative specialty materials,

- Stability or improvement in credit metrics influencing future borrowing costs given sizeable leverage position.

Returns Profile and Capital Allocation Policy

Return on Equity (ROE) approximates -67.7% given net losses prevailing against base equity of roughly $499 million at fiscal year-end '25—reflecting the severe impact of impairment charges on retained earnings balances creating an ongoing drag on measured equity returns [F1].

Operationally generated free cash flow (CFO minus capex) was near positive $94 million sustaining liquidity without reliance on new external funding despite debt repayments executed through the year [$161.9M principal repaid vs proceeds raised of only ~$82M implying modest deleveraging effort] [F1][S20].

Dividend distributions are maintained though conservative relative to historical levels at ~$22 million annually aligning with cash generation capacity while share buybacks have not been resumed since minor repurchase activity concluded after FY23.[F1][S25]

Capital expenditure discipline is evidenced by sequential reductions keeping investments focused primarily on maintenance CapEx possibly supplemented by targeted capacity or technology upgrades aligned with strategic priorities laid out by management [F1][S17].

Capital Structure and Liquidity Positioning

Mativ maintains an aggregate debt load slightly above one billion dollars distributed across revolving credit facilities ($160M outstanding), Term Loan A/B facilities ($200M combined), delayed draw term loan ($270M), supplemented by senior unsecured notes totaling $400M due 2029 carrying an interest coupon at 8%. Despite rising average interest cost (7.46% weighted average effective rate accounting for hedges), Mativ remains covenant compliant under amended credit arrangements designed to accommodate leverage reduction paths with specified net debt-to-EBITDA ratios tightened over time through Dec ‘25 onward periods ensuring financial discipline [F1][S4–8], [S10,S16,S27]

The company employs interest rate swap instruments prudently mitigating variability risks tied to benchmark SOFR/EURIBOR fluctuations. Global treasury liquidity management incorporates notional cash pooling agreements enhancing operational flexibility across subsidiaries' bank accounts internationally enabling offsetting overdrafts against surpluses minimizing interest costs when practical.[S8]

Risks Summary

Key risk factors emphasized include vulnerabilities associated with:

- Execution complexity tied to strategic transformations including geographic redistribution,

- Potential goodwill impairments triggered by volatility in share price or downgraded cash flow projections,

- Cyclical variability manifesting through end-market sensitivity affecting volumes/prices especially within industrial and construction sectors,

- Raw material price inflation not fully recoverable leading to margin compression,

- Supply chain disturbances affecting raw material availability or costing structures including energy input volatility especially European exposures,[S9,S13,S19]

- Geopolitical tensions influencing trade policies/tariffs that could hinder sales penetration,[N3,N4]

- Labor market tightness or labor actions impacting manufacturing continuity including collective bargaining agreements especially notable internationally,[S21]

- Regulatory scrutiny around environmental adherence potentially resulting in incremental compliance costs,[S11]

- Cybersecurity/data privacy breaches undermining proprietary data protection frameworks,[S9]

- Technological disruption requiring ongoing R&D investment balancing short-term cost against long-term competitive moat.[S26]

Conclusion

In sum, Mativ Holdings stands at a strategic inflection point defined by significant portfolio repositioning through recent divestitures coupled with operational challenges reflected acutely in the sizable impairment charges reported during FY25. Results underline stress particularly within the Filtration & Advanced Materials segment despite resilient sales volumes across both reporting units.

The firm’s notable operational cash flow generation paired with capital expenditure prudence underpins a cautiously constructive liquidity profile supporting ongoing business transformation initiatives. Vigilance around execution risks related to supply chains and persistent cost inflation remains essential given intensifying competition within specialty materials markets.

Market participants should track upcoming quarterly updates closely regarding profitability trends within FAM alongside adoption momentum on innovative film applications arising out of collaboration partnerships underpinning future growth potential.

Disclaimer: This report is intended solely for informational purposes based on publicly available data without offering investment advice or recommendations concerning any securities mentioned herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments