Arena Group Embraces Platform Scale with Renewed Growth and Debt Focus

Recent quarterly and event filings reveal Arena Group's strategic balance of expanding platform capabilities while managing refinancing pressures.

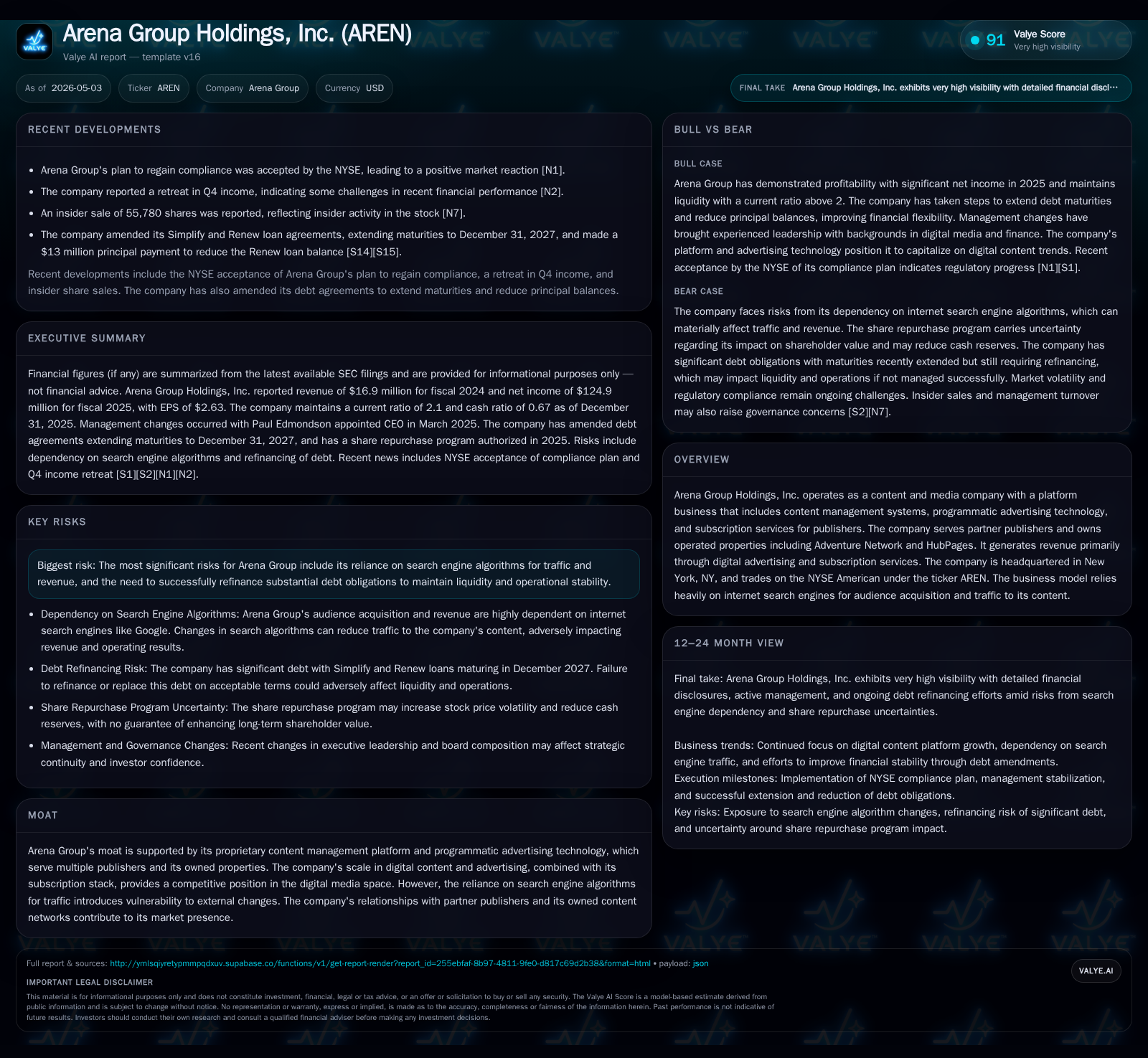

Arena Group Holdings, Inc. continues to develop its proprietary content management and programmatic advertising technology platforms, supporting both partner publishers and its own content networks. Its latest 10-Q and 8-K filings emphasize steady operational progress coupled with a notable focus on refinancing debt obligations extended to late 2027. The company's dependence on search engine algorithms for audience acquisition remains a critical risk, balanced against growth opportunities in subscription services and ad tech innovation. Near-term execution will hinge on traffic stabilization, subscription expansion, and successful debt refinancing.

Latest Operational Update: Q3 and Subsequent Developments

Arena Group’s most recent quarterly disclosure filed in November 2025 [S2] confirms ongoing operational stability without dramatic changes but emphasizes key priorities: optimizing audience acquisition primarily through SEO tactics driving search engine traffic — mainly Google — to its platform-hosted content.

In July 2025, the company announced a share repurchase program authorizing up to 3 million shares over the following year [S15]. This initiative reflects management’s intent to support shareholder value but also introduces cash reserve pressures given existing debt obligations.

The March 2026 event filing [S3] features CEO Paul Edmondson’s presentation reiterating these themes: operational focus remains on sustaining traffic levels amid algorithm volatility while advancing monetization layers via subscriptions and programmatic advertising enhancements. No significant shifts in guidance were noted, implying measured execution within known strategic parameters.

Business Model Deep Dive: Content Platforms, Advertising, and Subscription Stack

Arena Group operates a digital media platform ecosystem combining proprietary content management systems (CMS) with programmatic advertising technology tailored for multi-publisher environments [S1]. Revenue predominantly flows from two streams:

- Digital Advertising: Leveraging programmatic ad buys optimized by in-house technology enables monetization across owned brands (e.g., Adventure Network, HubPages) and partner publisher networks.

- Subscription Services: A growing subscription stack complements ads by providing recurring revenue through premium or exclusive content access.

This integrated platform architecture facilitates scale efficiencies—content creation, distribution, and monetization tightly interwoven—and supports multi-channel customer engagement enhancing retention. The CMS enables quick adaptation to evolving SEO landscapes, crucial since substantial audience volume is sourced from search.

The quality of editorial content versus volume-driven traffic is a tension point; sustaining relevance while attracting large audiences demands continuous investment in editorial standards alongside algorithm-focused tuning.

Competitive Landscape and Industry Positioning

Arena Group positions itself within the crowded digital media space by emphasizing differentiated technology capabilities—particularly its proprietary CMS and programmatic ad infrastructure—which enable it to service a broad base of publisher partners alongside managed owned properties [S1].

However, the industry-wide challenge is the dependence on dominant search engines’ algorithmic changes affecting organic traffic flows. This externally dictated volatility acts almost as a competitor dynamic itself because fluctuations directly impact revenue streams tied to audience size.

In contrast, the company's moat derives from scale advantages: integrated tech stack servicing diverse publishers plus direct subscriber relationships underpin more stable monetization compared to pure ad-funded models. Programmatic ad spend growth globally supports incremental upside if Arena can refine yield through data insights embedded in its platforms.

Growth Drivers: Technology Scale, Audience Diversification, and Monetization

Key growth catalysts revolve around three pillars:

- Partner Publisher Integration: Expanding the network of publishers using Arena’s CMS increases aggregate audience reach and digital ad inventory.

- Subscription Upsell: Converting casual readers into paying subscribers enhances lifetime value per user and diversifies revenue away from purely ad-dependent models.

- Platform Efficiency Improvements: Advances in programmatic advertising algorithms backed by enhanced user data analytics have potential to lift CPMs (cost per mille), improving yield on existing inventory.

Management commentary [S3] signals efforts to diversify traffic acquisition beyond traditional SEO dependency remain ongoing although concrete alternatives are nascent. The success of these initiatives will likely be reflected quantitatively via subscriber growth rates or average revenue per user metrics which investors should track carefully.

Risks and Constraints: Algorithm Dependence and Refinancing Pressures

The most salient operational risk articulated in the November 2025 10-Q risk factors section [S2][S15] centers on dependence on search engine algorithms for traffic acquisition. Changes by Google or others may reduce content discoverability abruptly causing revenue variability difficult to hedge or forecast reliably.

On the financial front, Arena faces significant refinancing challenges. As of December 31, 2025 balance-sheet data [F1], total debt stands near $97.7 million offset by roughly $10.3 million cash resulting in net leverage close to $87.4 million. These extensions provide breathing room but do not eliminate pressure; failure to refinance on acceptable terms or generate sufficient free cash flow risks forced operational curtailment or restructuring events [S4]. Share repurchases under way may complicate liquidity further if not balanced prudently.

Near-term Outlook: Key Milestones and Performance Indicators

Investors should monitor several critical vectors over the coming quarters:

- Subscription Metrics: Growth in active subscriber counts or ARPU (average revenue per user) can provide early signals on success diversifying away from volatile ad revenue.

- Ad Yield Trends: Improvements in CPMs driven by incremental platform efficiency or richer data targeting capability indicate monetization enhancement potential.

- Traffic Stability: Maintenance of organic search traffic levels amidst evolving algorithms will underpin top-line predictability.

- Refinancing Progress: Timely communication confirming execution of refinancing prior to end-2027 maturities will be essential for financial stability.

- Share Repurchase Activity: Pace relative to cash generation speaks to capital allocation discipline affecting overall liquidity dynamics.

Active investor scrutiny around these KPIs can help bridge understanding between reported financial results and underlying operational momentum or stress points [S3][S5].

Financial Snapshot: Liquidity, Leverage, and Capital Allocation

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $10mm | |

| 2025-12-31 | ||

| Total debt | $98mm | |

| 2025-12-31 | ||

| Net debt | $87mm | |

| 2025-12-31 | ||

| Current assets | $36mm | |

| 2025-12-31 | ||

| Current liabilities | $17mm | |

| 2025-12-31 | ||

| Current ratio | 2.1x | |

| 2025-12-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value (USD) |

|---|---|

| Cash & Equivalents | 10,338,000 |

| Total Debt | 97,691,000 |

| Net Debt | 87,353,000 |

| Current Assets | 35,630,000 |

| Current Liabilities | 17,003,000 |

| Current Ratio | 2.1 |

As of December 31, 2025 [F1], Arena Group holds about $10.3 million in cash against nearly $98 million total debt dominated by term loans extended through end-2027 after amendments reducing principal balances partially pre-paid in late 2025 [S16].

All financial figures are drawn directly from official SEC documents or companyfacts databases referenced herein. This memo does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments