Carriage Services Inc’s Financial Surge and Strategic Reorientation Through 2025

Carriage Services has demonstrated marked earnings growth against a backdrop of leadership realignment and emerging supply chain risks.

Carriage Services Inc. experienced significant financial growth in 2025, driven by operational efficiencies and strategic expansion within its funeral home and cemetery operations. Recent executive promotions signal a long-term corporate vision aligning leadership with future growth ambitions. However, challenges loom from U.S. trade policy volatility impacting supply chain costs, which could pressure margins. The company continues to prioritize shareholder returns through consistent dividends supported by strong free cash flow, while carefully managing capital expenditures and share repurchases.

Steady Historical Growth Driven by Operational Expansion and Efficiency Gains

Carriage Services Inc. advanced its financial performance significantly over recent years, culminating in a notable acceleration throughout fiscal 2025. Key annual metrics reveal revenue of approximately $97.7 million in operating income for FY2025—up nearly 19.4% from $81.8 million the prior year—and net income soaring to $51.5 million, a robust increase of 56.3% versus the previous twelve months [F1]. Revenue growth paced at roughly 3.5%, indicating measured top-line expansion complemented by meaningful margin improvements tied directly to operating leverage and efficiency gains.

This favorable trend reflects the company’s execution in optimizing unit economics at its funeral homes and cemetery locations, where operating margin expansion has contributed to improved earnings quality. Operating cash flows also rose by an estimated 16.7%, underscoring sustained free cash flow generation capacity despite rising costs [F1]. Incremental capex spending (+28.1%) highlights targeted investment in property upkeep, technology infrastructure, and potentially lot development to sustain sales backend support.

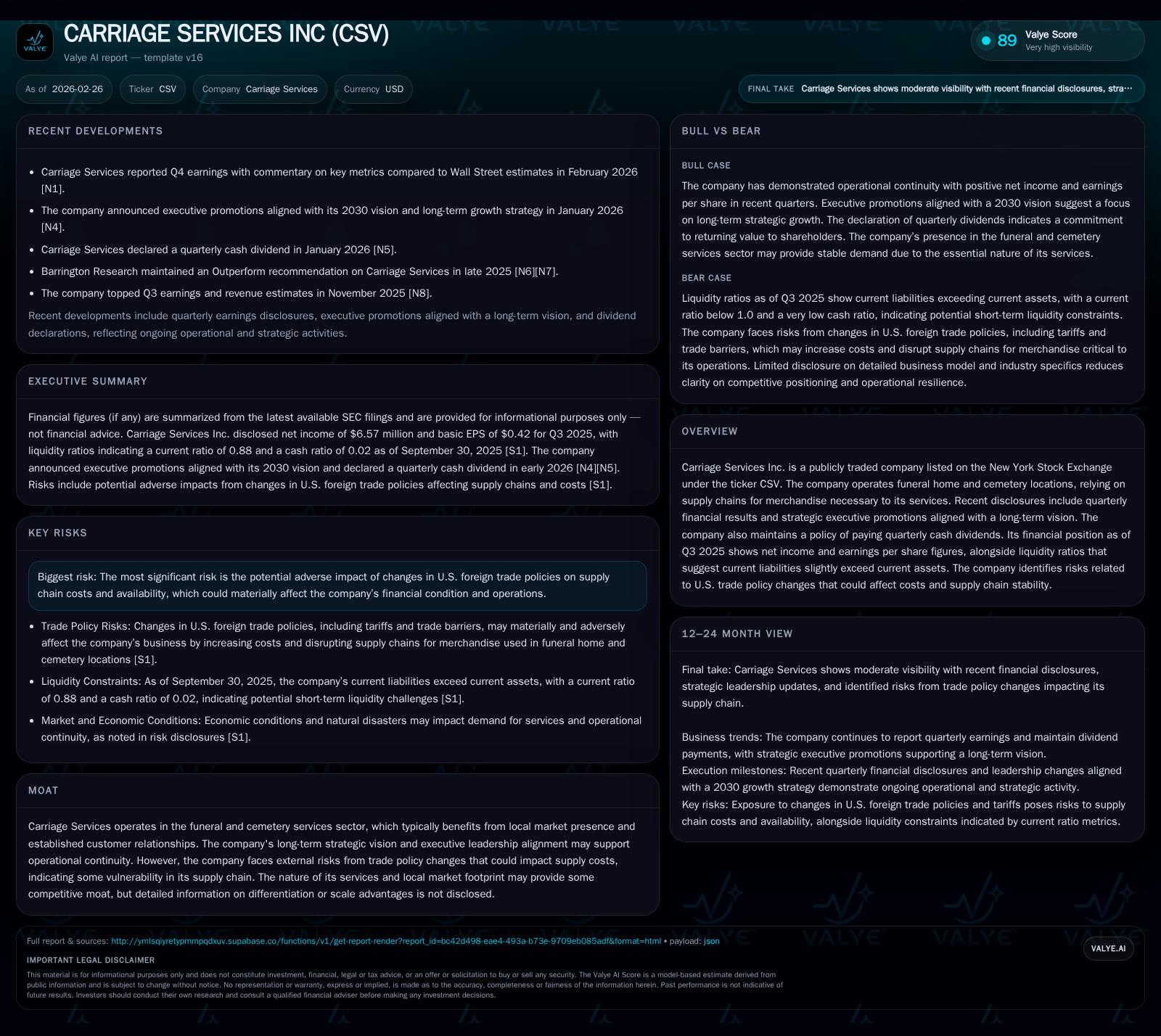

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 52 | 61 | 98 | 21 | +56.3% |

| 2024 | 33 | 52 | 82 | 16 | -1.4% |

| 2023 | 33 | 76 | 81 | 18 | -19.3% |

| 2022 | 41 | 61 | 80 | 26 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 7 | 40 | |

| 2024 | 7 | 0 | 36 |

| 2023 | 7 | 0 | 58 |

| 2022 | 7 | 37 | 35 |

Source: SEC companyfacts cache [F1].

Table: Historical Financial Performance Summary — Carriage Services Inc.

The displayed growth trajectory showcases an inflection point in profitability margins driven partly by operational refinements across the network’s local service nodes where funeral homes benefit from economies of scale and the amortization of fixed support center expenses.

Leadership Transitions Aligned With a Long-Term Vision Through 2030

Early in 2026, Carriage Services announced key executive promotions designed to synchronize management efforts with a corporate vision extending through the decade [N5]. Steven D. Metzger’s elevation to President and Chief Operating Officer underscores a grooming of leadership with comprehensive institutional knowledge—having previously served as General Counsel and other senior roles—positioning operational oversight closely alongside the CFO function.

These leadership adjustments reflect governance continuity principles essential in service businesses where cultural cohesion drives brand trust within communities served [N5]. By advancing seasoned executives internally, Carriage Services aims to maintain momentum on strategic initiatives while strengthening risk management frameworks amidst external uncertainties.

Trade Policy Volatility Threatening Supply Chain Stability and Costs

The company's filings articulate heightened concern surrounding U.S. foreign trade policies implemented throughout 2025, notably impacting import tariffs on goods from countries including China, Mexico, and Canada [S2], [S4], [S5], [S6]. Constructed as risk factors in SEC disclosures, these tariff actions—some paused—introduce substantial uncertainty regarding merchandise pricing inflation that directly affects toolbox cost structures for funerary products such as caskets and memorialization items.

Such tariff-induced supply chain inflation may exert upward pressure on operating expenses precisely when Carriage Services seeks to sustain margin expansion [S2]. While contingent mitigation measures are referenced, persistent volatility in international trade relations could disrupt planned procurement or raise costs beyond forecasted thresholds.

2025 Financial Results: Revenue Growth, Profitability, and Cash Flow Landscape

The Q4/Full-year results illuminated by the company late February confirm continued positive earnings momentum [N1], [S3]. Total operating income grew near double digits year-over-year in line with full-year figures noted earlier; meanwhile, reported liquidity ratios hovered with current assets slightly below current liabilities (current ratio approx. 0.98), fitting working capital patterns typical for middle-market operators heavily invested in inventory-like lot availability-for-sale within cemeteries [F1], [S1].

Free cash flow—a critical metric indicating funds available for discretionary use after maintenance capex—remained robust at around $40 million for FY2025 (operating cash flow minus capex), permitting ongoing shareholder returns without compromising asset reinvestment needs [F1].

Capital Allocation: Robust Dividends Amid Prudent Capex and Share Repurchase Decisions

Carriage Services upheld its quarterly cash dividend payments as declared in early January 2026 consistent with past payout patterns totaling roughly $7 million annually [N4], [F1]. These distributions align with an approximate return on equity near 20.2%, demonstrating disciplined capital use against the equity base that’s grown steadily from around $137 million in FY2022 to near $255 million by FY2025 [F1].

Share repurchase activities have been curtailed post-2022 following extensive buybacks previously (notably $36 million repurchased in FY2022 but zero reported for FYs 2023-24), suggesting a shift towards preferential dividend returns amidst evolving business conditions [F1], [S8]-[S23]. Meanwhile, capital expenditures increased moderately over the last year—a sign of balancing investment needed to maintain operational capacity with prudent free cash flow stewardship.

Future Outlook: What Earnings Drivers and External Variables to Monitor

While no formal guidance was provided during recent earnings releases or filings [N1], analysis points to several focal areas influencing Carriage Services’ prospects ahead:

- The evolution of U.S.-imposed tariffs remains pivotal; any resumption or escalation could compress margins materially given merchandise reliance on imports.

- Execution of the newly aligned executive leadership strategy may yield further operational efficiencies or new growth avenues but remains untested over extended horizons.

- Demand dynamics in local deathcare services markets remain generally stable but competitive pressures alongside consumer preferences for pre-need arrangements could shift sales patterns. Monitoring inventory turnover rates for lots available-for-sale within cemeteries will be crucial to gauge embedded growth potential uniquely pertinent to this sector [S1].

Asset Footprint and Market Position: A Closer Look at Funeral Homes and Cemeteries Portfolio

As articulated in the latest Form 10-K disclosure [S1], Carriage Services operates across a diversified geography comprising approximately 155 funeral homes spanning 24 states alongside ownership of 28 cemeteries across nine states. Of these funeral homes, the majority (136) are owned properties versus leased facilities (19), thus providing tangible real estate assets within the network’s operating model.

The cemeteries encompass roughly between 131,000 to over 140,000 developed units available-for-sale as inventory at year-end across recent reporting periods; additionally, Carriage holds nearly 487 acres designated for future development or sale—a material resource ensuring supply-side control over burial plots vital for sustaining long-term property sales volume [S1].

This regional footprint underpins customer intimacy leveraged by local teams familiar with market nuances—a common moat element within funeral services where proximity facilitates trust-based relationships crucial to conversion rates on memorial products and services.

This analysis compiles Carriage Services’ disclosed financials and corporate developments up through early 2026 without projecting investment outcomes or specific forecasts beyond documented data points or identified risk factors.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments